Cancer Stem Cells Market Report

RA00032

Cancer Stem Cells Market, By Cancer Form (Breast, Blood, Lung, Brain, Colorectal, Pancreatic, Bladder, Liver), By Application (Targeted CSCs, Stem Cell Based Cancer Therapy): Global Opportunity Analysis and Industry Forecast, 2019–2026

Update Available On-Demand

Cancer Stem Cells Market Outlook 2026:

Global Cancer Stem Cells Market was $786.3 million in 2018, and is projected to generate revenue of $ 1,722.7 million, growing at a CAGR of 10.3% during forecast period.

Cancer stem cells (CSCs) are rare immortal cells having various capabilities such as self-renewal, differentiation, and tumorigenicity along with the capacity to give rise to all cell types found in a particular cancer sample. Cancer stem cells have distinctive properties such as the ability to develop into multiple lineage, potential to proliferate extensively and others. These cells are present in most tissues including lungs, brain, prostates and others. Cancer stem cells play an important role in cancer therapy. There are many connections between stem cells and cancer that are important to understand. For instance, stem cells biology are lending insight into the origins of cancer disease and focuses on fight against the diseases causing cancer.

Driving Factors of Cancer Stem Cells Market:

Rising prevalence of cancer all over the globe is giving significant boost to the growth of cancer stem cells market

Poor food habits, rising prevalence of deskbound work & increase in alcohol consumption among populace are the frequent reasons for the increasing number of cancer patients in the world. According to the Cancer Research UK, there were around 17 million cancer cases that are registered in 2018, and out of which 9.6 million are deaths. There are many key factors that may affect the success rate of chemotherapy and a person's survival rate such as age, overall health and cancer stage. In addition, due to increasing healthcare expenditure at unsustainable pace & inequalities in regards to the access to health systems are also some of the significant factors for the growth of cancer cases.

Increasing awareness of cancer is one of the key factor that can drive the cancer stem cells market. In order to overcome the number of cancer cases and deaths, various public and private organizations are focusing on improving the efficiency of cancer treatment processes. For instance, the Indian Council of Medical Research (ICMR) in association with their Department of Biotechnology (DBT) started focusing on research & development activities to reduce the cancer risks, and they are also working on the standardization of regulatory processes to determine whether a proposed treatment is safe, effective and improved than existing treatments. Moreover, as per a research publication by the Indian Journal of Medical Research, a new type of stem cell has been identified that can help to restore fertility of both men and women who have undergone cancer treatment.

Market Restraints:

Inequality issues coupled with expensive cell therapy treatments will pose a severe threat to the Cancer Stem Cells Market growth

On the other hand, according to CBC Canada, stem cell treatment for each person costs around $5,000 to $8,000. Therefore, due to economic inequalities among the population, the people from middle class and lower middle class sectors are unable to adopt this technology. Moreover, inequalities in diagnosis and treatments through stem cell treatment is significantly hampering the growth of cancer stem cells market.

Cancer Stem Cells Market, by Cancer Form Segment:

Cancer stem cells market for breast cancer is projected to hold a dominant share, owing to the genetic influences & alcohol use

Source: Research Dive Analysis

Breast cancer market generated a revenue of $133.7 million in 2018, and is further projected to reach upto $295.0 million by the year of 2026. Differences in lifestyle, genetic influences & consumption of hormones and alcohol are the common reason for rising cases of cancer patients around the world. This cancer is prevalent human malignancy and frequent cause of cancer related death all over the globe. Thus, breast cancer patient could have comprehensive range of pathological, clinical and molecular characteristics.

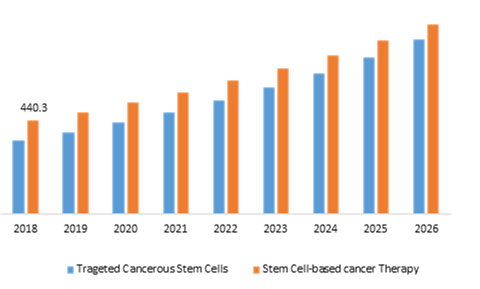

Cancer Stem Cells Market, by Application Segment:

Stem-cell based cancer segment is will generate revenue of $896.9 Mn by the year of 2026

