Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

CM23028641 |

Pages: 237 |

Feb 2023 |

In quarries and mines where continuous heavy-duty operations and all-weather usage are critical, operators seek high pulling power, improved grade ability, higher performance, better manoeuvrability, and robustness. These applications are well managed by dump trucks and mining trucks which are supported by a variety of service arrangements, depending on the site location and the number of vehicles and equipment deployed. Dump trucks and mining trucks family is popular for mining, quarries, road building projects, infrastructure, earthwork, tunnelling, and material movement applications. These factors are anticipated to boost the dump trucks and mining trucks industry growth in the upcoming years.

High maintenance costs and rigorous rules on big vehicles are projected to hinder market expansion. Also, safety issues related to mining and construction operations are expected to pose a barrier to the dump trucks and mining trucks market during the forecast period.

Trucks are necessary for mining, construction, infrastructure development, and energy plants, resulting in a favourable market climate. Several countries, including China, India, the United Kingdom, and the United States, are passing regulations to cut emissions and increase truck productivity, thus expanding the market. The criteria are in place to minimize carbon emissions and incorporate complex technology such as electric-operated mining trucks, resulting in huge dump trucks and mining trucks market opportunities.

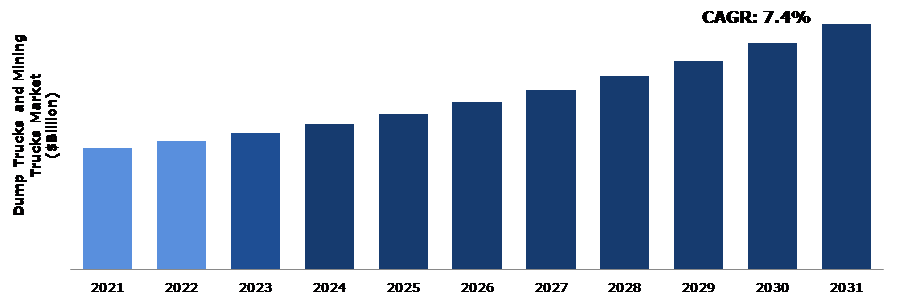

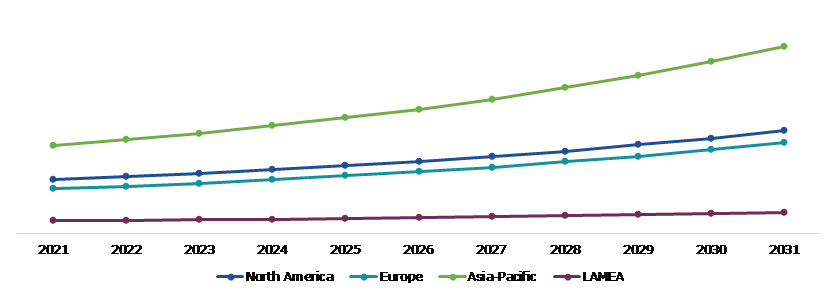

According to regional analysis, the Asia-Pacific dump trucks and mining trucks market accounted for $20.2 billion in 2021 and is predicted to grow with a CAGR of 7.5% in the projected timeframe.

Dump trucks and mining trucks are used to move materials for construction, such as sand, gravel, or dirt. The open-box bed of a conventional dump truck is hydraulically controlled and hinged at the back. The front of the bed can be raised to allow the contents to be dropped on the ground behind the truck at the delivery site.

The COVID-19 pandemic created multiple uncertainties, resulting in significant economic losses as various enterprises around the world came to a halt. This has ultimately reduced demand for the dump and mining trucks due to interruptions in the supply chain, the closure of manufacturing units, and an economic slump in various nations. Also, import-export restrictions were imposed on the key dump and mining trucks-producing countries such as the United States and China. The global COVID-19 epidemic has had an influence on heavy truck manufacture and demand, and this is expected to restrain the dump trucks and mining trucks market over the forecast period. The pandemic has resulted in stringent containment measures such as social separation, remote working, and the shutdown of some manufacturing units to handle the disease. These initiatives are predicted to drive the dump trucks and mining trucks market size during the analysis timeframe.

Globally, increased industrialization and urbanization are increasing the demand for natural resources such as oil and minerals. As a result, the worldwide mining sector is expanding, which is driving demand possibilities in the dump trucks and mining trucks market. The growing number of infrastructure-related developments has a further impact on the market. Dump truck and mining trucks demand is increasing as a result of the expansion of infrastructure-related projects and increasing government investments in infrastructure development. The expansion of the market is aided by the increase in mining production activities brought on by the rising demand for minerals and natural resources. In addition, the market for dump trucks is positively impacted by rising urbanization, changing lifestyle, an increase in expenditures, and higher consumer spending.

