Steel Processing Market Report

RA08675

Steel Processing Market by Method (Blast Furnace and Electric Arc Furnace), Steel Type (Alloy Steel and Carbon Steel), Product (Flat Steel, Long Steel, and Tubular Steel) End-use Industry (Building & Infrastructure, Automotive, Metal Products, Mechanical Equipment, Transport, Electrical Equipment, and Domestic Appliances), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2022-2031

Global Steel Processing Market Analysis

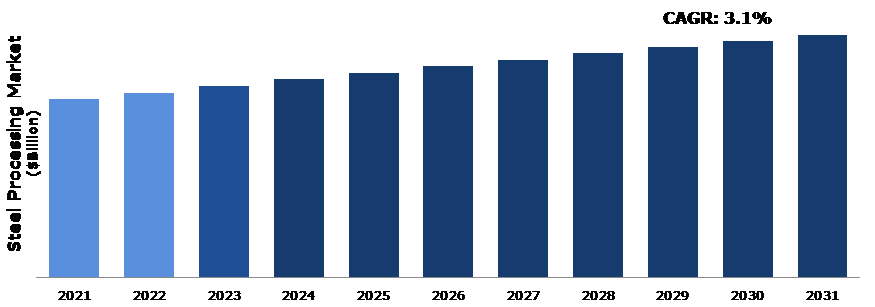

The Global Steel Processing Market Size was $647.7 billion in 2021 and is predicted to grow with a CAGR of 3.1%, by generating a revenue of $884.1 billion by 2031.

Global Steel Processing Market Synopsis

The growth of urbanization and infrastructure development in developing countries has been a major growth factor of the steel processing market. As cities grow and expand, there is a growing demand for steel products such as steel pipes, rods, and beams to construct buildings, bridges, highways, and other infrastructure. Steel is a versatile and durable material that can withstand harsh weather conditions and heavy use that urban infrastructure is subjected to. It is also an affordable and readily available material, making it an attractive choice for construction projects in developing countries.

The steel processing market has experienced significant growth in recent years, with many steel manufacturers investing in new technologies and production methods to meet the growing demand. This trend is expected to continue in the coming years as developing countries continue to invest in infrastructure development and urbanization. These factors are anticipated to boost the steel processing market industry growth in the upcoming years.

However, the demand for steel has been decreasing due to reduced activity in key end-use sectors such as construction, automotive, and infrastructure. This has led to a surplus of steel production capacity, which has put pressure on prices and profit margins for steel manufacturers. Many steel manufacturers are working to differentiate themselves by offering value-added services such as custom fabrication, design assistance, and inventory management. By focusing on these areas, steel manufacturers can build stronger relationships with their customers and mitigate the impact of the challenging market conditions.

Steel is used for various applications, including bridges, pipelines, and transmission towers. With the increasing need for infrastructure development in many countries, the demand for steel is expected to grow. Steel processors can capitalize on this opportunity by expanding their operations and providing high-quality steel products to the infrastructure development industry. The increasing demand for steel presents a significant opportunity for the steel processing market.

As construction activities, automotive production, and infrastructure development continue to grow, the demand for steel is expected to increase in the coming years. Steel processors can take advantage of this opportunity by expanding their operations and providing high-quality steel products to these industries.

According to regional analysis, the Asia-Pacific steel processing market accounted for the highest market share in 2021. The Asia-Pacific region is witnessing significant growth in construction and infrastructure development, which is driving the demand for steel products. Steel is used in the construction of buildings, bridges, roads, and other infrastructure projects, making it a crucial material for economic development.

Steel Processing Overview

Steel processing refers to the various techniques and methods used to transform raw steel into usable products. It includes a range of processes such as casting, forging, rolling, extrusion, drawing, and welding. The process of steel processing typically begins with melting down raw steel in a furnace, which is then formed into shapes or sheets using various techniques. Once the steel has been formed into the desired shape, it may be treated with heat or chemicals to improve its strength or durability.

