Gastric Cancer Market Report

RA08663

Gastric Cancer Market by Disease Type (Adenocarcinoma, Lymphoma, Gastrointestinal Stromal Tumor, Carcinoid Tumor, and Others), Treatment Type (Immunotherapy, Targeted Therapy, Chemotherapy, and Radiation Therapy and Surgery), Drug Class Outlook (PD-1/PD-L1 Inhibitors, HER2 Antagonists, VEGFR2 Antagonists, and Others), Route of Administration (Oral and Injectable), Distribution Channel (Hospital Pharmacies, Specialty & Retail Pharmacies, and Others), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2022-2031

Global Gastric Cancer Market Analysis

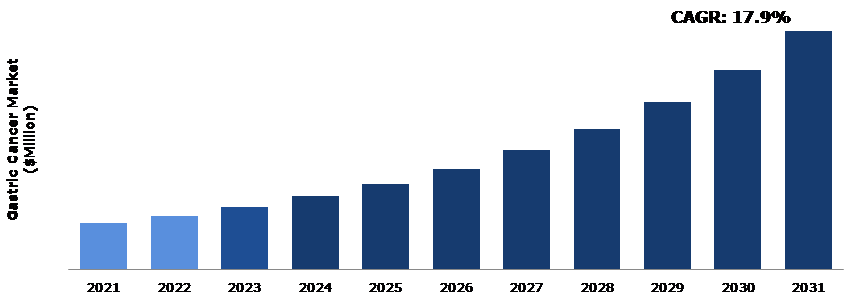

The Global Gastric Cancer Market Size was $2,100.00 million in 2021 and is predicted to grow with a CAGR of 17.9%, by generating a revenue of $10,737.00 million by 2031.

Global Gastric Cancer Market Synopsis

The major factors driving the gastric cancer market include increasing prevalence of gastric cancer worldwide, advancements in diagnostic and treatment technologies, increasing healthcare expenditure, and a growing aging population. Moreover, advancements in diagnostic technologies such as endoscopy, biopsy, and imaging techniques have facilitated early detection and diagnosis of gastric cancer, which can improve patient outcomes and survival rates. Treatment options for gastric cancer include surgery, chemotherapy, radiation therapy, targeted therapy, and immunotherapy. Advances in these treatment options has led to improved outcomes and increase in demand for these treatments. The growing aging population, particularly in developed countries, is also a significant driver of the gastric cancer market, as age is a risk factor for the disease. These factors are anticipated to boost the gastric cancer industry growth in the upcoming years.

However, lack of awareness about gastric cancer is one of the key factors that is expected to restrain the growth of the gastric cancer market. Gastric cancer is not as well-known as other types of cancer, and its symptoms can often be vague and easily mistaken for other less serious conditions. Moreover, there is also a lack of awareness among healthcare professionals about the latest diagnostic and treatment options for gastric cancer. All these factors are projected to hamper the gastric cancer market growth in the upcoming years.

Minimally invasive procedures, such as laparoscopic and robotic-assisted surgery, have been proved to be effective in the treatment of gastric cancer and can offer benefits such as faster recovery time, less pain, and reduced hospital stays. The adoption of these procedures is expected to increase as technology advances and more surgeons become trained in these techniques. The growing awareness and screening programs for gastric cancer is also predicted to provide opportunities for the market players. The gastric cancer market presents several opportunities for growth, including the development of new targeted therapies, the adoption of minimally invasive surgical procedures, and increased awareness and screening programs.

According to regional analysis, the Asia-Pacific gastric cancer market size accounted for the largest market share in 2021, due to the high prevalence of gastric cancer in this region. Gastric cancer is one of the leading causes of cancer-related deaths in Asia-Pacific, with a higher incidence rate compared to other regions across the world.

Gastric Cancer Market Overview

Gastric cancer, also known as stomach cancer, is a type of cancer that develops in the lining of the stomach. Gastric cancer can be classified into different types based on the location of the tumor in the stomach and the type of cells it affects. The two most common types are adenocarcinoma, which develops in the glandular cells of the stomach lining, and lymphoma, which develops in the immune system cells of the stomach. There are several risk factors that have been identified, including age (most cases occur in people over the age of 50), a family history of stomach cancer, smoking, a diet high in salted or smoked foods, and chronic infection with the bacteria Helicobacter pylori.

COVID-19 Impact on Global Gastric Cancer Market

The COVID-19 pandemic had a significant impact on the healthcare industry worldwide, including the gastric cancer market. The pandemic disrupted the global supply chain, leading to shortages of raw materials and delay in the delivery of finished products. The pandemic also led to the postponement or cancellation of elective surgeries and other medical procedures, which affected the diagnosis and treatment of gastric cancer patients. Moreover, the covid-19 impact on gastric cancer market had reduced healthcare spending in many countries, as resources had been redirected to pandemic-related measures. This affected the development of new drugs and therapies for gastric cancer, as well as the availability of existing treatments. Many pharmaceutical companies faced challenges in securing the raw materials and components needed to manufacture their products, which resulted in delays in drug production and distribution.