To know more about global dump trucks and mining trucks market drivers, get in touch with our analysts here.

The dump truck and mining trucks are mostly utilized for agricultural and forestry tasks as well as mining and construction. The dump truck inspection and servicing are critical for preserving the vehicle's condition and smooth operation. Dump trucks have a high maintenance cost since they are checked on a regular basis, particularly the tire pressure and suspension system. These trucks are also not fuel-efficient. The high fuel consumption raises the maintenance costs for dump truck and mining trucks.

The adoption of robots and autonomous technology is creating opportunities for market participants. With rising complexities in mining operations, robotic technology is gaining traction in the industry. The demand for several resources, including iron, gold, silver, and aluminium, is rising, which is accelerating the extraction process. Robotics enable extraction processes to be completed in a fraction of the time and effort previously required. Mining businesses are using driverless trucks, which allow operators to control mining activities from afar. The increased emphasis of automobile manufacturers on vehicle electrification is driving up demand for dump trucks and mining trucks.

To know more about global dump trucks and mining trucks market opportunities, get in touch with our analysts here.

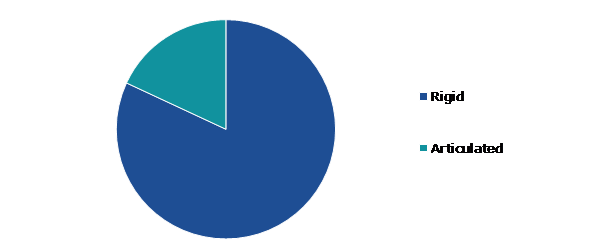

Based on type, the market has been divided into rigid and articulated. Among these, the rigid sub-segment accounted for the highest market share in 2021 whereas the articulated sub-segment is estimated to show the fastest growth during the forecast period.

Source: Research Dive Analysis

The rigid sub-type accounted a dominant market share in 2021. A rigid dump truck is a vehicle chassis with a dump body attached to the frame. The bed is elevated by a hydraulic ram positioned under the front of the dumper body between the frames, and the back of the bed is attached to the truck. The tailgate can be hinged or designed in the high raise tailgate type, in which pneumatic rams lift the gate open and up over the dump body. Because of their inexpensive price and appropriateness for a wide range of mining sites and building sites, these machines continue to be popular among some contractors.

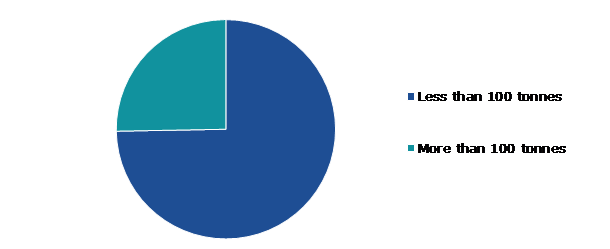

Based on payload class, the market has been divided into less than 100 tons and more than 100 tons. Among these, the less than 100 tons sub-segment accounted for highest revenue share in 2021.

Source: Research Dive Analysis

The less than 100 tonnes sub-segment accounted a dominant market share in 2021. The machine category for less than 100 tonnes is now the most active and expanding. The government's desire to push ultra-mega power projects near collieries is guaranteed to maintain demand for this equipment robustly. The anticipated privatization of coal mines where this kind of machine is wanted is another factor supporting this industry.

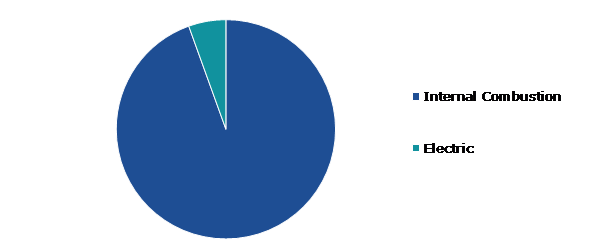

Based on engine type, the market has been divided into internal combustion and electric. Among these, the internal combustion sub-segment accounted for the highest revenue share in 2021.