COVID-19 Impact on Global Steel Processing Market

The COVID-19 pandemic has had a significant impact on the steel processing market. The lockdowns and restrictions on movement imposed by governments around the world have resulted in a decline in demand for steel. This decline in demand has been further exacerbated by the economic slowdown resulting from the pandemic. The construction industry, which is a major consumer of steel, has been affected by the pandemic as well. Many construction projects have been put on hold or delayed, leading to a drop in demand for steel. The automotive industry, which is another major consumer of steel, has also been impacted as car sales have declined.

In addition to the decline in demand, the steel processing market has also had to deal with supply chain disruptions caused by the pandemic. The closure of factories and transport restrictions have led to a shortage of raw materials, making it difficult for steel processors to maintain production levels. Despite these challenges, there have been some signs of recovery in the steel processing market as countries begin to reopen their economies. The demand for steel is expected to increase as construction projects resume and the automotive industry grows. However, the recovery is likely to be slow and uneven, and the long-term impact of the pandemic on the steel processing market remains uncertain.

Growing Construction and Industrial Sector to Drive the Market Growth

The construction industry is a major consumer of steel products. Steel is a versatile and durable material that is used extensively in the construction of buildings, bridges, roads, and other infrastructure projects. As urbanization and population growth continue, the demand for new construction projects is increasing, which in turn drives the demand for steel products. Moreover, technological advancements in the steel processing industry have led to the development of high-quality, high-performance steel products that are more efficient and cost-effective. For example, advanced steel products such as high-strength steel and galvanized steel are being increasingly used in construction projects to improve their durability and longevity.

Additionally, initiatives by governments and private organizations to promote sustainable and eco-friendly construction practices have also led to the growth of the steel processing market. Steel is a recyclable material, and its use in construction can significantly reduce the carbon footprint of buildings and infrastructure projects. The construction industry's growth is a significant driver of the steel processing market, and as demand for new infrastructure and housing projects continues to increase, the demand for steel products will also continue to rise.

To know more about global steel processing market drivers, get in touch with our analysts here.

Environmental Regulations to Restrain the Market Growth

The steel processing industry is subject to strict environmental regulations due to the high level of pollution it generates. These regulations aim to reduce the impact of industry on the environment and protect human health. Compliance with these regulations can be costly and time-consuming for steel processing companies. They may have to invest in new technologies and equipment to reduce emissions and meet environmental standards. This can result in higher production costs and lower profitability, which can be a significant challenge for companies operating in a highly competitive market, which is anticipated to hamper the steel processing market growth.

Increasing Demand for Steel to Drive Excellent Opportunities

As the demand for steel increases, the steel processing market is expected to grow as well. Steel processing involves transforming raw steel into a finished product that can be used for various applications, including construction, automotive production, and infrastructure development. With the growing demand for steel in these industries, the steel processing market is poised for growth. In the construction industry, steel is used for structural applications, such as beams, columns, and other components.

With the increase in construction activities around the world, the demand for steel is expected to continue growing. This presents an opportunity for steel processors to expand their operations and meet the growing demand for steel products. In the automotive industry, steel is used for various applications, including body panels, frames, and engine components. With the increase in automotive production around the world, the demand for steel is also expected to grow.

To know more about global steel processing market opportunities, get in touch with our analysts here.

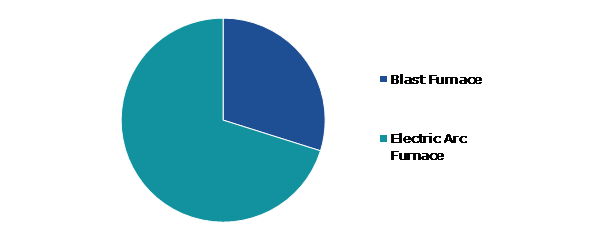

Global Steel Processing Market, by Method

Based on the method, the market has been divided into blast furnace and electric arc furnace. Among these, the electric arc furnace sub-segment accounted for the highest market share in 2021.