Source: Research Dive Analysis

Stem Cell based Cancer Therapy generated a revenue of $440.3 million in 2018, and is projected to reach upto $896.9 million by the end of 2026.On the basis of application, global cancer stem cells market is segmented into stem cell based cancer therapy and targeted cancerous stem cell therapy. Further, cell based therapy is bifurcated into allogenic SC therapy and autologous SC therapy. Allogenic HSCT (Hematopoietic Stem Cell Transplantation) has advantages over autologous HSCT for BC (Breast cancer) due to factors such as cancer free graft & immune-mediated GvT (Graft vs Tumor) effect mediated by the donor’s immune cell. Successful engraftment rates together with a lower transplant-related mortality and the presence of GvT effect made allogeneic HSCT with RIC (Reduced Intensity conditioning) is the preferable option for the treatment of several solid tumors. For instance, according to the World Health Organization (WHO), breast cancer is most commonly diagnosed disease along with leading cause of cancer deaths in women. Due to aforementioned factors, it is expected that, allogenic cell therapy will upsurge the cancer stem cell market.

Regional Growth Forecast of Cancer Stem Cells Market:

North America region will dominate the global market during the projected period, owing to the rising number of cancer cases, and increasing treatments

North America Cancer Stem Cells Market:

North America market was $365.6 million in 2018, and is further projected to generate revenue of $783.8 million by 2026. In this region, U.S. and Canada are mainly heading the cancer stem cell market. The North America market is expected to grow over the forecast period due to various factors. One of the main factors is the increasing doctors’ involvement in the promotion of stem cell interventions, which are ethical, legal, and regulatory. For instance, the Canadian physicians are getting involved in promoting and providing unproven & unapproved stem cell interventions.

Asia-Pacific Cancer Stem Cells Market is anticipated to grow up to $367.7 Million till 2026

The Asia-Pacific market is expected to be the fastest growing region for cancer stem cells. Governments of Asian countries such as India, Japan and others are drafting policies for the establishment of centers of stem cells and building new infrastructure. Japan is considered as the world leaders in stem cell and regenerative medicine research, as they are good at understanding critical regenerative processes in human health and disease, and also the capability of developing the tools and technologies.

Europe Cancer Stem Cells Market is anticipated to generate revenue of $419.5 Million till 2026.

Stem Cells market is expected to grow in European countries such as Turkey, UK and Denmark. According to Altunta?, founder of Turkish cord blood and bone marrow storage bank, stem cell research is the fastest growing medical practice in Turkey due to the rapid increase in number of stem cell transplants. Younger pool, modern equipment and high-quality, low-cost stem cell treatment are the significant factors that can raise the enormous opportunities for the stem cell’s investors. Moreover, the people are becoming overweight and obese in the UK, which raises the risk of rising a number of cancer patients.

