Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

EN23028627 |

Pages: 240 |

Feb 2023 |

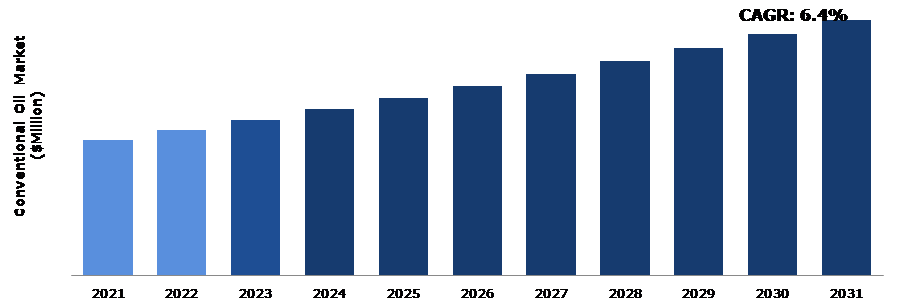

Conventional oil, often known as crude oil or petroleum, is an organic material that has originated naturally within the earth's crust. Conventional oil deposits are the most accessible and least technically difficult to develop. Increase in the need for improved equipment reliability and uptime in various industries is expected to impact industrial oil sales in the upcoming years. Increase in production and sales of light-duty cars are expected to have a direct impact on engine oil consumption, driving demand for engine oil during the forecast period. Fossil fuels have been at the center of growth and trade ever since industrialization reorganized economies in order to manufacture goods. Fuels made from energy-dense crude oil have long since replaced coal in many applications and have dominated the transportation fuel market. These factors are expected to drive conventional oil market share expansion during the forecast period.

The frequency and size of changes in the price of conventional oil on a global scale have increased. The uncertainty brought on by fluctuations in oil prices is expected to slow down economic growth by raising production costs or altering investment behavior. All of these reasons are expected to hamper the growth of the conventional oil market revenue.

The increase in the use of cutting-edge technologies in the global market has emerged in the creation of sophisticated conventional oil-based engine oil. The development of superior engine oil for automotive applications is being aided by the rise in the usage of cutting-edge fuel and lubricant technology. These continuing innovations are anticipated to fuel market expansion during the forecast period.

According to regional analysis, the LAMEA conventional oil market accounted for the dominating market share in 2021. LAMEA conventional oil market is expected to expand as a result of the rise in automobile sales in Brazil, South Africa, and Saudi Arabia and the increase in demand for lower-viscosity motor oil supplements.

Conventional oil petroleum reservoirs are often stratified, with numerous levels of varied reservoir quality. Conventional oil is an organic substance that formed naturally within the Earth's crust and is also referred to as crude oil or petroleum. It is a hydrocarbon, which means that its main ingredients are hydrogen and carbon with traces of other substances including nitrogen, sulfur, and different metals. Conventional oil is extracted from the earth through drilling and pumping.

The COVID-19 pandemic has brought several uncertainties leading to severe economic losses as various businesses across the world were standstill. In addition to posing a serious threat to human health, the global COVID-19 outbreak has also changed people's work and way of life. Countries implemented precautions like lockdowns to stop the disease from spreading as the number of confirmed cases increased. As a result of these measures, the world was subjected to an economic blockade, with global supply lines disrupted.

Conventional oils are frequently the most cost-effective alternative because they require far less refinement and re-engineering, which can be costly processes. Many automakers still request conventional engine oils as long as they meet the most recent industry specifications. Importantly, while conventional motor oils are closer to natural oil than synthetics or half synthetics, they still contain key additives to assist decrease engine wear and increasing performance. Advanced conventional oils contain additives that can clear away existing sludge in oilways and prevent new sludge from accumulating. All these factors are anticipated to boost the conventional oil market share.

To know more about global conventional oil market drivers, get in touch with our analysts here.

Conventional oil is effective at protecting the engine, but it does contain pollutants. Conventional oil is created by refining crude oil to give it the required characteristics for lubricating an engine. However, as it is derived from a natural process, conventional oil has some intrinsic irregularity in its structure at the molecular level. These contaminants may increase friction, hastening the oil's decomposition. Synthetic oil, on the other hand, is created from a wholly synthetic oil with a more regular molecular structure. Therefore, synthetic oil will last longer and perform better under harsh conditions. Due to all these factors, the market demand for conventional oil is expected to be hampered during the forecast years.

