Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

LI20128330 |

Pages: 300 |

Sep 2022 |

The antinuclear antibody (ANA) test is a blood test done to determine whether there are any autoimmune diseases that affect the body's tissues and organs. These exams look for antinuclear antibodies in the blood. Antibodies are proteins that the human immune system normally makes to fight foreign bodies such as viruses and bacteria. However, these antibodies start attacking their own healthy cells instead. It is fine to have a few antinuclear antibodies in the blood. However, the presence of a large number of antinuclear antibodies is a sign of having an autoimmune disease.

Indirect immunofluorescence, ELISA, and other procedures are some of the methods used to assess antinuclear antibodies. The cases of autoimmune diseases are increasing across the globe. The increasing incidence rate of autoimmune diseases is a serious threat to society. For instance, according to the National Stem Cell Foundation (NSCF), a non-profit organization that funds regenerative medicine and adult stem cell research, around 4% of the world population is affected by one of more than eighty different autoimmune diseases. The most common autoimmune diseases include type 1 diabetes, rheumatoid arthritis, multiple sclerosis, Crohn’s disease, lupus, psoriasis, and scleroderma. Antinuclear antibody tests are becoming more and more popular as a way to diagnose autoimmune diseases such as rheumatoid arthritis, Systemic Lupus Erythematosus, Sjogren's syndrome, and many more. The growing prevalence of autoimmune diseases is the main factor driving the demand for the antinuclear antibody test market.

A shortage of skilled lab technicians and diagnostic mistakes are the main factors anticipated to impede the growth of the global anti-nuclear antibody testing market. For instance, according to the American College of Rheumatology, anti-nuclear antibody test may yield false positive results in healthy individuals, who are free of any medical illnesses or those who are taking drugs like isoniazid and procainamide. According to the Herald Scholarly Open Access, the antinuclear antibody test is very sensitive for the diagnosis of an autoimmune disorder and may provide false results. It has been observed that 15% of healthy individuals have a positive antinuclear antibody test without autoimmune disorders.

The growing awareness and improving healthcare infrastructure in developing countries are anticipated to provide growth opportunities for the global antinuclear antibody test market during the forecast period. Furthermore, the rising number of diagnostic laboratories along with the increasing investment in lab automation is projected to provide growth opportunities for the global market.

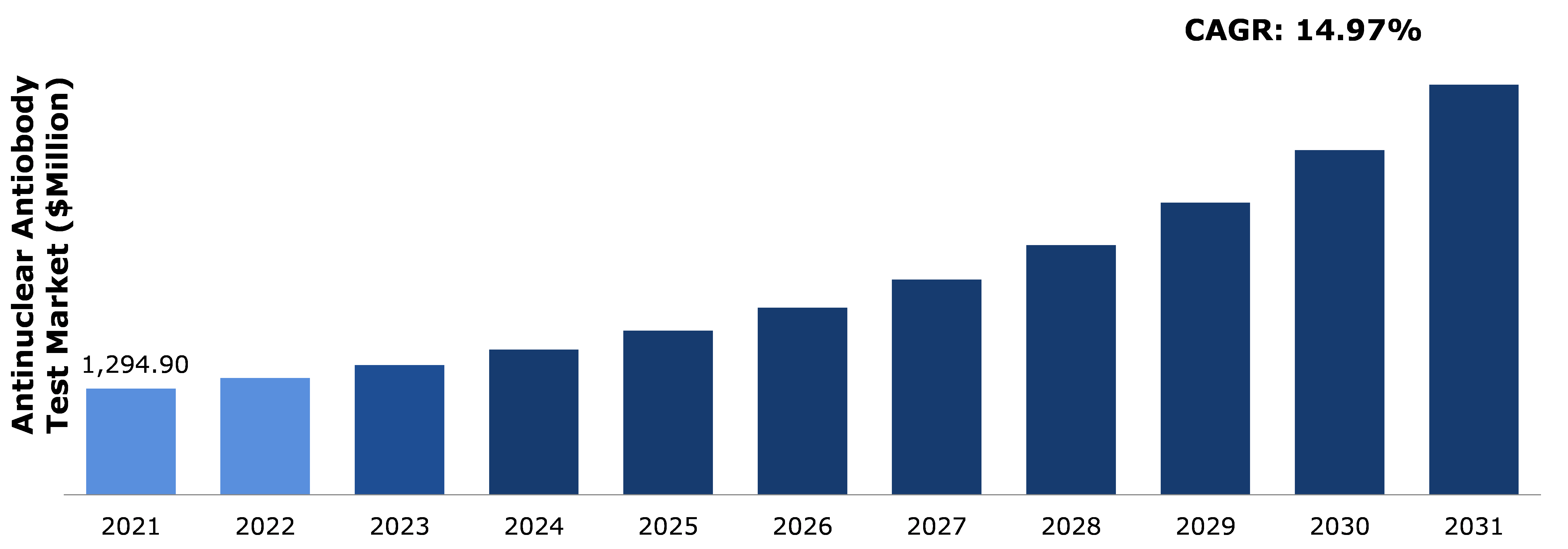

According to regional analysis, the North America antinuclear antibody test market accounted for $461.00 million in 2021 and is predicted to grow with a CAGR of 13.85% in the projected timeframe. The growing incidence of autoimmune diseases across the region is driving the growth of the anti-nuclear antibody test market.