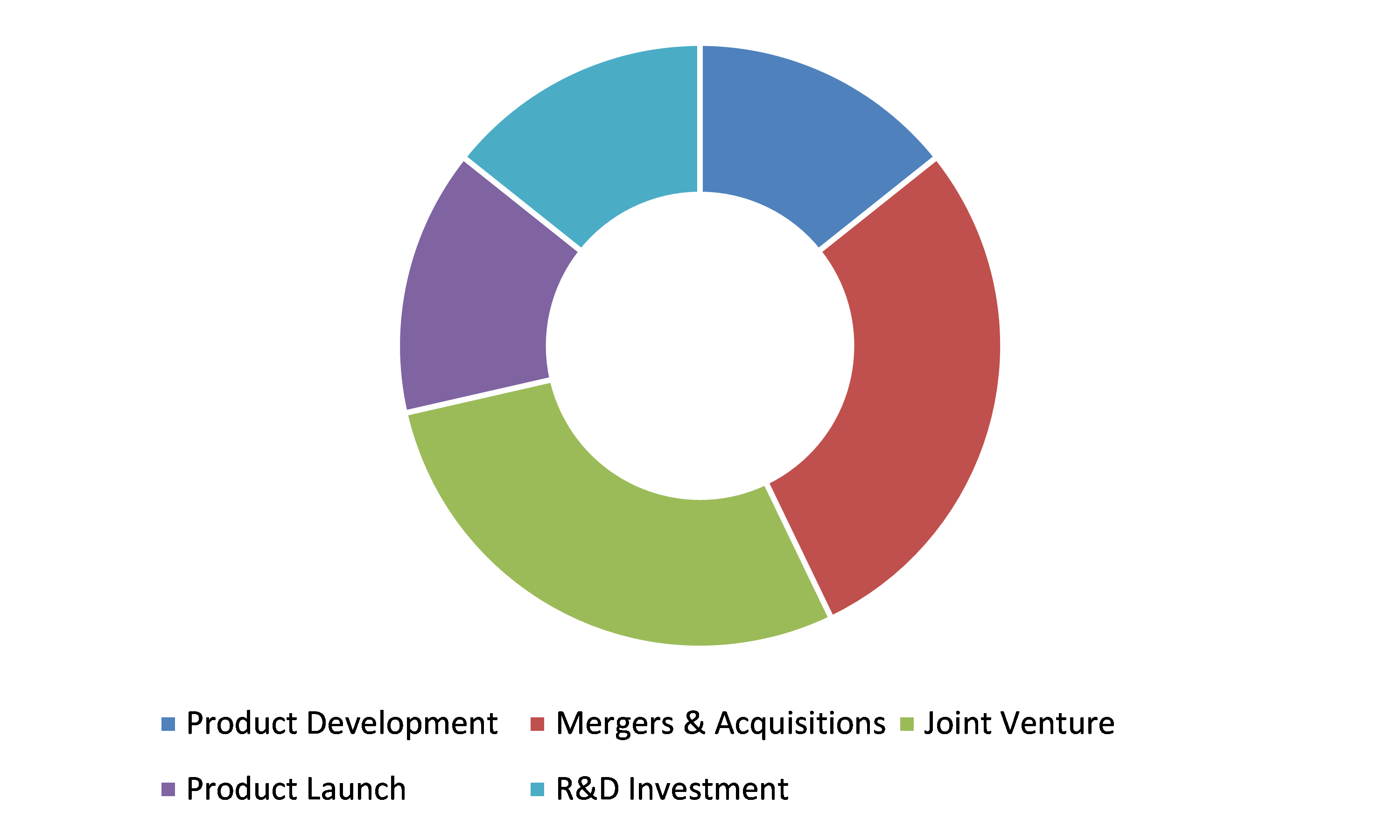

Key Participants in Global Cancer Stem Cells Market:

Merger & Acquisition and Advanced Product development are the frequent strategies followed by the market players

Source: Research Dive Analysis

Some of the major players in the global cancer stem cells market are AdnaGen GmbH, Advanced Cell Diagnostics, Inc., AVIVA Biosciences Corporation, Celula, Inc., Epic Sciences, Inc., Fluxion Biosciences, Inc., Rarecells USA, Inc. and Silicon Biosystems, S.p.A. These players are initiating various steps in order strengthen their presence such as merger & acquisitions, new product development. For instance, in April 2019, Celularity declared a long term lease agreement for the development of 145,000 square-foot advanced cell manufacturing and research facility in the U.S.

| Aspect | Particulars |

| Historical Market Estimations | 2016-2018 |

| Base Year for Market Estimation | 2018 |

| Forecast timeline for Market Projection | 2019-2026 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Cancer Form |

|

| Segmentation by Application |

|

| Key Countries Covered | U.S., Canada, Germany, France, Spain, Russia, Japan, China, India, South Korea, Australia, Brazil, and Saudi Arabia |

| Key Companies Profiled |

|

Q1. What is the scope of Cancer Stem Cells Market in the next five years?

A. The scope of cancer stem cells market in the next five years is 1,561.8 million.

Q2. Which application segment will benefit the Cancer Stem Cells Market?

A. Stem Cell based Cancer Therapy will benefit the cancer stem cells market.

Q3. How do cancer stem cells arise?

A. Cancer stem cells (CSCs) are rare immortal cells having various capabilities such as self-renewal, differentiation, and tumorigenicity. These cells are present in most tissues including lungs, brain, prostates and others.

Q4. What is the difference between stem cells and cancer cells?

A. Stem cells are mostly quiescent, since they replicate very slowly, while the cancer cells grow and replicate much faster.

Q5. What are the factors limiting the market growth of the Cancer Stem Cells market?

A. Inequality issues coupled with expensive cell therapy treatments are the factors limiting the market growth of the Cancer Stem Cells market.

Q6. What are the recent Merger & Acquisition in Cancer Stem Cells market?

A. In June 23, 2020 Century Therapeutics Canada will develop induced pluripotent Stem Cell (iPSC)-derived allogeneic immune cell therapies against glioblastoma (GBM) by acquiring Empirica Therapeutics.