However, despite the challenges posed by the pandemic, the gastric cancer market is expected to continue to grow in the post-pandemic period. This growth is driven by factors such as an aging population, increasing incidence of gastric cancer, and the development of new therapies and treatments.

Growing Prevalence of Gastric Cancer to Drive the Market Growth

The increase in prevalence of gastric cancer is expected to drive the demand for new and more effective treatments. Gastric cancer is a major global health problem, with an estimated one million new cases diagnosed each year. Several factors contribute to the increasing incidence of gastric cancer, including aging population, unhealthy lifestyle habits such as smoking and poor dietary choices, and infections with Helicobacter pylori, a bacterium that can cause chronic inflammation of the stomach lining. The development of targeted therapies and immunotherapies, in particular, has proven to be efficient in treating gastric cancer and is expected to drive the market in the upcoming years. The demand for effective treatments is expected to drive growth of the market, particularly in the areas of targeted therapies and immunotherapies.

To know more about global gastric cancer market drivers, get in touch with our analysts here.

High Cost of Treatment for Gastric Cancer to Restrain the Market Growth

The high cost of treating gastric cancer is one of the key factors restraining the growth of the gastric cancer market. The treatment of gastric cancer involves a combination of surgery, chemotherapy, radiation therapy, and targeted therapy. Moreover, the need for ongoing monitoring and follow-up care after treatment can further add to the cost of treatment. The high cost of treatment can also lead to limited access to care, particularly in low- and middle-income countries, where healthcare resources may be limited. This can result in delayed diagnosis and treatment, which can have a negative impact on patient outcomes. All these are the major factors anticipated to hamper the gastric cancer market growth during the forecast period.

Rising Healthcare Expenditure to Drive Excellent Opportunities in the Market

The increase in investment in R&D for gastric cancer treatments has led to the discovery of new and more effective treatments, which can help improve patient outcomes. In addition, the rising healthcare expenditure has also led to the development of better diagnostic tools and screening techniques for early detection of gastric cancer, which can lead to better prognosis and survival rates. Furthermore, the increase in prevalence of gastric cancer globally, especially in developing countries, provides a significant opportunity for pharmaceutical companies to expand their market and develop new treatments for this disease. These factors are projected to create several growth opportunities for the key players operating in the market in the future.

To know more about global gastric cancer market opportunities, get in touch with our analysts here.

Global Gastric Cancer Market, by Disease Type

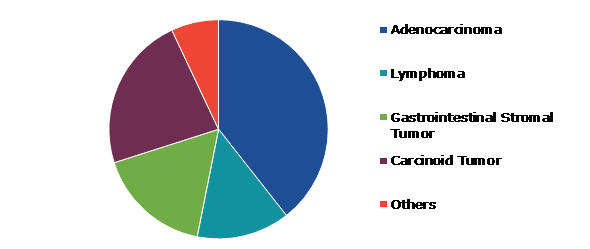

Based on disease type, the market has been divided into adenocarcinoma, lymphoma, gastrointestinal stromal tumor, carcinoid tumor, and others. Among these, the adenocarcinoma sub-segment accounted for the highest market share in 2021 and is anticipated to show the fastest growth during the forecast period.

Global Gastric Cancer Market Share, by Disease Type, 2021

Source: Research Dive Analysis

The adenocarcinoma sub-segment accounted for the largest gastric cancer market share in 2021 and is anticipated to witness the fastest growth in 2031. Adenocarcinoma is the most common type of gastric cancer, accounting for approximately 95% of cases worldwide. Gastric cancer incidence rates vary across regions and populations, though the incidence of gastric cancer has been increasing in various regions across the world including Asia-Pacific, Europe, and North America. This is expected to drive demand for treatments and diagnostic tools for adenocarcinoma. There have been advances in the treatment of gastric cancer, including the development of targeted therapies and immunotherapies. These therapies can potentially improve outcomes for patients with adenocarcinoma, which is predicted to drive the market growth.

Global Gastric Cancer Market, by Treatment Type

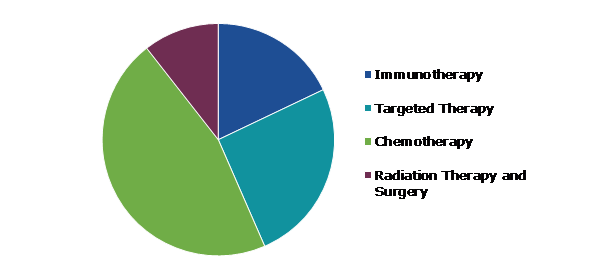

Based on treatment type, the market has been divided into immunotherapy, targeted therapy, chemotherapy, and radiation therapy and surgery. Among these, the chemotherapy sub-segment accounted for the highest revenue share in 2021.