Global Steel Processing Market Share, by Method, 2021

Source: Research Dive Analysis

The electric arc furnace sub-type accounted for highest market size in 2021 and it is anticipated to show the fastest growth in 2031. Electric Arc Furnace (EAF) are widely used for steelmaking, particularly for producing specialty steels and alloys, due to their flexibility, energy efficiency, and low capital costs compared to traditional blast furnace technology. Additionally, there is a growing trend towards sustainability and reducing carbon emissions in the steel industry, and EAFs are seen as a more environmentally friendly option as they use recycled scrap metal as their primary input material. This makes EAFs a preferred choice for companies looking to reduce their carbon footprint and meet sustainability goals.

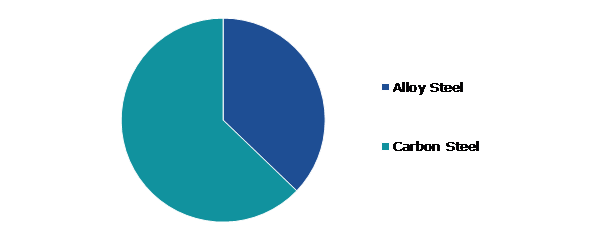

Global Steel Processing Market, by Steel Type

Based on steel type, the market has been divided into alloy steel and carbon steel. Among these, the carbon steel sub-segment accounted for highest revenue share in 2021.

Global Steel Processing Market Size, by Steel Type, 2021

Source: Research Dive Analysis

The carbon steel sub-segment accounted for the largest market share in 2021. Carbon steel is a cost-effective material compared to other alloys, making it an attractive option for manufacturers. Carbon steel can be used in a variety of applications, including construction, automotive, and manufacturing. Carbon steel is widely available and easy to source, making it a popular choice among manufacturers. Carbon steel is a ductile and tough material that can withstand high temperatures and pressures, making it suitable for demanding applications. Carbon steel is easy to process and fabricate, allowing manufacturers to produce complex shapes and structures. Carbon steel has a high strength-to-weight ratio, making it a popular choice for applications that require strength without adding significant weight. These factors are anticipated to boost the growth of carbon steel sub-segment during the analysis timeframe.

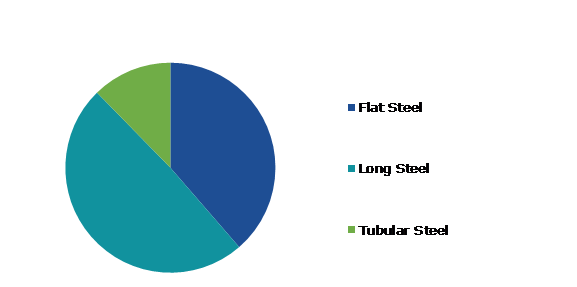

Global Steel Processing Market, by Product

Based on product, the market has been divided into flat steel, long steel, and tubular steel. Among these, the long steel sub-segment accounted for the highest revenue share in 2021.

Global Steel Processing Market Trends, by Product, 2021

Source: Research Dive Analysis

The long steel sub-segment accounted for the largest market share in 2021. The demand for long steel products is closely linked to economic growth, as it is used in the construction, infrastructure, and manufacturing sectors. A strong economy with high levels of investment and construction activity will drive the demand for long steel products. The growth of urban areas and the increase in infrastructure development in these areas will also drive demand for long steel products.

Urbanization leads to the construction of buildings, bridges, and other infrastructure projects that require long steel products. The use of advanced technologies in the production and processing of long steel products can lead to increased efficiency, lower costs, and higher quality products. This can give companies a competitive advantage in the market. These factors are anticipated to boost the growth of the long steel sub-segment during the analysis timeframe.