The ANA test is performed to check for the presence of antinuclear antibodies in the blood. The presence of antinuclear antibodies in the blood may indicate an individual might have an autoimmune condition. The immune system mistakenly attacks one's cells, tissues, and/or organs as a result of an autoimmune illness. Serious health issues may result from these conditions. Additionally, the immune system produces antibodies, which are proteins, to combat external invaders like viruses and bacteria. An antinuclear antibody, however, targets one's healthy cells.

The COVID-19 pandemic is anticipated to have a positive effect on the market. Anti-nuclear antibody testing since COVID-19 patients have a high chance of developing autoimmune illnesses, which necessitates early diagnosis utilizing anti-nuclear antibody testing as a screening technique. For instance, according to a study conducted by the Department of Laboratory Medicine and Pathology at the University of Washington in the United States in 2020, 30% of COVID-19 patients had anti-nuclear antibodies that could be detected. Antinuclear antibody testing has also been the subject of wide research and clinical studies for the development of the COVID-19 vaccine and for the treatment of COVID-19, which will further fuel the market's expansion.

The incidence of autoimmune diseases is rising across the world. However, according to medical practitioners, the cause of the onset of autoimmune disease is unknown. Individual own genes combined with environmental or infection might be the reason for the cause of the autoimmune disorder. In an autoimmune disorder, the body's immune system attacks one's healthy cells. The conditions include rheumatoid arthritis, type 1 diabetes, multiple sclerosis, Crohn’s disease, lupus, psoriasis, and scleroderma. Changing lifestyles and eating are linked to increased incidences of autoimmune diseases across the globe. Western food items such as fried chicken, and pizza, burgers are becoming popular worldwide. However, regular consumption of these food products could be one of the factors for the spike in cases of autoimmune diseases worldwide. For instance, according to Johns Hopkins University, autoimmune disease affects 3% of the U.S. population. The increasing incidence of autoimmune disease is the main factor driving the demand for the antinuclear antibody test market.

To know more about global methanol market drivers, get in touch with our analysts here.

Antinuclear antibody testing is a sensitive process and sometimes yields false results, even in healthy individuals. As a result, testing antinuclear antibodies require trained and skilled technicians. Furthermore, detecting and accurately predicting the result of the ANA test requires advanced lad equipment. The high cost of this equipment may hinder the market growth during the forecast period. Therefore, the shortage of skilled lab technicians and the high cost of advanced lab equipment may hinder the market growth.

Improving healthcare infrastructure and rising spending on laboratory automation are expected to provide growth opportunities for the global antinuclear antibody market. Furthermore, government initiatives and rising awareness about the autoimmune disease among people will further propel the demand for ANA tests during the forecast period. In addition, companies like Johnson & Johnson are increasingly spending on increasing product portfolios for autoimmune diseases. For instance, Johnson & Johnson acquired Momenta in October 2020 to increase its focus on autoimmune diseases. Johnson & Johnson now has rights to nipocalimab (M281), a clinically validated antibody. Nipocalimab could be used to treat autoimmune diseases. Growing R&D investment to develop novel treatments will provide growth opportunities for the ANA test market in the coming years.

To know more about global antinuclear antibody test market opportunities, get in touch with our analysts here.