Technological advancements will be essential in addressing global energy demand because they enable the discovery of new resources, access to harsh or isolated regions, and the development of difficult reservoirs, Technological developments allow for more oil and natural gas to be extracted from the length of each well, enhancing production and lowering the environmental impact of energy production. For example, by combining extended-reach drilling capacity with modern stimulation technology, oil companies may optimize how and where stimulation fluid interacts with rock, allowing sustained production rates along the length of the wellbore. These factors are estimated to create several opportunities for the key players operating in the market during the forecast period.

To know more about global conventional oil market opportunities, get in touch with our analysts here.

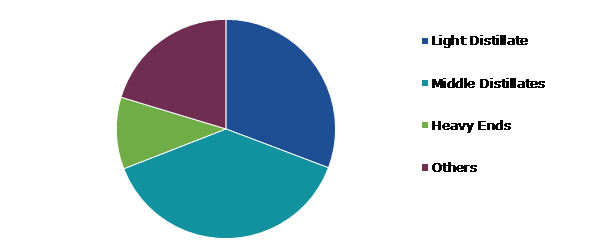

Based on type, the market has been divided into light distillate, middle distillates, heavy ends, and others. Among these, the middle distillates sub-segment accounted for the highest market share in 2021, whereas the light distillate sub-segment is estimated to show the fastest growth during the forecast period.

Source: Research Dive Analysis

The middle distillates sub-segment accounted for a dominant market share in 2021. Crude oil is one of the most precious commodities on the planet, but it is useless in its raw form. Middle distillates are largely utilized as fuel for heating, lighting, and transportation around the world. Middle distillates account for 25% to 40% of the oil product output during the refinement of crude oil. These are the major factors expected to drive the sub-segment growth during the forecast period.