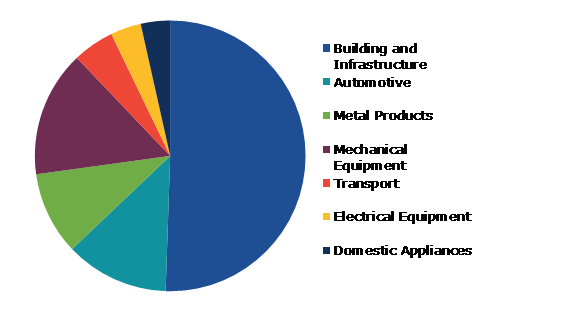

Global Steel Processing Market, by End-use Industry

Based on end-use industry, the market has been divided into building & infrastructure, automotive, metal products, mechanical equipment, transport, electrical equipment, and domestic appliances. Among these, the building and infrastructure sub-segment accounted for highest revenue share in 2021.

Global Steel Processing Market Analysis, by End-use Industry, 2021

Source: Research Dive Analysis

The building & infrastructure sub-segment accounted for the largest market share in 2021. This segment includes construction activities such as building construction, road construction, and bridge construction. Steel is a versatile material that is widely used in the building and infrastructure segment because of its strength, durability, and cost-effectiveness. In building construction, steel is used for a variety of applications such as structural framing, roofing, cladding, and reinforcement.

Steel framing is lightweight, easy to install, and can be fabricated off-site, which makes it a popular choice for high-rise buildings and large industrial structures. Steel roofing and cladding provide excellent weather resistance and require minimal maintenance. These factors are anticipated to boost the growth of building and infrastructure sub-segment during the analysis timeframe.

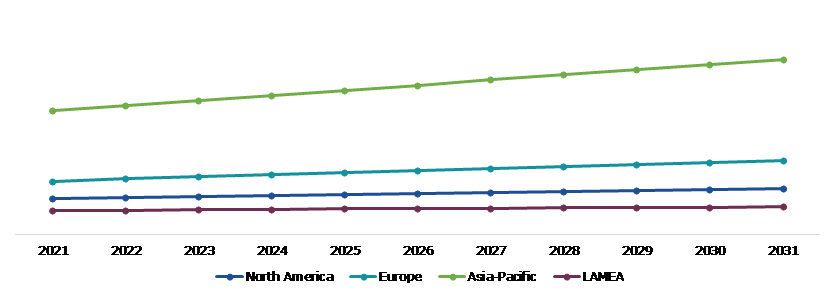

Global Steel Processing Market, Regional Insights

The steel processing market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Global Steel Processing Market Size & Forecast, by Region, 2021-2031 ($Billion)

Source: Research Dive Analysis

The Market for Steel Processing in Asia-Pacific was the Most Dominant

The Asia-Pacific steel processing market accounted for the highest market share in 2021. The Asia-Pacific region has a large and growing population that is increasingly urbanizing. As people move to cities, the demand for steel products such as appliances and other consumer goods also increases, which drives the demand for steel processing. China is the largest steel-producing country globally, and its steel industry accounts for approximately half of the world's total steel production. China's steel processing market is driven by its strong domestic demand for steel, which is used in construction, infrastructure, automotive, and other industries.

The steel processing industry is constantly evolving, with new technologies emerging that allow for faster and more efficient production of steel products. As these technologies become more widely adopted, they are helping the growth of the Asia-Pacific steel processing market. Governments in the Asia-Pacific region are implementing policies and initiatives aimed at promoting economic growth and development, which often include investments in infrastructure and construction projects. These initiatives are driving the demand for steel products and supporting the growth of the steel processing industry.

Competitive Scenario in the Global Steel Processing Market

Investment and agreement are common strategies followed by major market players. For instance, in July 2020, JSW Steel proclaimed its plans to expand the capacity to produce around 27 million ton of crude steel by 2022 from about 18 million ton in 2020.

Source: Research Dive Analysis

Some of the leading steel processing market players are China Baowu Group, ArcelorMittal, Ansteel Group, Nippon Steel Corporation, Shagang Group, POSCO, HBIS Group, Jianlong Group, Shougang Group, and Tata Steel Group.

| Aspect | Particulars |

| Historical Market Estimations | 2021 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Method |

|

| Segmentation by Steel Type |

|

| Segmentation by Product |

|

| Segmentation by End-use Industry |

|

| Key Companies Profiled |

|

Q1. What is the size of the global steel processing market?