Global Gastric Cancer Market Size, by Treatment Type, 2021

Source: Research Dive Analysis

The chemotherapy sub-segment accounted for the largest gastric cancer market share in 2021. Gastric cancer, also known as stomach cancer, is a type of cancer that originates in the cells of the stomach. Chemotherapy is one of the main treatments for gastric cancer and involves the use of drugs to kill cancer cells. Chemotherapy works by targeting rapidly dividing cells, including cancer cells. It can be used before or after surgery, or as the primary treatment for advanced gastric cancer. Chemotherapy can also be combined with other treatments, such as radiation therapy and targeted therapy, to increase its effectiveness. These factors are anticipated to boost the growth of the chemotherapy sub-segment during the forecast timeframe.

Global Gastric Cancer Market, by Drug Class Outlook

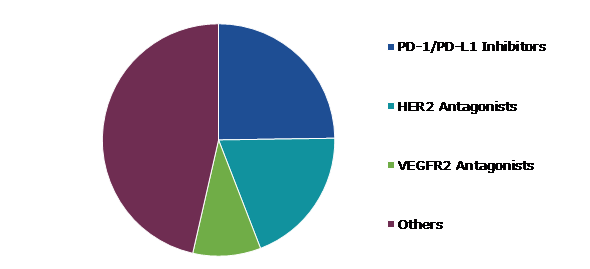

Based on drug class outlook, the market has been divided into PD-1/PD-L1 inhibitors, HER2 antagonists, VEGFR2 antagonists, and others. Among these, the PD-1/PD-L1 inhibitors sub-segment is estimated to show the fastest growth during the forecast period.

Global Gastric Cancer Market Trends, by Drug Class Outlook, 2021

Source: Research Dive Analysis

The PD-1/PD-L1 inhibitors sub-segment is estimated to show the fastest growth during the forecast period. PD-1/PD-L1 inhibitors are a type of immunotherapy that can help the body's immune system recognize and attack cancer cells. PD-1/PD-L1 inhibitors work by blocking the interaction between the PD-1 protein on T cells and the PD-L1 protein on cancer cells. This interaction can suppress the immune system's ability to attack cancer cells. By blocking this interaction, PD-1/PD-L1 inhibitors can allow the immune system to mount a more effective response against cancer cells. These factors are anticipated to boost the growth of the PD-1/PD-L1 inhibitors sub-segment during the forecast years.

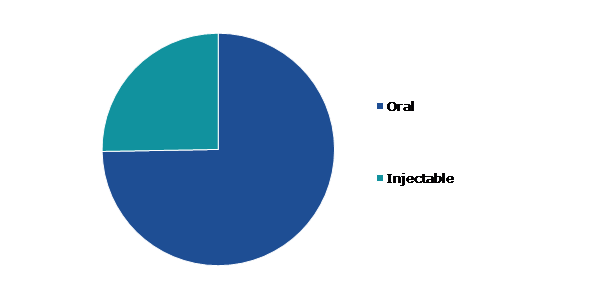

Global Gastric Cancer Market, by Route of Administration

Based on route of administration, the market has been divided into oral and injectable. Among these, the oral sub-segment accounted for the largest market share in 2021.

Global Gastric Cancer Market Growth, by Route of Administration, 2021

Source: Research Dive Analysis

The oral sub-segment accounted for the largest market share in 2021. Gastric cancer is a type of cancer that begins in the stomach and it can affect various parts of the stomach, including the oral segment. The oral segment of the stomach refers to the part of the stomach that is closest to the esophagus. The oral segment growth is driven by the need for early detection and effective treatment options. Early detection is critical for successful treatment outcomes, and there is a growing demand for minimally invasive diagnostic techniques that can accurately detect oral segment gastric cancer at an early stage. These factors are anticipated to boost the growth of oral sub-segment during the forecast period.

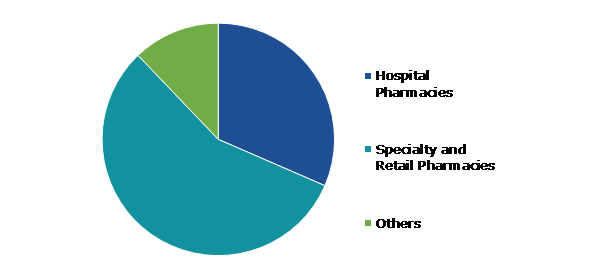

Global Gastric Cancer Market, by Distribution Channel

Based on distribution channel, the market has been divided into hospital pharmacies, specialty & retail pharmacies, and others. Among these, the specialty & retail pharmacies sub-segment accounted for the largest market share in 2021.

Global Gastric Cancer Market Analysis, by Distribution Channel, 2021

Source: Research Dive Analysis

The specialty & retail pharmacies sub-segment accounted for the largest market share in 2021. Gastric cancer is the fifth most common cancer and the third leading cause of cancer-related deaths globally. Therefore, there is a growing demand for effective treatments for gastric cancer, and specialty and retail pharmacies play a crucial role in the offering these treatments. Specialty pharmacies, in particular, are well-suited for distributing treatments for gastric cancer because they have expertise in managing complex therapies, providing patient education and support, and coordinating with healthcare providers. These factors are anticipated to boost the growth of specialty & retail pharmacies sub-segment in the upcoming years.