Source: Research Dive Analysis

The internal combustion sub-segment accounted a dominant market share in 2021. Internal combustion engines are the most popular choice for dump trucks and mining truck applications, because it is a safer fuel choice for commercial vehicles with larger fuel tanks. Also, the internal combustion engine as a transportation fuel has a number of performance, efficiency, and safety advantages. Furthermore, due to its higher energy density, this engine provides more usable energy per unit of volume than others.

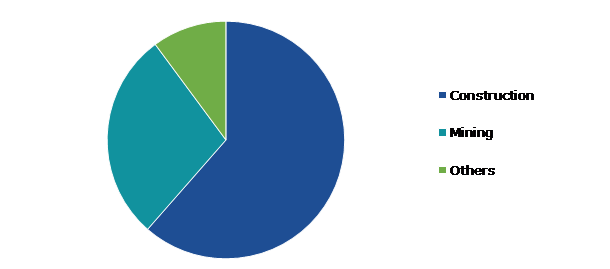

Based on end-use industry, the market has been divided into construction, mining, and others. Among these, the construction sub-segment accounted for the highest revenue share in 2021.

Source: Research Dive Analysis

The construction sub-segment accounted a dominant market share in 2021. Rising infrastructural projects that meet the growing demands of rural and urban people worldwide are also propelling the sector. The rising government investment in infrastructure and rising real estate spending and a focus on public infrastructure will drive product demand. Construction is significant in both emerging and developed economies. All these factors are anticipated to boost the dump trucks and mining trucks market share in the construction industry.

The dump trucks and mining trucks market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The Asia-Pacific dump trucks and mining trucks market accounted for the highest market share in 2021 and is anticipated to show the fastest growth during the forecast period. The Asia-Pacific region is predicted to have the biggest growth potential for mining equipment, including material handling equipment such as dump and mining trucks. The region has enormous potential in terms of mining production and mineral mines, which is increasing the demand for dump trucks and mining trucks. The region has seen a rise in mining equipment manufacture due to increased production in surface mining and the predictable nature of the equipment maintenance and replacement cycle in surface mining.