A. The size of the global steel processing market was over $647.7 billion in 2021 and is projected to reach $884.1 billion by 2031.

Q2. Which are the major companies in the steel processing market?

A. China Baowu Group, ArcelorMittal, Ansteel Group,are some of the key players in the global steel processing market.

Q3. Which region, among others, possesses greater investment opportunities in the near future?

A. The Asia-Pacific region possesses great investment opportunities for investors to witness the most promising growth in the future.

Q4. What will be the growth rate of the Asia-Pacific steel processing market?

A. Asia-Pacific steel processing market is anticipated to grow at 3.5% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Nippon Steel Corporation, and Shagang Group are the companies investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global steel processing market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on steel processing market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Steel Processing Market Analysis, by Method

5.1.Overview

5.2.Blast Furnace

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region,2021-2031

5.2.3.Market share analysis, by country,2021-2031

5.3.Electric Arc Furnace

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region,2021-2031

5.3.3.Market share analysis, by country,2021-2031

5.4.Research Dive Exclusive Insights

5.4.1.Market attractiveness

5.4.2.Competition heatmap

6.Steel Processing Market Analysis, by Steel Type

6.1.Overview

6.2.Alloy Steel

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region,2021-2031

6.2.3.Market share analysis, by country,2021-2031

6.3.Carbon Steel

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.2.Market size analysis, by region,2021-2031

6.3.3.Market share analysis, by country,2021-2031

6.4.Research Dive Exclusive Insights

6.4.1.Market attractiveness

6.4.2.Competition heatmap

7.Steel Processing Market Analysis, by Product

7.1.Overview

7.2.Flat Steel

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region,2021-2031

7.2.3.Market share analysis, by country,2021-2031

7.3.Long Steel

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region,2021-2031

7.3.3.Market share analysis, by country,2021-2031

7.4.Tubular Steel

7.4.1.Definition, key trends, growth factors, and opportunities

7.4.2.Market size analysis, by region,2021-2031

7.4.3.Market share analysis, by country,2021-2031

7.5.Research Dive Exclusive Insights

7.5.1.Market attractiveness

7.5.2.Competition heatmap

8.Steel Processing Market Analysis, by End-use Industry

8.1.Overview

8.2.Building and Infrastructure

8.2.1.Definition, key trends, growth factors, and opportunities

8.2.2.Market size analysis, by region,2021-2031

8.2.3.Market share analysis, by country,2021-2031

8.3.Automotive

8.3.1.Definition, key trends, growth factors, and opportunities

8.3.2.Market size analysis, by region,2021-2031

8.3.3.Market share analysis, by country,2021-2031

8.4.Metal Products

8.4.1.Definition, key trends, growth factors, and opportunities

8.4.2.Market size analysis, by region,2021-2031

8.4.3.Market share analysis, by country,2021-2031

8.5.Mechanical Equipment

8.5.1.Definition, key trends, growth factors, and opportunities

8.5.2.Market size analysis, by region,2021-2031

8.5.3.Market share analysis, by country,2021-2031

8.6.Transport

8.6.1.Definition, key trends, growth factors, and opportunities

8.6.2.Market size analysis, by region,2021-2031

8.6.3.Market share analysis, by country,2021-2031

8.7.Electrical Equipment

8.7.1.Definition, key trends, growth factors, and opportunities

8.7.2.Market size analysis, by region,2021-2031

8.7.3.Market share analysis, by country,2021-2031

8.8.Domestic Appliances

8.8.1.Definition, key trends, growth factors, and opportunities

8.8.2.Market size analysis, by region,2021-2031

8.8.3.Market share analysis, by country,2021-2031

8.9.Research Dive Exclusive Insights

8.9.1.Market attractiveness

8.9.2.Competition heatmap

9.Steel Processing Market, by Region

9.1.North America

9.1.1.U.S.