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.4.1. Assumptions

1.4.2. Forecast parameters

1.5. Data sources

1.5.1. Primary

1.5.2. Secondary

2. Executive Summary

2.1. 360° summary

2.2. Cancer Form

2.3. Application

3. Market Overview

3.1. Market segmentation & definitions

3.2. Key takeaways

3.2.1. Top investment pockets

3.2.2. Top winning strategies

3.3. Porter’s five forces analysis

3.3.1. Bargaining power of consumers

3.3.2. Bargaining power of suppliers

3.3.3. Threat of new entrants

3.3.4. Threat of substitutes

3.3.5. Competitive rivalry in the market

3.4. Market dynamics

3.4.1. Drivers

3.4.2. Restraints

3.4.3. Opportunities

3.5. Technology landscape

3.6. Regulatory landscape

3.7. Patent landscape

3.8. Market value chain analysis

3.8.1. Stress point analysis

3.9. Strategic overview

4. Cancer Stem Cells, by Form

4.1. Breast

4.1.1. Market size and forecast, by region, 2016-2026

4.1.2. Comparative market share analysis, 2018 & 2026

4.2. Blood

4.2.1. Market size and forecast, by region, 2016-2026

4.2.2. Comparative market share analysis, 2018 & 2026

4.3. Lung

4.3.1. Market size and forecast, by region, 2016-2026

4.3.2. Comparative market share analysis, 2018 & 2026

4.4. Brain

4.4.1. Market size and forecast, by region, 2016-2026

4.4.2. Comparative market share analysis, 2018 & 2026

4.5. Colorectal

4.5.1. Market size and forecast, by region, 2016-2026

4.5.2. Comparative market share analysis, 2018 & 2026

4.6. Pancreas

4.6.1. Market size and forecast, by region, 2016-2026

4.6.2. Comparative market share analysis, 2018 & 2026

4.7. Bladder

4.7.1. Market size and forecast, by region, 2016-2026

4.7.2. Comparative market share analysis, 2018 & 2026

4.8. Liver

4.8.1. Market size and forecast, by region, 2016-2026

4.8.2. Comparative market share analysis, 2018 & 2026

4.9. Others

4.9.1. Market size and forecast, by region, 2016-2026

4.9.2. Comparative market share analysis, 2018 & 2026

5. Cancer Stem Cells Market, by Application

5.1. Targeted Cancerous Stem Cells

5.1.1. Market size and forecast, by region, 2016-2026

5.1.2. Comparative market share analysis, 2018 & 2026

5.2. Stem Cell Based cancer therapy

5.2.1. Market size and forecast, by region, 2016-2026

5.2.2. Comparative market share analysis, 2018 & 2026

5.3. Others

5.3.1. Market size and forecast, by region, 2016-2026

5.3.2. Comparative market share analysis, 2018 & 2026

6. Cancer Stem Cells Market, by Region

6.1. North America

6.1.1. Market size and forecast, by cancer form, 2016-2026

6.1.2. Market size and forecast, by application, 2016-2026

6.1.3. Market size and forecast, by country, 2016-2026

6.1.4. Comparative market share analysis, 2018 & 2026

6.1.5. U.S.

6.1.5.1. Market size and forecast, by cancer form, 2016-2026

6.1.5.2. Market size and forecast, by application, 2016-2026

6.1.5.3. Comparative market share analysis, 2018 & 2026

6.1.6. Canada

6.1.6.1. Market size and forecast, by cancer form, 2016-2026

6.1.6.2. Market size and forecast, by application, 2016-2026

6.1.6.3. Comparative market share analysis, 2018 & 2026

6.1.7. Mexico

6.1.7.1. Market size and forecast, by cancer form, 2016-2026

6.1.7.2. Market size and forecast, by application, 2016-2026

6.1.7.3. Comparative market share analysis, 2018 & 2026

6.2. Europe

6.2.1. Market size and forecast, by cancer form, 2016-2026

6.2.2. Market size and forecast, by application, 2016-2026

6.2.3. Market size and forecast, by country, 2016-2026

6.2.4. Comparative market share analysis, 2018 & 2026

6.2.5. Germany

6.2.5.1. Market size and forecast, by cancer form, 2016-2026

6.2.5.2. Market size and forecast, by application, 2016-2026

6.2.5.3. Comparative market share analysis, 2018 & 2026

6.2.6. Spain

6.2.6.1. Market size and forecast, by cancer form, 2016-2026

6.2.6.2. Market size and forecast, by application, 2016-2026

6.2.6.3. Comparative market share analysis, 2018 & 2026

6.2.7. France

6.2.7.1. Market size and forecast, by cancer form, 2016-2026

6.2.7.2. Market size and forecast, by application, 2016-2026

6.2.7.3. Comparative market share analysis, 2018 & 2026

6.2.8. Italy

6.2.8.1. Market size and forecast, by cancer form, 2016-2026

6.2.8.2. Market size and forecast, by application, 2016-2026

6.2.8.3. Comparative market share analysis, 2018 & 2026