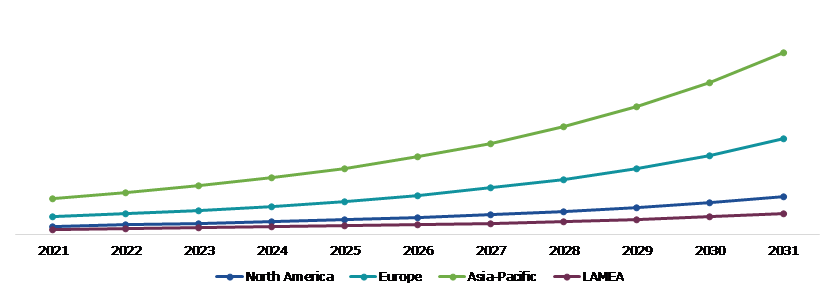

Global Gastric Cancer Market, Regional Insights

The gastric cancer market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Global Gastric Cancer Market Size & Forecast, by region, 2021-2031 (USD Million)

Source: Research Dive Analysis

The Market for Gastric Cancer in Asia-Pacific was the Most Dominant

The Asia-Pacific gastric cancer market analysis accounted for the largest market share in 2021. Asia-Pacific is the largest market for gastric cancer due to several factors such as the high incidence of gastric cancer, a large population, increasing awareness and diagnosis of the disease, and rising healthcare expenditure. Several countries in the region such as Japan, China, South Korea, and India have a high incidence of gastric cancer, which is driving the demand for diagnostic and treatment options. Increasing awareness about gastric cancer and its risk factors among the population, along with the availability of advanced diagnostic technologies such as endoscopy and imaging techniques, is also driving the regional market growth. Furthermore, the increasing healthcare expenditure in the region, especially in emerging countries, is boosting the demand for better treatment options and driving the market growth. These are the key factors anticipated to drive the gastric cancer market in the region during the forecast period.

Competitive Scenario in the Global Gastric Cancer Market

Investment and agreement are common strategies followed by major market players. For instance, in April 2020, in the U.S., Samsung Bioepis launched ONTRUZANT, a biosimilar version of the reference biologic drug HERCEPTIN, for the treatment of HER2-overexpressing breast cancer, metastatic breast cancer, and metastatic gastric cancer or gastroesophageal junction adenocarcinoma.

Source: Research Dive Analysis

Some of the leading gastric cancer market players are Novartis AG, Pfizer, Inc., Mylan N.V., F. Hoffmann La Roche Ltd., Eli Lilly and Company, Merck & Co., Inc., Teva Pharmaceutical Industries Ltd., Celltrion Healthcare Co., Ltd., Samsung Bioepis, and Bristol Myers Squibb Company.

| Aspect | Particulars |

| Historical Market Estimations | 2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Disease Type |

|

| Segmentation by Treatment Type |

|

| Segmentation by Drug Class Outlook |

|

| Segmentation by Route of Administration |

|

| Segmentation by Distribution Channel |

|

| Key Companies Profiled |

|

Q1. What is the size of the global gastric cancer market?

A. The size of the global gastric cancer market was over $2,100.00 million in 2021 and is projected to reach $10,737.00 million by 2031.

Q2. Which are the major companies in the gastric cancer market?

A. Novartis AG, Pfizer, Inc., and Mylan N.V. are some of the key players in the global gastric cancer market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. Europe possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the Asia-Pacific gastric cancer market?

A. Asia-pacific gastric cancer market is anticipated to grow at 17.9% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. F. Hoffmann La Roche Ltd., Eli Lilly and Company, and Merck & Co., Inc. are the companies investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global Gastric Cancer market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on Gastric Cancer market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Gastric Cancer Market Analysis, by Disease Type

5.1.Overview

5.2.Adenocarcinoma

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region,2021-2031

5.2.3.Market share analysis, by country,2021-2031

5.3.Lymphoma

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region,2021-2031

5.3.3.Market share analysis, by country,2021-2031

5.4.Gastrointestinal Stromal Tumor

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region,2021-2031

5.4.3.Market share analysis, by country,2021-2031

5.5.Carcinoid Tumor

5.5.1.Definition, key trends, growth factors, and opportunities

5.5.2.Market size analysis, by region,2021-2031

5.5.3.Market share analysis, by country,2021-2031

5.6.Others

5.6.1.Definition, key trends, growth factors, and opportunities

5.6.2.Market size analysis, by region

5.6.3.Market share analysis, by country

5.7.Research Dive Exclusive Insights

5.7.1.Market attractiveness

5.7.2.Competition heatmap

6.Gastric Cancer Market Analysis, by Treatment Type

6.1.Immunotherapy

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region,2021-2031

6.1.3.Market share analysis, by country,2021-2031

6.2.Targeted Therapy

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region,2021-2031

6.2.3.Market share analysis, by country,2021-2031

6.3.Chemotherapy

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.2.Market size analysis, by region,2021-2031