9.1.1.1.Market size analysis, by Method, 2021-2031

9.1.1.2.Market size analysis, by Steel Type, 2021-2031

9.1.1.3.Market size analysis, by Product, 2021-2031

9.1.1.4.Market size analysis, by End-use Industry, 2021-2031

9.1.2.Canada

9.1.2.1.Market size analysis, by Method, 2021-2031

9.1.2.2.Market size analysis, by Steel Type, 2021-2031

9.1.2.3.Market size analysis, by Product, 2021-2031

9.1.2.4.Market size analysis, by End-use Industry, 2021-2031

9.1.3.Mexico

9.1.3.1.Market size analysis, by Method, 2021-2031

9.1.3.2.Market size analysis, by Steel Type, 2021-2031

9.1.3.3.Market size analysis, by Product, 2021-2031

9.1.3.4.Market size analysis, by End-use Industry, 2021-2031

9.1.4.Research Dive Exclusive Insights

9.1.4.1.Market attractiveness

9.1.4.2.Competition heatmap

9.2.Europe

9.2.1.Germany

9.2.1.1.Market size analysis, by Method, 2021-2031

9.2.1.2.Market size analysis, by Steel Type, 2021-2031

9.2.1.3.Market size analysis, by Product, 2021-2031

9.2.1.4.Market size analysis, by End-use Industry, 2021-2031

9.2.2.UK

9.2.2.1.Market size analysis, by Method, 2021-2031

9.2.2.2.Market size analysis, by Steel Type, 2021-2031

9.2.2.3.Market size analysis, by Product, 2021-2031

9.2.2.4.Market size analysis, by End-use Industry, 2021-2031

9.2.3.France

9.2.3.1.Market size analysis, by Method, 2021-2031

9.2.3.2.Market size analysis, by Steel Type, 2021-2031

9.2.3.3.Market size analysis, by Product, 2021-2031

9.2.3.4.Market size analysis, by End-use Industry, 2021-2031

9.2.4.Spain

9.2.4.1.Market size analysis, by Method, 2021-2031

9.2.4.2.Market size analysis, by Steel Type, 2021-2031

9.2.4.3.Market size analysis, by Product, 2021-2031

9.2.4.4.Market size analysis, by End-use Industry, 2021-2031

9.2.5.Italy

9.2.5.1.Market size analysis, by Method, 2021-2031

9.2.5.2.Market size analysis, by Steel Type, 2021-2031

9.2.5.3.Market size analysis, by Product, 2021-2031

9.2.5.4.Market size analysis, by End-use Industry, 2021-2031

9.2.6.Rest of Europe

9.2.6.1.Market size analysis, by Method, 2021-2031

9.2.6.2.Market size analysis, by Steel Type, 2021-2031

9.2.6.3.Market size analysis, by Product, 2021-2031

9.2.6.4.Market size analysis, by End-use Industry, 2021-2031

9.2.7.Research Dive Exclusive Insights

9.2.7.1.Market attractiveness

9.2.7.2.Competition heatmap

9.3.Asia Pacific

9.3.1.China

9.3.1.1.Market size analysis, by Method, 2021-2031

9.3.1.2.Market size analysis, by Steel Type, 2021-2031

9.3.1.3.Market size analysis, by Product, 2021-2031

9.3.1.4.Market size analysis, by End-use Industry, 2021-2031

9.3.2.Japan

9.3.2.1.Market size analysis, by Method, 2021-2031

9.3.2.2.Market size analysis, by Steel Type, 2021-2031

9.3.2.3.Market size analysis, by Product, 2021-2031

9.3.2.4.Market size analysis, by End-use Industry, 2021-2031

9.3.3.India

9.3.3.1.Market size analysis, by Method, 2021-2031

9.3.3.2.Market size analysis, by Steel Type, 2021-2031

9.3.3.3.Market size analysis, by Product, 2021-2031

9.3.3.4.Market size analysis, by End-use Industry, 2021-2031

9.3.4.Australia

9.3.4.1.Market size analysis, by Method, 2021-2031

9.3.4.2.Market size analysis, by Steel Type, 2021-2031

9.3.4.3.Market size analysis, by Product, 2021-2031

9.3.4.4.Market size analysis, by End-use Industry, 2021-2031

9.3.5.South Korea

9.3.5.1.Market size analysis, by Method, 2021-2031

9.3.5.2.Market size analysis, by Steel Type, 2021-2031

9.3.5.3.Market size analysis, by Product, 2021-2031

9.3.5.4.Market size analysis, by End-use Industry, 2021-2031

9.3.6.Rest of Asia Pacific

9.3.6.1.Market size analysis, by Method, 2021-2031