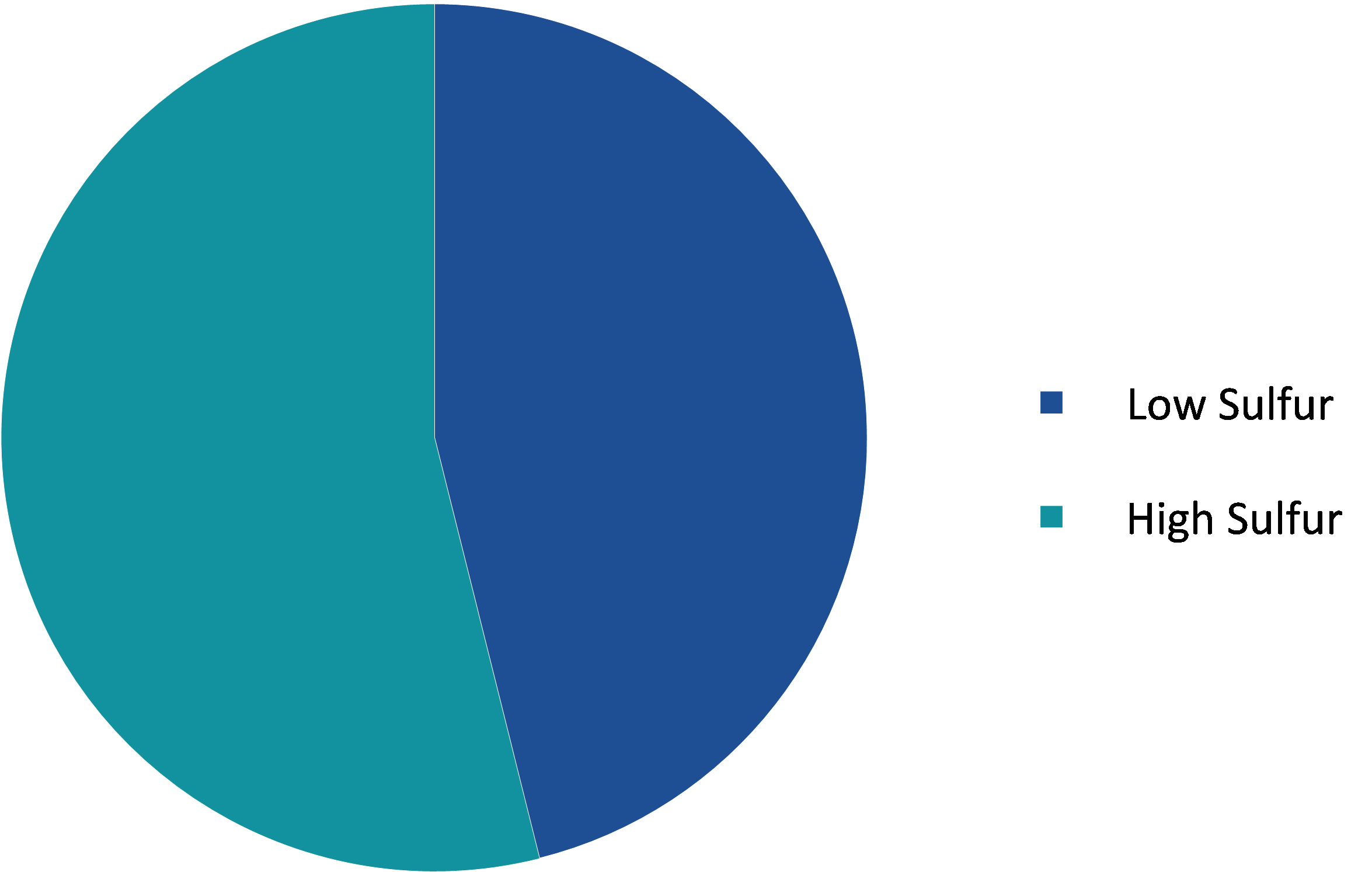

Based on sulfur content, the market has been divided into low sulfur and high sulfur. Among these, the high sulfur sub-segment accounted for the highest revenue share in 2021.

Source: Research Dive Analysis

The high sulfur sub-segment accounted for a dominant market share in 2021. A common ingredient found in crude oil and petroleum products is sulfur. A crude oil grade with a high sulfur percentage will have a lower value on average. The high sulfur content of conventional oil is sometimes referred to as sour crude. It is suitable for use in all types of power plants, industries, industrial buildings, constructions, and boilers.

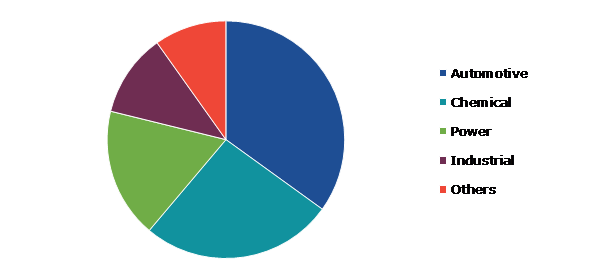

Based on end-user industry, the market has been divided into automotive, chemical, power, industrial, and others. Among these, the automotive sub-segment accounted for the highest revenue share in 2021.

Source: Research Dive Analysis

The automotive sub-segment accounted for a dominant market share in 2021. Increase in automotive manufacturing and demand for traditional and synthetic materials are expected to drive growth. Automobile sales in Asia-Pacific and North America have been gradually expanding in recent years, owing mostly to population growth and an increase in consumer buying capacity. The market is predicted to develop significantly during the forecast period due to the high level of technological advancement implemented in the entire automotive sector.

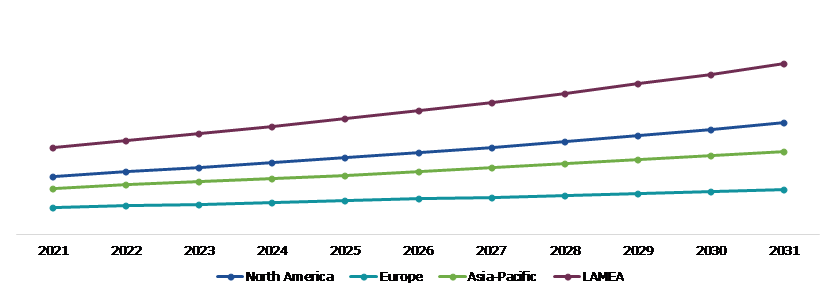

The conventional oil market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The LAMEA conventional oil market is anticipated to hold the highest market share in 2031. The LAMEA region, which includes five of the top ten oil-producing countries, accounts for around 27% of global oil output. The Middle East, the second most dynamic upstream market, has seen more than 30% expansion of refining capacity in recent years, and even more sizable global refining projects will be carried out there in the upcoming years. These investments are expected to have a beneficial influence on the market growth of the conventional oil market during the forecast period.

Investment and agreement are common strategies followed by major market players. For instance, in January 2023, UK-based oil giant BP intends to raise investments in its Texas and Gulf of Mexico oil and gas production assets. The decision comes in response to the U.S. government's plea to energy corporations to expand oil supplies in order to lower fuel prices as inflation expenses hit the industry.