6.3.3.Market share analysis, by country,2021-2031

6.4.Radiation Therapy and Surgery

6.4.1.Definition, key trends, growth factors, and opportunities

6.4.2.Market size analysis, by region,2021-2031

6.4.3.Market share analysis, by country,2021-2031

6.5.Research Dive Exclusive Insights

6.5.1.Market attractiveness

6.5.2.Competition heatmap

7.Gastric Cancer Market Analysis, by Drug Class Outlook

7.1.PD-1/PD-L1 Inhibitors

7.1.1.Definition, key trends, growth factors, and opportunities

7.1.2.Market size analysis, by region,2021-2031

7.1.3.Market share analysis, by country,2021-2031

7.2.HER2 Antagonists

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region,2021-2031

7.2.3.Market share analysis, by country,2021-2031

7.3.VEGFR2 Antagonists

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region,2021-2031

7.3.3.Market share analysis, by country,2021-2031

7.4.Others

7.4.1.Definition, key trends, growth factors, and opportunities

7.4.2.Market size analysis, by region,2021-2031

7.4.3.Market share analysis, by country,2021-2031

7.5.Research Dive Exclusive Insights

7.5.1.Market attractiveness

7.5.2.Competition heatmap

8.Gastric Cancer Market Analysis, by Route of Administration

8.1.Oral

8.1.1.Definition, key trends, growth factors, and opportunities

8.1.2.Market size analysis, by region,2021-2031

8.1.3.Market share analysis, by country,2021-2031

8.2.Injectable

8.2.1.Definition, key trends, growth factors, and opportunities

8.2.2.Market size analysis, by region,2021-2031

8.2.3.Market share analysis, by country,2021-2031

8.3.Research Dive Exclusive Insights

8.3.1.Market attractiveness

8.3.2.Competition heatmap

9.Gastric Cancer Market Analysis, by Distribution Channel

9.1.Hospital Pharmacies

9.1.1.Definition, key trends, growth factors, and opportunities

9.1.2.Market size analysis, by region,2021-2031

9.1.3.Market share analysis, by country,2021-2031

9.2.Specialty & Retail Pharmacies

9.2.1.Definition, key trends, growth factors, and opportunities

9.2.2.Market size analysis, by region,2021-2031

9.2.3.Market share analysis, by country,2021-2031

9.3.Others

9.3.1.Definition, key trends, growth factors, and opportunities

9.3.2.Market size analysis, by region,2021-2031

9.3.3.Market share analysis, by country,2021-2031

9.4.Research Dive Exclusive Insights

9.4.1.Market attractiveness

9.4.2.Competition heatmap

10.Gastric Cancer Market, by Region

10.1.North America

10.1.1.U.S.