9.3.6.2.Market size analysis, by Steel Type, 2021-2031

9.3.6.3.Market size analysis, by Product, 2021-2031

9.3.6.4.Market size analysis, by End-use Industry, 2021-2031

9.3.7.Research Dive Exclusive Insights

9.3.7.1.Market attractiveness

9.3.7.2.Competition heatmap

9.4.LAMEA

9.4.1.Brazil

9.4.1.1.Market size analysis, by Method, 2021-2031

9.4.1.2.Market size analysis, by Steel Type, 2021-2031

9.4.1.3.Market size analysis, by Product, 2021-2031

9.4.1.4.Market size analysis, by End-use Industry, 2021-2031

9.4.2.Saudi Arabia

9.4.2.1.Market size analysis, by Method, 2021-2031

9.4.2.2.Market size analysis, by Steel Type, 2021-2031

9.4.2.3.Market size analysis, by Product, 2021-2031

9.4.2.4.Market size analysis, by End-use Industry, 2021-2031

9.4.3.UAE

9.4.3.1.Market size analysis, by Method, 2021-2031

9.4.3.2.Market size analysis, by Steel Type, 2021-2031

9.4.3.3.Market size analysis, by Product, 2021-2031

9.4.3.4.Market size analysis, by End-use Industry, 2021-2031

9.4.4.South Africa

9.4.4.1.Market size analysis, by Method, 2021-2031

9.4.4.2.Market size analysis, by Steel Type, 2021-2031

9.4.4.3.Market size analysis, by Product, 2021-2031

9.4.4.4.Market size analysis, by End-use Industry, 2021-2031

9.4.5.Rest of LAMEA

9.4.5.1.Market size analysis, by Method, 2021-2031

9.4.5.2.Market size analysis, by Steel Type, 2021-2031

9.4.5.3.Market size analysis, by Product, 2021-2031

9.4.5.4.Market size analysis, by End-use Industry, 2021-2031

9.4.6.Research Dive Exclusive Insights

9.4.6.1.Market attractiveness

9.4.6.2.Competition heatmap

10.Competitive Landscape

10.1.Top winning strategies, 2021

10.1.1.By strategy

10.1.2.By year

10.2.Strategic overview

10.3.Market share analysis, 2021

11.Company Profiles

11.1.China Baowu Group

11.1.1.Overview

11.1.2.Business segments

11.1.3.Product portfolio

11.1.4.Financial performance

11.1.5.Recent developments

11.1.6.SWOT analysis

11.2.ArcelorMittal

11.2.1.Overview

11.2.2.Business segments

11.2.3.Product portfolio

11.2.4.Financial performance

11.2.5.Recent developments

11.2.6.SWOT analysis

11.3.Ansteel Group

11.3.1.Overview

11.3.2.Business segments

11.3.3.Product portfolio

11.3.4.Financial performance

11.3.5.Recent developments

11.3.6.SWOT analysis

11.4.Nippon Steel Corporation

11.4.1.Overview

11.4.2.Business segments

11.4.3.Product portfolio

11.4.4.Financial performance

11.4.5.Recent developments

11.4.6.SWOT analysis

11.5.Shagang Group

11.5.1.Overview

11.5.2.Business segments

11.5.3.Product portfolio

11.5.4.Financial performance

11.5.5.Recent developments

11.5.6.SWOT analysis

11.6.POSCO

11.6.1.Overview

11.6.2.Business segments

11.6.3.Product portfolio

11.6.4.Financial performance

11.6.5.Recent developments

11.6.6.SWOT analysis

11.7.HBIS Group

11.7.1.Overview

11.7.2.Business segments

11.7.3.Product portfolio

11.7.4.Financial performance

11.7.5.Recent developments

11.7.6.SWOT analysis

11.8.Jianlong Group

11.8.1.Overview

11.8.2.Business segments

11.8.3.Product portfolio

11.8.4.Financial performance

11.8.5.Recent developments

11.8.6.SWOT analysis

11.9.Shougang Group

11.9.1.Overview

11.9.2.Business segments

11.9.3.Product portfolio

11.9.4.Financial performance

11.9.5.Recent developments

11.9.6.SWOT analysis

11.10.Tata Steel Group

11.10.1.Overview

11.10.2.Business segments

11.10.3.Product portfolio

11.10.4.Financial performance

11.10.5.Recent developments

11.10.6.SWOT analysis