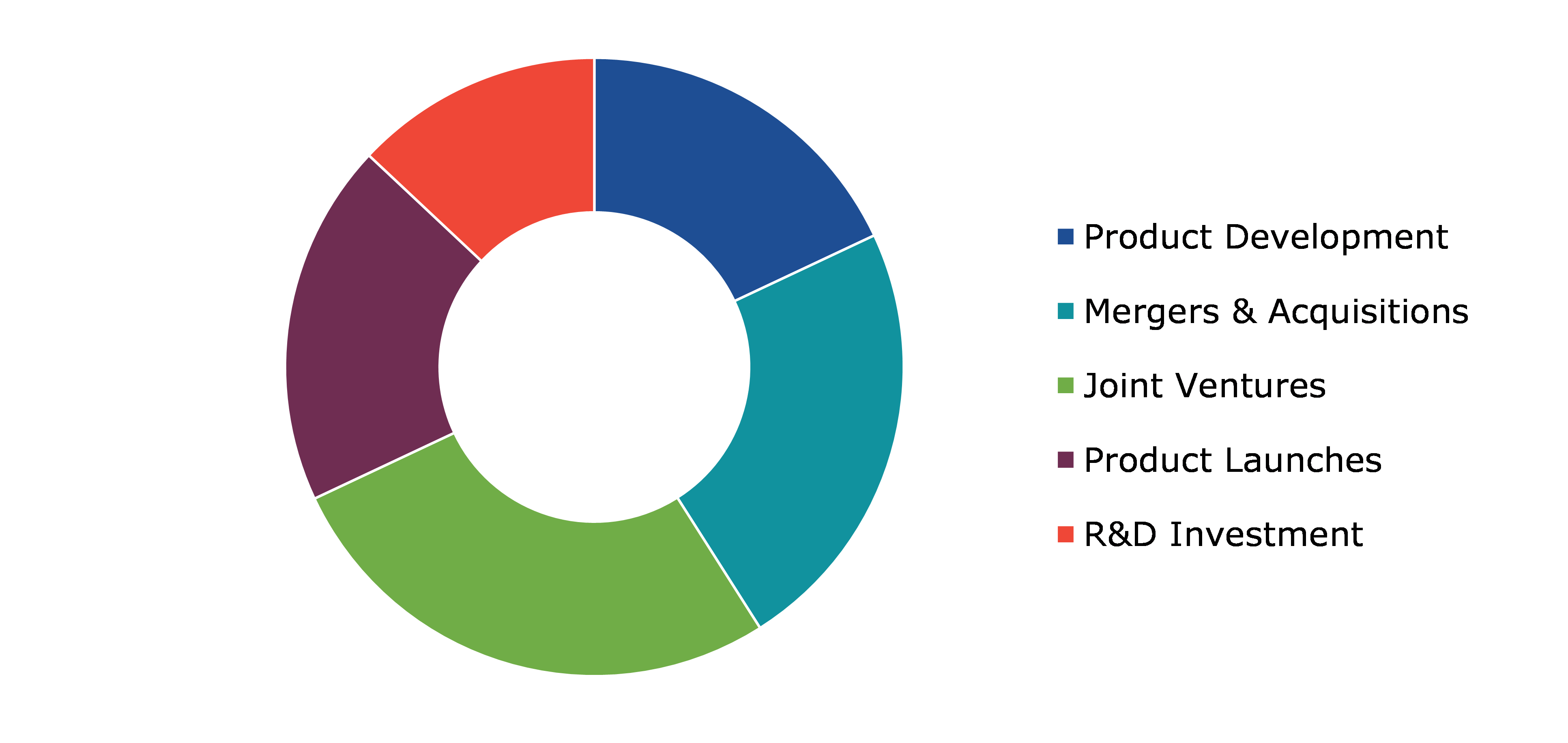

Investment and agreement are common strategies followed by major market players. For instance, in January 2021, Bell Trucks America collaborated with Bell Engineering and Pronto AI to launch North America’s first self-driving articulated dump truck. The Pronto system observes the road and job site environment using cameras mounted on the truck.

Source: Research Dive Analysis

Some of the leading dump trucks and mining trucks market players are SANY Group, Caterpillar, Hitachi Construction Machinery Co., Ltd., Liebherr, Volvo, Komatsu, Deere & Company, Zoomlion Heavy Industry Science and Technology Co., Ltd., XCMG Group, Scania.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Type |

|

| Segmentation by Payload Class |

|

| Segmentation by Engine Type |

|

| Segmentation by End-use Industry |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global dump trucks and mining market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on dump trucks and mining market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Dump Trucks and Mining Market Analysis, by Type

5.1.Overview

5.2.Rigid

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region, 2021-2031

5.2.3.Market share analysis, by country, 2021-2031

5.3.Articulated

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region, 2021-2031

5.3.3.Market share analysis, by country, 2021-2031

5.4.Research Dive Exclusive Insights

5.4.1.Market attractiveness

5.4.2.Competition heatmap

6.Dump Trucks and Mining Market Analysis, by Payload Class

6.1.Less than 100 tonnes

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region, 2021-2031

6.1.3.Market share analysis, by country, 2021-2031

6.2.More than 100 tonnes

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region, 2021-2031

6.2.3.Market share analysis, by country, 2021-2031

6.3.Research Dive Exclusive Insights

6.3.1.Market attractiveness

6.3.2.Competition heatmap

7.Dump Trucks and Mining Market Analysis, by Engine Type

7.1.Internal Combustion

7.1.1.Definition, key trends, growth factors, and opportunities

7.1.2.Market size analysis, by region, 2021-2031

7.1.3.Market share analysis, by country, 2021-2031

7.2.Electric

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region, 2021-2031

7.2.3.Market share analysis, by country, 2021-2031

7.3.Research Dive Exclusive Insights

7.3.1.Market attractiveness

7.3.2.Competition heatmap

8.Dump Trucks and Mining Market Analysis, by End-use Industry

8.1.Construction

8.1.1.Definition, key trends, growth factors, and opportunities

8.1.2.Market size analysis, by region, 2021-2031

8.1.3.Market share analysis, by country, 2021-2031

8.2.Mining

8.2.1.Definition, key trends, growth factors, and opportunities

8.2.2.Market size analysis, by region, 2021-2031

8.2.3.Market share analysis, by country, 2021-2031

8.3.Others

8.3.1.Definition, key trends, growth factors, and opportunities

8.3.2.Market size analysis, by region, 2021-2031

8.3.3.Market share analysis, by country, 2021-2031

8.4.Research Dive Exclusive Insights

8.4.1.Market attractiveness

8.4.2.Competition heatmap

9.Dump Trucks and Mining Market, by region

9.1.North America

9.1.1.U.S.