10.1.1.1.Market size analysis, by Disease Type

10.1.1.2.Market size analysis, by Treatment Type

10.1.1.3.Market size analysis, by Drug Class Outlook

10.1.1.4.Market size analysis, by Route of Administration

10.1.1.5.Market size analysis, by Distribution Channel

10.1.2.Canada

10.1.2.1.Market size analysis, by Disease Type

10.1.2.2.Market size analysis, by Treatment Type

10.1.2.3.Market size analysis, by Drug Class Outlook

10.1.2.4.Market size analysis, by Route of Administration

10.1.2.5.Market size analysis, by Distribution Channel

10.1.3.Mexico

10.1.3.1.Market size analysis, by Disease Type

10.1.3.2.Market size analysis, by Treatment Type

10.1.3.3.Market size analysis, by Drug Class Outlook

10.1.3.4.Market size analysis, by Route of Administration

10.1.3.5.Market size analysis, by Distribution Channel

10.1.4.Research Dive Exclusive Insights

10.1.4.1.Market attractiveness

10.1.4.2.Competition heatmap

10.2.Europe

10.2.1.Germany

10.2.1.1.Market size analysis, by Disease Type

10.2.1.2.Market size analysis, by Treatment Type

10.2.1.3.Market size analysis, by Drug Class Outlook

10.2.1.4.Market size analysis, by Route of Administration

10.2.1.5.Market size analysis, by Distribution Channel

10.2.2.UK

10.2.2.1.Market size analysis, by Disease Type

10.2.2.2.Market size analysis, by Treatment Type

10.2.2.3.Market size analysis, by Drug Class Outlook

10.2.2.4.Market size analysis, by Route of Administration

10.2.2.5.Market size analysis, by Distribution Channel

10.2.3.France

10.2.3.1.Market size analysis, by Disease Type

10.2.3.2.Market size analysis, by Treatment Type

10.2.3.3.Market size analysis, by Drug Class Outlook

10.2.3.4.Market size analysis, by Route of Administration

10.2.3.5.Market size analysis, by Distribution Channel

10.2.4.Spain

10.2.4.1.Market size analysis, by Disease Type

10.2.4.2.Market size analysis, by Treatment Type

10.2.4.3.Market size analysis, by Drug Class Outlook

10.2.4.4.Market size analysis, by Route of Administration

10.2.4.5.Market size analysis, by Distribution Channel

10.2.5.Italy

10.2.5.1.Market size analysis, by Disease Type

10.2.5.2.Market size analysis, by Treatment Type

10.2.5.3.Market size analysis, by Drug Class Outlook

10.2.5.4.Market size analysis, by Route of Administration

10.2.5.5.Market size analysis, by Distribution Channel

10.2.6.Rest of Europe

10.2.6.1.Market size analysis, by Disease Type

10.2.6.2.Market size analysis, by Treatment Type

10.2.6.3.Market size analysis, by Drug Class Outlook

10.2.6.4.Market size analysis, by Route of Administration

10.2.6.5.Market size analysis, by Distribution Channel

10.2.7.Research Dive Exclusive Insights

10.2.7.1.Market attractiveness

10.2.7.2.Competition heatmap

10.3.Asia-Pacific

10.3.1.China

10.3.1.1.Market size analysis, by Disease Type

10.3.1.2.Market size analysis, by Treatment Type

10.3.1.3.Market size analysis, by Drug Class Outlook

10.3.1.4.Market size analysis, by Route of Administration

10.3.1.5.Market size analysis, by Distribution Channel

10.3.2.Japan

10.3.2.1.Market size analysis, by Disease Type

10.3.2.2.Market size analysis, by Treatment Type

10.3.2.3.Market size analysis, by Drug Class Outlook

10.3.2.4.Market size analysis, by Route of Administration

10.3.2.5.Market size analysis, by Distribution Channel

10.3.3.India

10.3.3.1.Market size analysis, by Disease Type

10.3.3.2.Market size analysis, by Treatment Type

10.3.3.3.Market size analysis, by Drug Class Outlook

10.3.3.4.Market size analysis, by Route of Administration

10.3.3.5.Market size analysis, by Distribution Channel

10.3.4.Australia

10.3.4.1.Market size analysis, by Disease Type

10.3.4.2.Market size analysis, by Treatment Type

10.3.4.3.Market size analysis, by Drug Class Outlook