Steel processing involves procedures and methodologies to transform iron ore and scrap into steel that can be used for specific manufacturing processes. In these processes, impurities present in iron ore such as nitrogen, sulfur, silicon, phosphorous, etc., are removed. Along with this, important metalloid elements like manganese, vanadium, chromium, nickel, etc., are added to the iron ore so as to produce manufacturing-purpose steel.

Forecast Analysis of the Steel Processing Market

The growing pace of urbanization and infrastructure development in developing countries of the world is predicted to be the primary growth driver of the global steel processing market in the forecast period. Additionally, increasing automobile production and construction businesses across the world is anticipated to push the market forward. Along with this, increasing demand for steel from the global industrial sector is projected to offer numerous growth and investment opportunities to the market in the analysis timeframe. However, environmental regulations with respect to steel processing are estimated to create hurdles in the full-fledged growth of the steel processing market in the coming period.

Regionally, the steel processing market in the Asia-Pacific region is expected to be the most dominant by 2031. Growing demand for steel products from the consumer goods industry is expected to be the leading factor behind the growth of the market in this region.

According to the report published by Research Dive, the global steel processing market is expected to gather a revenue of $884.1 billion by 2031 and grow at 3.1% CAGR in the 2022–2031 timeframe. Some prominent market players include China Baowu Group, Shagang Group, Jianlong Group, ArcelorMittal, POSCO, Shougang Group, Ansteel Group, HBIS Group, Tata Steel Group, Nippon Steel Corporation, and many others.

Covid-19 Impact on the Steel Processing Market

The outbreak of the Covid-19 pandemic has had a massive negative effect on almost all industries and businesses across the world. The steel processing market, too, faced a negative impact of the pandemic. The disruptions in the global supply chains immensely affected the production of steel in industries around the world. Also, since almost all the manufacturing industries were shut down during the lockdown, the demand for steel went down drastically. Both these factors brought down the growth rate of the steel processing market.

Significant Market Developments

The significant companies operating in the industry are adopting numerous growth strategies & business tactics such as partnerships, collaborations, mergers & acquisitions, and launches to maintain a robust position in the overall market, thus helping the steel processing market to flourish. For instance:

- In November 2021, PSI Metals, a management solutions provider, announced that it was partnering with Smart Steel Technologies, an operating system developer for steel production. This partnership is aimed at developing AI-based applications for the steel production industry. The partnership is expected to help both the companies to increase their footprint in the steel processing industry substantially in the near future.

- In October 2022, Steel Dynamics, a leading steel producing company, announced the acquisition of ROCA Acero, a scrap metal recycling company. This acquisition by Steel Dynamics is expected to increase its market share in the next few years.

- In April 2023, BICO Steel, a steel processing company, announced the acquisition of RE Metal Finishing, a metal finishing services provider. This acquisition is expected to help BICO steel to expand its steel processing operations and consolidate its lead over its competitors in the industry in the coming period.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com