9.1.1.1.Market size analysis, by Type, 2021-2031

9.1.1.2.Market size analysis, by Payload Class, 2021-2031

9.1.1.3.Market size analysis, by Engine Type, 2021-2031

9.1.1.4.Market size analysis, by End-use Industry, 2021-2031

9.1.2.Canada

9.1.2.1.Market size analysis, by Type, 2021-2031

9.1.2.2.Market size analysis, by Payload Class, 2021-2031

9.1.2.3.Market size analysis, by Engine Type, 2021-2031

9.1.2.4.Market size analysis, by End-use Industry, 2021-2031

9.1.3.Mexico

9.1.3.1.Market size analysis, by Type, 2021-2031

9.1.3.2.Market size analysis, by Payload Class, 2021-2031

9.1.3.3.Market size analysis, by Engine Type, 2021-2031

9.1.3.4.Market size analysis, by End-use Industry, 2021-2031

9.1.4.Research Dive Exclusive Insights

9.1.4.1.Market attractiveness

9.1.4.2.Competition heatmap

9.2.Europe

9.2.1.Germany

9.2.1.1.Market size analysis, by Type, 2021-2031

9.2.1.2.Market size analysis, by Payload Class, 2021-2031

9.2.1.3.Market size analysis, by Engine Type, 2021-2031

9.2.1.4.Market size analysis, by End-use Industry, 2021-2031

9.2.2.UK

9.2.2.1.Market size analysis, by Type, 2021-2031

9.2.2.2.Market size analysis, by Payload Class, 2021-2031

9.2.2.3.Market size analysis, by Engine Type, 2021-2031

9.2.2.4.Market size analysis, by End-use Industry, 2021-2031

9.2.3.France

9.2.3.1.Market size analysis, by Type, 2021-2031

9.2.3.2.Market size analysis, by Payload Class, 2021-2031

9.2.3.3.Market size analysis, by Engine Type, 2021-2031

9.2.3.4.Market size analysis, by End-use Industry, 2021-2031

9.2.4.Spain

9.2.4.1.Market size analysis, by Type, 2021-2031

9.2.4.2.Market size analysis, by Payload Class, 2021-2031

9.2.4.3.Market size analysis, by Engine Type, 2021-2031

9.2.4.4.Market size analysis, by End-use Industry, 2021-2031

9.2.5.Italy

9.2.5.1.Market size analysis, by Type, 2021-2031

9.2.5.2.Market size analysis, by Payload Class, 2021-2031

9.2.5.3.Market size analysis, by Engine Type, 2021-2031

9.2.5.4.Market size analysis, by End-use Industry, 2021-2031

9.2.6.Rest of Europe

9.2.6.1.Market size analysis, by Type, 2021-2031

9.2.6.2.Market size analysis, by Payload Class, 2021-2031

9.2.6.3.Market size analysis, by Engine Type, 2021-2031

9.2.6.4.Market size analysis, by End-use Industry, 2021-2031

9.2.7.Research Dive Exclusive Insights

9.2.7.1.Market attractiveness

9.2.7.2.Competition heatmap

9.3.Asia Pacific

9.3.1.China

9.3.1.1.Market size analysis, by Type, 2021-2031

9.3.1.2.Market size analysis, by Payload Class, 2021-2031

9.3.1.3.Market size analysis, by Engine Type, 2021-2031

9.3.1.4.Market size analysis, by End-use Industry, 2021-2031

9.3.2.Japan

9.3.2.1.Market size analysis, by Type, 2021-2031

9.3.2.2.Market size analysis, by Payload Class, 2021-2031

9.3.2.3.Market size analysis, by Engine Type, 2021-2031

9.3.2.4.Market size analysis, by End-use Industry, 2021-2031

9.3.3.India

9.3.3.1.Market size analysis, by Type, 2021-2031

9.3.3.2.Market size analysis, by Payload Class, 2021-2031

9.3.3.3.Market size analysis, by Engine Type, 2021-2031

9.3.3.4.Market size analysis, by End-use Industry, 2021-2031

9.3.4.Australia

9.3.4.1.Market size analysis, by Type, 2021-2031

9.3.4.2.Market size analysis, by Payload Class, 2021-2031

9.3.4.3.Market size analysis, by Engine Type, 2021-2031

9.3.4.4.Market size analysis, by End-use Industry, 2021-2031

9.3.5.South Korea

9.3.5.1.Market size analysis, by Type, 2021-2031

9.3.5.2.Market size analysis, by Payload Class, 2021-2031

9.3.5.3.Market size analysis, by Engine Type, 2021-2031

9.3.5.4.Market size analysis, by End-use Industry, 2021-2031