10.3.4.4.Market size analysis, by Route of Administration

10.3.4.5.Market size analysis, by Distribution Channel

10.3.5.South Korea

10.3.5.1.Market size analysis, by Disease Type

10.3.5.2.Market size analysis, by Treatment Type

10.3.5.3.Market size analysis, by Drug Class Outlook

10.3.5.4.Market size analysis, by Route of Administration

10.3.5.5.Market size analysis, by Distribution Channel

10.3.6.Rest of Asia-Pacific

10.3.6.1.Market size analysis, by Disease Type

10.3.6.2.Market size analysis, by Treatment Type

10.3.6.3.Market size analysis, by Drug Class Outlook

10.3.6.4.Market size analysis, by Route of Administration

10.3.6.5.Market size analysis, by Distribution Channel

10.3.7.Research Dive Exclusive Insights

10.3.7.1.Market attractiveness

10.3.7.2.Competition heatmap

10.4.LAMEA

10.4.1.Brazil

10.4.1.1.Market size analysis, by Disease Type

10.4.1.2.Market size analysis, by Treatment Type

10.4.1.3.Market size analysis, by Drug Class Outlook

10.4.1.4.Market size analysis, by Route of Administration

10.4.1.5.Market size analysis, by Distribution Channel

10.4.2.Saudi Arabia

10.4.2.1.Market size analysis, by Disease Type

10.4.2.2.Market size analysis, by Treatment Type

10.4.2.3.Market size analysis, by Drug Class Outlook

10.4.2.4.Market size analysis, by Route of Administration

10.4.2.5.Market size analysis, by Distribution Channel

10.4.3.UAE

10.4.3.1.Market size analysis, by Disease Type

10.4.3.2.Market size analysis, by Treatment Type

10.4.3.3.Market size analysis, by Drug Class Outlook

10.4.3.4.Market size analysis, by Route of Administration

10.4.3.5.Market size analysis, by Distribution Channel

10.4.4.South Africa

10.4.4.1.Market size analysis, by Disease Type

10.4.4.2.Market size analysis, by Treatment Type

10.4.4.3.Market size analysis, by Drug Class Outlook

10.4.4.4.Market size analysis, by Route of Administration

10.4.4.5.Market size analysis, by Distribution Channel

10.4.5.Rest of LAMEA

10.4.5.1.Market size analysis, by Disease Type

10.4.5.2.Market size analysis, by Treatment Type

10.4.5.3.Market size analysis, by Drug Class Outlook

10.4.5.4.Market size analysis, by Route of Administration

10.4.5.5.Market size analysis, by Distribution Channel

10.4.6.Research Dive Exclusive Insights

10.4.6.1.Market attractiveness

10.4.6.2.Competition heatmap

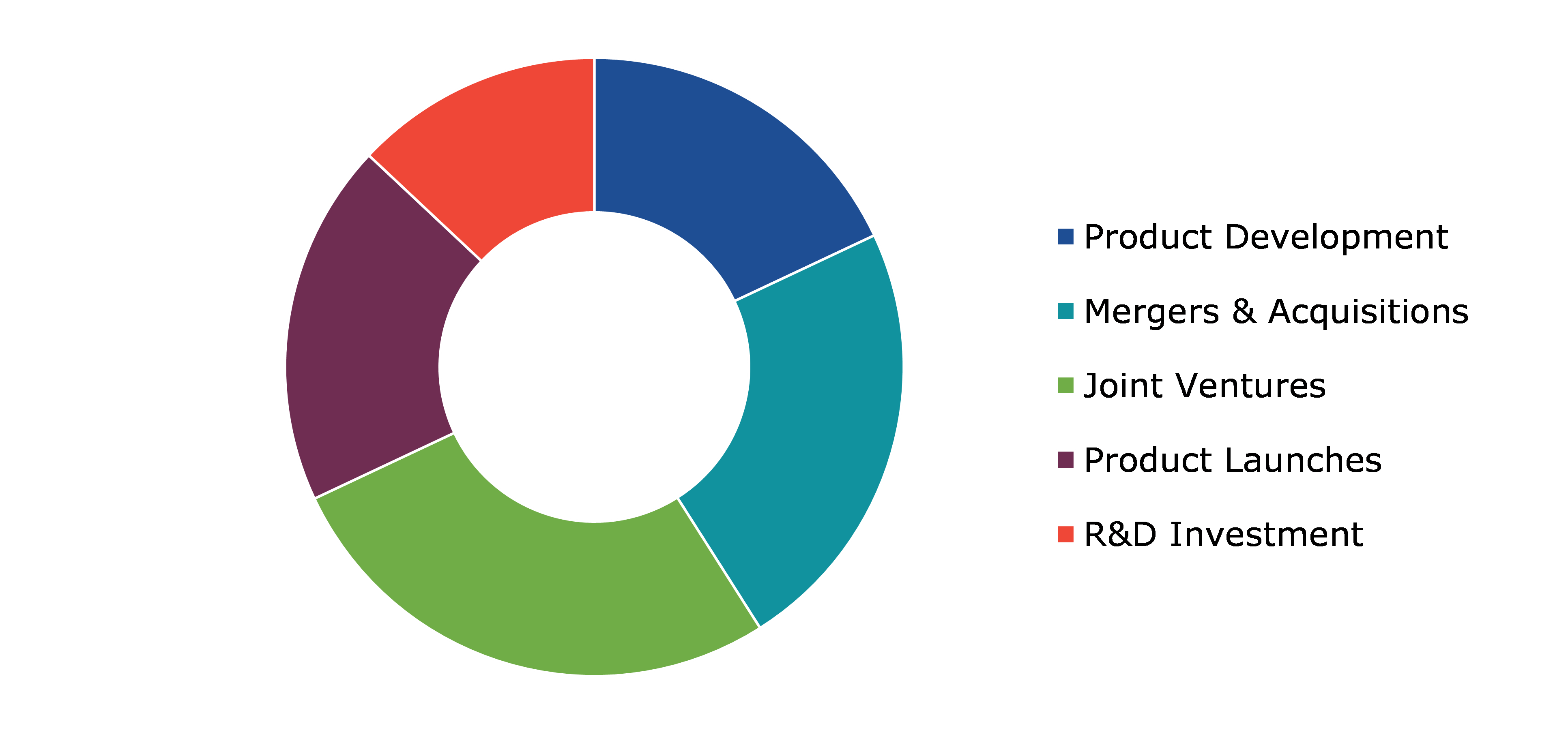

11.Competitive Landscape

11.1.Top winning strategies, 2021

11.1.1.By strategy

11.1.2.By year

11.2.Strategic overview

11.3.Market share analysis, 2021

12.Company Profiles

12.1.Novartis AG

12.1.1.Overview

12.1.2.Business segments

12.1.3.Product portfolio

12.1.4.Financial performance

12.1.5.Recent developments

12.1.6.SWOT analysis

12.2.Pfizer, Inc.

12.2.1.Overview

12.2.2.Business segments

12.2.3.Product portfolio

12.2.4.Financial performance

12.2.5.Recent developments

12.2.6.SWOT analysis

12.3.Mylan N.V.

12.3.1.Overview

12.3.2.Business segments

12.3.3.Product portfolio

12.3.4.Financial performance

12.3.5.Recent developments

12.3.6.SWOT analysis

12.4.F. Hoffmann La Roche Ltd.

12.4.1.Overview

12.4.2.Business segments

12.4.3.Product portfolio

12.4.4.Financial performance

12.4.5.Recent developments

12.4.6.SWOT analysis

12.5.Eli Lilly And Company

12.5.1.Overview

12.5.2.Business segments

12.5.3.Product portfolio

12.5.4.Financial performance

12.5.5.Recent developments

12.5.6.SWOT analysis

12.6.Merck & Co., Inc.

12.6.1.Overview

12.6.2.Business segments

12.6.3.Product portfolio

12.6.4.Financial performance

12.6.5.Recent developments

12.6.6.SWOT analysis

12.7.Teva Pharmaceutical Industries Ltd.

12.7.1.Overview

12.7.2.Business segments

12.7.3.Product portfolio

12.7.4.Financial performance

12.7.5.Recent developments

12.7.6.SWOT analysis

12.8.Celltrion Healthcare Co., Ltd.