Source: Research Dive Analysis

Some of the leading conventional oil market players are BP, Chevron, Eni, ExxonMobil, Shell, Total, CNPC, Equinor, Petrobras, and Repsol.

| Aspect | Particulars |

| Historical Market Estimations | 2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Type |

|

| Segmentation by Sulfur Content |

|

| Segmentation by End-user Industry |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global Conventional Oil market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on Conventional Oil market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Conventional Oil Market Analysis, by Type

5.1.Overview

5.2.Light Distillate

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region

5.2.3.Market share analysis, by country

5.3.Middle Distillates

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region

5.3.3.Market share analysis, by country

5.4.Heavy Ends

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region

5.4.3.Market share analysis, by country

5.5.Others

5.5.1.Definition, key trends, growth factors, and opportunities

5.5.2.Market size analysis, by region

5.5.3.Market share analysis, by country

5.6.Research Dive Exclusive Insights

5.6.1.Market attractiveness

5.6.2.Competition heatmap

6.Conventional Oil Market Analysis, by Sulfur Content

6.1.Low Sulfur

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region

6.1.3.Market share analysis, by country

6.2.High Sulfur

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region

6.2.3.Market share analysis, by country

6.3.Research Dive Exclusive Insights

6.3.1.Market attractiveness

6.3.2.Competition heatmap

7.Conventional Oil Market Analysis, by End-user Industry

7.1.Automotive

7.1.1.Definition, key trends, growth factors, and opportunities

7.1.2.Market size analysis, by region

7.1.3.Market share analysis, by country

7.2.Chemical

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region

7.2.3.Market share analysis, by country

7.3.Power

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region

7.3.3.Market share analysis, by country

7.4.Industrial

7.4.1.Definition, key trends, growth factors, and opportunities

7.4.2.Market size analysis, by region

7.4.3.Market share analysis, by country

7.5.Others

7.5.1.Definition, key trends, growth factors, and opportunities

7.5.2.Market size analysis, by region

7.5.3.Market share analysis, by country

7.6.Research Dive Exclusive Insights

7.6.1.Market attractiveness

7.6.2.Competition heatmap

8.Conventional Oil Market, by Region

8.1.North America

8.1.1.U.S.