6.2.9. Rest of the Europe

6.2.9.1. Market size and forecast, by cancer form, 2016-2026

6.2.9.2. Market size and forecast, by application, 2016-2026

6.2.9.3. Comparative market share analysis, 2018 & 2026

6.3. Asia-Pacific

6.3.1. Market size and forecast, by cancer form, 2016-2026

6.3.2. Market size and forecast, by application, 2016-2026

6.3.3. Market size and forecast, by country, 2016-2026

6.3.4. Comparative market share analysis, 2018 & 2026

6.3.5. China

6.3.5.1. Market size and forecast, by cancer form, 2016-2026

6.3.5.2. Market size and forecast, by application, 2016-2026

6.3.5.3. Comparative market share analysis, 2018 & 2026

6.3.6. Japan

6.3.6.1. Market size and forecast, by cancer form, 2016-2026

6.3.6.2. Market size and forecast, by application, 2016-2026

6.3.6.3. Comparative market share analysis, 2018 & 2026

6.3.7. India

6.3.7.1. Market size and forecast, by cancer form, 2016-2026

6.3.7.2. Market size and forecast, by application, 2016-2026

6.3.7.3. Comparative market share analysis, 2018 & 2026

6.3.8. Australia

6.3.8.1. Market size and forecast, by cancer form, 2016-2026

6.3.8.2. Market size and forecast, by application, 2016-2026

6.3.8.3. Comparative market share analysis, 2018 & 2026

6.3.9. South Korea

6.3.9.1. Market size and forecast, by cancer form, 2016-2026

6.3.9.2. Market size and forecast, by application, 2016-2026

6.3.9.3. Comparative market share analysis, 2018 & 2026

6.3.10. Rest of the Asia Pacific

6.3.10.1. Market size and forecast, by cancer form, 2016-2026

6.3.10.2. Market size and forecast, by application, 2016-2026

6.3.10.3. Comparative market share analysis, 2018 & 2026

6.4. LAMEA

6.4.1. Market size and forecast, by cancer form, 2016-2026

6.4.2. Market size and forecast, by application, 2016-2026

6.4.3. Market size and forecast, by country, 2016-2026

6.4.4. Comparative market share analysis, 2018 & 2026

6.4.5. Brazil

6.4.5.1. Market size and forecast, by cancer form, 2016-2026

6.4.5.2. Market size and forecast, by application, 2016-2026

6.4.5.3. Comparative market share analysis, 2018 & 2026

6.4.6. Saudi Arabia

6.4.6.1. Market size and forecast, by cancer form, 2016-2026

6.4.6.2. Market size and forecast, by application, 2016-2026

6.4.6.3. Comparative market share analysis, 2018 & 2026

6.4.7. South Africa

6.4.7.1. Market size and forecast, by cancer form, 2016-2026

6.4.7.2. Market size and forecast, by application, 2016-2026

6.4.7.3. Comparative market share analysis, 2018 & 2026

6.4.8. Rest of LAMEA

6.4.8.1. Market size and forecast, by cancer form, 2016-2026

6.4.8.2. Market size and forecast, by application, 2016-2026

6.4.8.3. Comparative market share analysis, 2018 & 2026

7. Company Profiles

7.1. AdnaGen GmbH

7.1.1. Business overview

7.1.2. Financial performance

7.1.3. Product portfolio

7.1.4. Recent strategic moves & developments

7.1.5. SWOT analysis

7.2. Advanced Cell Diagnostics, Inc.

7.2.1. Business overview

7.2.2. Financial performance

7.2.3. Product portfolio

7.2.4. Recent strategic moves & developments

7.2.5. SWOT analysis

7.3. AVIVA Biosciences Corporation

7.3.1. Business overview

7.3.2. Financial performance

7.3.3. Product portfolio

7.3.4. Recent strategic moves & developments

7.3.5. SWOT analysis

7.4. Celula, Inc.

7.4.1. Business overview

7.4.2. Financial performance

7.4.3. Product portfolio

7.4.4. Recent strategic moves & developments

7.4.5. SWOT analysis

7.5. Epic Sciences Inc.

7.5.1. Business overview

7.5.2. Financial performance

7.5.3. Product portfolio

7.5.4. Recent strategic moves & developments

7.5.5. SWOT analysis

7.6. Fluxion Biosciences, Inc.

7.6.1. Business overview

7.6.2. Financial performance

7.6.3. Product portfolio

7.6.4. Recent strategic moves & developments

7.6.5. SWOT analysis

7.7. Rarecells USA Inc.

7.7.1. Business overview

7.7.2. Financial performance

7.7.3. Product portfolio

7.7.4. Recent strategic moves & developments

7.7.5. SWOT analysis

7.8. Silicon Biosystems, S.p.A.

7.8.1. Business overview

7.8.2. Financial performance

7.8.3. Product portfolio

7.8.4. Recent strategic moves & developments

7.8.5. SWOT analysis