12.8.1.Overview

12.8.2.Business segments

12.8.3.Product portfolio

12.8.4.Financial performance

12.8.5.Recent developments

12.8.6.SWOT analysis

12.9.Samsung Bioepis

12.9.1.Overview

12.9.2.Business segments

12.9.3.Product portfolio

12.9.4.Financial performance

12.9.5.Recent developments

12.9.6.SWOT analysis

12.10.Bristol Myers Squibb Company

12.10.1.Overview

12.10.2.Business segments

12.10.3.Product portfolio

12.10.4.Financial performance

12.10.5.Recent developments

12.10.6.SWOT analysis

Gastric cancer is a formidable health challenge affecting individuals worldwide. The exact cause of gastric cancer is still unknown. However, several risk factors have been identified including helicobacter pylori infection, use of tobacco and alcohol use, unhealthy diet, and genetic predisposition. Helicobacter pylori is a spiral bacterium that is a major risk factor for developing gastric cancer. It can cause chronic inflammation of the stomach lining, leading to the formation of cancerous cells. In addition, a diet rich in smoked, salted, or pickled foods, as well as a low intake of fruits and vegetables, has been associated with an increased risk of gastric cancer. Moreover, heavy tobacco and alcohol consumption has been linked to an elevated risk of developing gastric cancer. Furthermore, certain inherited genetic mutations, such as mutations in the CDH1 gene, can increase the likelihood of developing gastric cancer. The treatment of gastric cancer depends on several factors, including the stage of the cancer, the patient’s overall health, and individual preferences. Surgery, chemotherapy, radiation therapy, and targeted therapy are some of the common treatment options for gastric cancer.

Forecast Analysis of the Global Gastric Cancer Market

According to the report published by Research Dive, the global gastric cancer market is anticipated to garner a revenue of $10,737.00 million and rise at a striking CAGR of 17.9% over the analysis timeframe from 2022 to 2031.

The increasing prevalence of gastric cancer among individuals across the globe owing to the growing aged population, infections with Helicobacter pylori, and unhealthy lifestyle habits is predicted to fortify the growth of the gastric cancer market over the analysis timeframe. Besides, the increasing demand for effective treatments such as targeted therapies and immunotherapies is predicted to augment the growth of the market during the forecast period. Moreover, the increasing investment in R&D activities for gastric cancer treatments and the growing healthcare expenditure for the development of advanced diagnostic tools and screening techniques are expected to create huge growth opportunities for the gastric cancer market over the estimated period. However, the high cost of treating gastric cancer may hinder the growth of the market throughout the analysis period.

The major players of the gastric cancer market include Merck & Co., Inc., Eli Lilly and Company, Teva Pharmaceutical Industries Ltd., F. Hoffmann La Roche Ltd., Celltrion Healthcare Co., Ltd., Mylan N.V., Samsung Bioepis, Pfizer, Inc., Bristol Myers Squibb Company, Novartis AG, and many more.

Key Developments of the Gastric Cancer Market

The key companies operating in the industry are adopting various growth strategies & business tactics such as partnerships, collaborations, mergers & acquisitions, and launches to maintain a robust position in the overall market, which is subsequently helping the global gastric cancer market to grow exponentially. For instance:

- In September 2022, Pfizer Inc., a leading American multinational pharmaceutical and biotechnology corporation announced its partnership with Strata, a global leader in geotechnical engineering solutions. With this partnership, the enterprises aimed to promote several pan-tumor therapeutic trials to access the safety and efficacy of various cancer therapies.

- In March 2023, Pfizer Inc., a renowned American multinational pharmaceutical and biotechnology company announced its acquisition of Seagen Inc., an American biotechnology company. With this acquisition, the companies together aimed to bring new solutions to patients suffering from various types of cancers by combining the power of Seagen’s antibody-drug conjugate (ADC) technology.

- In April 2023, BeiGene Ltd., a global biotechnology company, developed a new drug with Novartis AG, a global healthcare company based in Switzerland. This drug is expected to become the first line of therapy for patients recognized with advanced forms of gastric cancer or for a unique type of cancer that begins in the food pipe or stomach join.

Most Profitable Region

The Asia-Pacific region of the gastric cancer market held the highest market share in 2021. This is mainly due to the increasing prevalence of gastric cancer among people and the growing awareness and diagnosis of this disease in the region. Moreover, the increasing healthcare expenditure across the region, especially in developing countries, is expected to drive the regional growth of the market throughout the estimated period.

Covid-19 Impact on the Gastric Cancer Market

The rise of the Covid-19 pandemic has badly affected the growth of the gastric cancer market, likewise, various other industries. This is mainly due to the delay in the delivery of finished products during the pandemic owing to the shortage of raw materials owing to disruption in the supply chains. Moreover, the reduced healthcare spending in many countries as most resources had been redirected to pandemic-related measures, has declined the growth of the market throughout the crisis. However, the increasing incidences of gastric cancer and the development of new therapies and treatments are expected to bring wide growth opportunities for the gastric cancer market post-pandemic period.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com