8.1.1.1.Market size analysis, by Type

8.1.1.2.Market size analysis, by Sulfur Content

8.1.1.3.Market size analysis, by End-user Industry

8.1.2.Canada

8.1.2.1.Market size analysis, by Type

8.1.2.2.Market size analysis, by Sulfur Content

8.1.2.3.Market size analysis, by End-user Industry

8.1.3.Mexico

8.1.3.1.Market size analysis, by Type

8.1.3.2.Market size analysis, by Sulfur Content

8.1.3.3.Market size analysis, by End-user Industry

8.1.4.Research Dive Exclusive Insights

8.1.4.1.Market attractiveness

8.1.4.2.Competition heatmap

8.2.Europe

8.2.1.Germany

8.2.1.1.Market size analysis, by Type

8.2.1.2.Market size analysis, by Sulfur Content

8.2.1.3.Market size analysis, by End-user Industry

8.2.2.UK

8.2.2.1.Market size analysis, by Type

8.2.2.2.Market size analysis, by Sulfur Content

8.2.2.3.Market size analysis, by End-user Industry

8.2.3.France

8.2.3.1.Market size analysis, by Type

8.2.3.2.Market size analysis, by Sulfur Content

8.2.3.3.Market size analysis, by End-user Industry

8.2.4.Spain

8.2.4.1.Market size analysis, by Type

8.2.4.2.Market size analysis, by Sulfur Content

8.2.4.3.Market size analysis, by End-user Industry

8.2.5.Italy

8.2.5.1.Market size analysis, by Type

8.2.5.2.Market size analysis, by Sulfur Content

8.2.5.3.Market size analysis, by End-user Industry

8.2.6.Rest of Europe

8.2.6.1.Market size analysis, by Type

8.2.6.2.Market size analysis, by Sulfur Content

8.2.6.3.Market size analysis, by End-user Industry

8.2.7.Research Dive Exclusive Insights

8.2.7.1.Market attractiveness

8.2.7.2.Competition heatmap

8.3.Asia-Pacific

8.3.1.China

8.3.1.1.Market size analysis, by Type

8.3.1.2.Market size analysis, by Sulfur Content

8.3.1.3.Market size analysis, by End-user Industry

8.3.2.Japan

8.3.2.1.Market size analysis, by Type

8.3.2.2.Market size analysis, by Sulfur Content

8.3.2.3.Market size analysis, by End-user Industry

8.3.3.India

8.3.3.1.Market size analysis, by Type

8.3.3.2.Market size analysis, by Sulfur Content

8.3.3.3.Market size analysis, by End-user Industry

8.3.4.Australia

8.3.4.1.Market size analysis, by Type

8.3.4.2.Market size analysis, by Sulfur Content

8.3.4.3.Market size analysis, by End-user Industry

8.3.5.South Korea

8.3.5.1.Market size analysis, by Type

8.3.5.2.Market size analysis, by Sulfur Content

8.3.5.3.Market size analysis, by End-user Industry

8.3.6.Rest of Asia-Pacific

8.3.6.1.Market size analysis, by Type

8.3.6.2.Market size analysis, by Sulfur Content

8.3.6.3.Market size analysis, by End-user Industry

8.3.7.Research Dive Exclusive Insights

8.3.7.1.Market attractiveness

8.3.7.2.Competition heatmap

8.4.LAMEA

8.4.1.Brazil

8.4.1.1.Market size analysis, by Type

8.4.1.2.Market size analysis, by Sulfur Content

8.4.1.3.Market size analysis, by End-user Industry

8.4.2.Saudi Arabia

8.4.2.1.Market size analysis, by Type

8.4.2.2.Market size analysis, by Sulfur Content

8.4.2.3.Market size analysis, by End-user Industry

8.4.3.UAE

8.4.3.1.Market size analysis, by Type

8.4.3.2.Market size analysis, by Sulfur Content

8.4.3.3.Market size analysis, by End-user Industry

8.4.4.South Africa

8.4.4.1.Market size analysis, by Type

8.4.4.2.Market size analysis, by Sulfur Content

8.4.4.3.Market size analysis, by End-user Industry

8.4.5.Rest of LAMEA

8.4.5.1.Market size analysis, by Type

8.4.5.2.Market size analysis, by Sulfur Content

8.4.5.3.Market size analysis, by End-user Industry

8.4.6.Research Dive Exclusive Insights

8.4.6.1.Market attractiveness

8.4.6.2.Competition heatmap

9.Competitive Landscape

9.1.Top winning strategies, 2021

9.1.1.By strategy

9.1.2.By year

9.2.Strategic overview

9.3.Market share analysis, 2021

10.Company Profiles

10.1.BP

10.1.1.Overview

10.1.2.Business segments

10.1.3.Product portfolio

10.1.4.Financial performance

10.1.5.Recent developments

10.1.6.SWOT analysis

10.2.Chevron

10.2.1.Overview

10.2.2.Business segments

10.2.3.Product portfolio

10.2.4.Financial performance

10.2.5.Recent developments

10.2.6.SWOT analysis

10.3.Eni

10.3.1.Overview

10.3.2.Business segments

10.3.3.Product portfolio

10.3.4.Financial performance

10.3.5.Recent developments

10.3.6.SWOT analysis

10.4.ExxonMobil

10.4.1.Overview

10.4.2.Business segments

10.4.3.Product portfolio

10.4.4.Financial performance

10.4.5.Recent developments

10.4.6.SWOT analysis

10.5.Shell

10.5.1.Overview

10.5.2.Business segments

10.5.3.Product portfolio

10.5.4.Financial performance

10.5.5.Recent developments

10.5.6.SWOT analysis

10.6.Total

10.6.1.Overview

10.6.2.Business segments

10.6.3.Product portfolio

10.6.4.Financial performance

10.6.5.Recent developments

10.6.6.SWOT analysis

10.7.CNPC

10.7.1.Overview

10.7.2.Business segments

10.7.3.Product portfolio

10.7.4.Financial performance

10.7.5.Recent developments

10.7.6.SWOT analysis

10.8.Equinor

10.8.1.Overview

10.8.2.Business segments

10.8.3.Product portfolio

10.8.4.Financial performance

10.8.5.Recent developments

10.8.6.SWOT analysis

10.9.Petrobras

10.9.1.Overview

10.9.2.Business segments

10.9.3.Product portfolio

10.9.4.Financial performance

10.9.5.Recent developments

10.9.6.SWOT analysis

10.10.Repsol

10.10.1.Overview

10.10.2.Business segments

10.10.3.Product portfolio

10.10.4.Financial performance

10.10.5.Recent developments

10.10.6.SWOT analysis

11.Appendix

11.1.Parent & peer market analysis

11.2.Premium insights from industry experts

11.3.Related reports

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}