9.3.6.Rest of Asia Pacific

9.3.6.1.Market size analysis, by Type, 2021-2031

9.3.6.2.Market size analysis, by Payload Class, 2021-2031

9.3.6.3.Market size analysis, by Engine Type, 2021-2031

9.3.6.4.Market size analysis, by End-use Industry, 2021-2031

9.3.7.Research Dive Exclusive Insights

9.3.7.1.Market attractiveness

9.3.7.2.Competition heatmap

9.4.LAMEA

9.4.1.Brazil

9.4.1.1.Market size analysis, by Type, 2021-2031

9.4.1.2.Market size analysis, by Payload Class, 2021-2031

9.4.1.3.Market size analysis, by Engine Type, 2021-2031

9.4.1.4.Market size analysis, by End-use Industry, 2021-2031

9.4.2.Saudi Arabia

9.4.2.1.Market size analysis, by Type, 2021-2031

9.4.2.2.Market size analysis, by Payload Class, 2021-2031

9.4.2.3.Market size analysis, by Engine Type, 2021-2031

9.4.2.4.Market size analysis, by End-use Industry, 2021-2031

9.4.3.UAE

9.4.3.1.Market size analysis, by Type, 2021-2031

9.4.3.2.Market size analysis, by Payload Class, 2021-2031

9.4.3.3.Market size analysis, by Engine Type, 2021-2031

9.4.3.4.Market size analysis, by End-use Industry, 2021-2031

9.4.4.South Africa

9.4.4.1.Market size analysis, by Type

9.4.4.2.Market size analysis, by Payload Class

9.4.4.3.Market size analysis, by Engine Type

9.4.4.4.Market size analysis, by End-use Industry

9.4.5.Rest of LAMEA

9.4.5.1.Market size analysis, by Type, 2021-2031

9.4.5.2.Market size analysis, by Payload Class, 2021-2031

9.4.5.3.Market size analysis, by Engine Type, 2021-2031

9.4.5.4.Market size analysis, by End-use Industry, 2021-2031

9.4.6.Research Dive Exclusive Insights

9.4.6.1.Market attractiveness

9.4.6.2.Competition heatmap

10.Competitive Landscape

10.1.Top winning strategies, 2021

10.1.1.By strategy

10.1.2.By year

10.2.Strategic overview

10.3.Market share analysis, 2021

11.Company Profiles

11.1.SANY Group

11.1.1.Overview

11.1.2.Business segments

11.1.3.Product portfolio

11.1.4.Financial performance

11.1.5.Recent developments

11.1.6.SWOT analysis

11.2.Caterpillar

11.2.1.Overview

11.2.2.Business segments

11.2.3.Product portfolio

11.2.4.Financial performance

11.2.5.Recent developments

11.2.6.SWOT analysis

11.3.Hitachi Construction Machinery Co., Ltd.

11.3.1.Overview

11.3.2.Business segments

11.3.3.Product portfolio

11.3.4.Financial performance

11.3.5.Recent developments

11.3.6.SWOT analysis

11.4.Liebherr

11.4.1.Overview

11.4.2.Business segments

11.4.3.Product portfolio

11.4.4.Financial performance

11.4.5.Recent developments

11.4.6.SWOT analysis

11.5.AB Volvo

11.5.1.Overview

11.5.2.Business segments

11.5.3.Product portfolio

11.5.4.Financial performance

11.5.5.Recent developments

11.5.6.SWOT analysis

11.6.Komatsu

11.6.1.Overview

11.6.2.Business segments

11.6.3.Product portfolio

11.6.4.Financial performance

11.6.5.Recent developments

11.6.6.SWOT analysis

11.7.Deere & Company

11.7.1.Overview

11.7.2.Business segments

11.7.3.Product portfolio

11.7.4.Financial performance

11.7.5.Recent developments

11.7.6.SWOT analysis

11.8.Zoomlion Heavy Industry Science and Technology Co., Ltd.

11.8.1.Overview

11.8.2.Business segments

11.8.3.Product portfolio

11.8.4.Financial performance

11.8.5.Recent developments

11.8.6.SWOT analysis

11.9.XCMG Group

11.9.1.Overview

11.9.2.Business segments

11.9.3.Product portfolio

11.9.4.Financial performance

11.9.5.Recent developments

11.9.6.SWOT analysis

11.10.Scania

11.10.1.Overview

11.10.2.Business segments

11.10.3.Product portfolio

11.10.4.Financial performance

11.10.5.Recent developments

11.10.6.SWOT analysis

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}