According to a study by the World Health Organization (WHO), cancer is the cause for every one death out of six occurrences. Growing cases of cancers such as breast cancer, lung cancer and others due to poor diet patterns, air pollution, sexually transmitted infections, alcohol consumption. Other types of cancer are liver cancer, pancreas cancer, brain cancer, bladder cancer, colon, and blood cancer. The most common cures for cancer are chemotherapy, radiation, and surgeries. These procedures have an adverse effect on the human body. High doses of radiation and chemotherapy destroy the blood-forming stem cells. Stem cells are the soft tissues of the bone that grow inside the bone marrow. Stem cell transplants restore the blood-forming stem cells. These stem cells grow into platelets, RBCs, and WBCs that are required by the body to fight illness and provide oxygen. Usually, these transplants are done within the family to find the closest match.

Stem Cells for Cancer

Cancer stem cells or CSCs are a subpopulation of cells that has the driving force of carcinogenesis. Characteristics of cancer stem cells are proliferation, and differentiation capabilities and distinctive self-renewal. These characteristics play a vital role in many stages of cancer such as cancer initiation, drug resistance, progression, maintenance, and metastasis or relapse. CSCs have traits that are linked with normal stem cells and are found within hematological cancers or tumors.

Stem Cell-based therapy

According to the World Health Organization (WHO), the most common cause of deaths in women diagnosed with cancer is breast cancer. Global cancer stem cells market is projected to reach up to $896.9 million by the end of 2026 as the stem cell-based cancer therapy and targeted cancerous stem cell therapy are advancing in the medical field. Cell-based therapy is split into allogenic Stem Cell therapy and autologous Stem Cell therapy. Allogenic Hematopoietic Stem Cell Transplantation is more beneficial than the autologous Hematopoietic Stem Cell Transplantation for Breast cancer based on different aspects such as cancer-free graft & immune-mediated Graft vs Tumor effect mediated by the donor’s immune cell.

Successful engraftment rates together with lesser transplant-related mortality and the presence of Graft vs Tumor effect made allogeneic Hematopoietic Stem Cell Transplantation with Reduced Intensity conditioning is the better choice option for the treatment of multiple solid tumors. Due to aforesaid aspects, it is anticipated that allogenic cell therapy will be the rising point for the cancer stem cell market. The global market for stem cell-based cancer therapy is estimated to grow at 9.3% CAGR in 2026 from $440.3 million in 2018.

Advancements in Cancer Stem Cell Transplantation

The prime reason for such huge growth is majorly owed to the rising developments in stem cell therapy of the Asia-Pacific and Europe region. Physicians in Canada are endorsing and promotion of stem cell interventions, which are ethical, legal, and regulatory. U.S. and Canada are leading the cancer stem cell market in the North America region. The North America market is expected to grow over the forecast period and is further projected to generate revenue of $783.8 million by 2026 from its market value of $365.6 million in 2018. While the Asia-Pacific Cancer Stem Cells Market is anticipated to rise to $367.7 Million till 2026 and the Europe Cancer Stem Cells Market is anticipated to generate revenue of $419.5 Million till 2026. Amongst these regions, the Asia-Pacific region is anticipated to be the fastest-growing region for cancer stem cells market. Governing bodies of India, Japan, and other countries are promoting Stem cell transplant by constructing new infrastructure and enlisting new strategies for the launch of centers of stem cells.

The major players in the global cancer stem cell market are introducing several strategies to reinforce their presence in the market

Some of these strategies are introducing new product development and merger & acquisitions. Celula Inc. declared a long term lease agreement In April 2019, for the development of 145,000 square-foot advanced cell manufacturing and research facility in the U.S. Other market players include:

- Advanced Cell Diagnostics Inc.

- Fluxion Biosciences Inc.

- Silicon Biosystems, S.p.A.

- AdnaGen GmbH

- AVIVA Biosciences Corporation

- Epic Sciences Inc.

- Rarecells USA Inc.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com