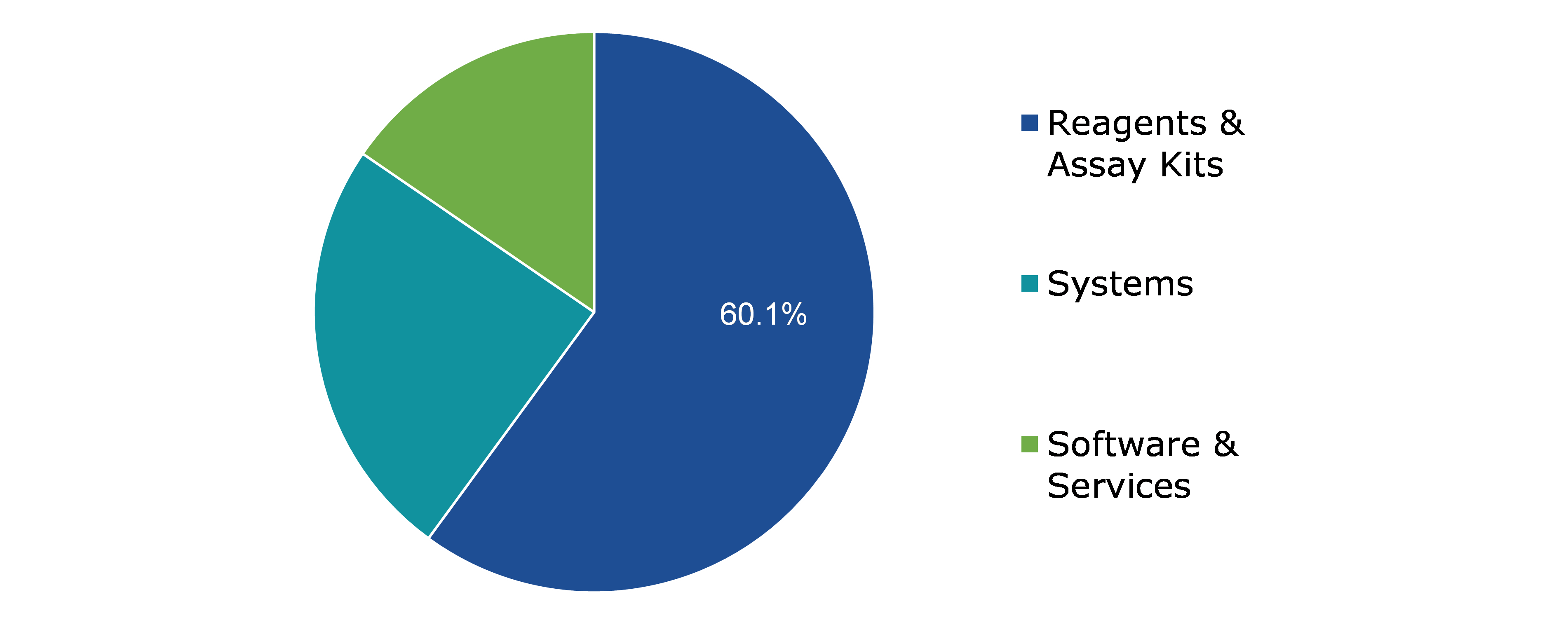

Based on product, the market has been divided into reagents & assay kits, systems, software & services. Among these, the reagents & assay kits sub-segment accounted for the highest market share in 2021 and estimated to show the fastest growth during the forecast period. System sub-segment is expected to significantly grow during the timeframe

Source: Research Dive Analysis

The reagents & assay kits sub-type is anticipated to have a dominant market share and fastest growth generating a revenue of $3,153.10 million by 2031, growing from $777.70 million in 2021. The test kits are primarily used in life science research, drug discovery and development, environmental monitoring, and the study of disease pathways, as well as for various research and development purposes such as screening for potential drug candidates and evaluating biopharmaceutical production processes.

The ANA test detects the presence of antinuclear antibodies in the blood of an individual which adheres to reagent test cells, generating distinctive fluorescence patterns linked to specific autoimmune disorders The growing number of ANA tests owing to increasing awareness among people, improving healthcare infrastructure, and a broad array of applications is anticipated to enhance the market throughout the projected timeframe..

The systems sub-type is anticipated to show the second dominate market share and shall generate a revenue of $ 1,089.90 million by 2031, increasing from $ 317.30 million in 2021. Government bodies are focusing on improving healthcare infrastructure and increasing spending on diagnostic lab automation to minimize human error and false results. Furthermore, hospitals and existing diagnostic labs are upgrading testing equipment and devices to increase efficiency. Such factors are driving the demand systems in the market.

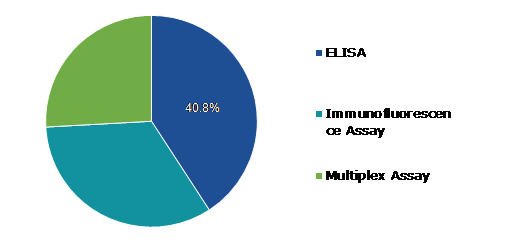

Based on technique, the market has been divided into ELISA, immunofluorescence assay, multiplex assay. Among these, the ELISA sub-segment accounted for highest revenue share in 2021 and is expected to be the fastest growing sub-segment.

Source: Research Dive Analysis

The ELISA sub-segment is anticipated to have a dominant market share and generate a revenue of $2,167.70 million by 2031, growing from $528.50 million in 2021. An ELISA or EIA test is also known as an enzyme-linked immunosorbent assay. The ANA ELISA is used to screen antinuclear antibodies in the specimen. Your body makes antibodies, which are proteins, in reaction to dangerous chemicals known as antigens. The ANA ELISA test is made to detect antibodies against histones, dsDNA, SS-B (La), SS-A (Ro), Smith, Smith/RNP, centromeric proteins, Scl-70, Jo-1, and other antigens extracted from the HEp-2 cell nucleus. Compared to ANA IFAANA, ELISA assays have lower sensitivities for systemic autoimmune rheumatic diseases (SARD). The increasing use of ELISA tests for screening antinuclear antibodies in the specimen is the main factor driving the market.

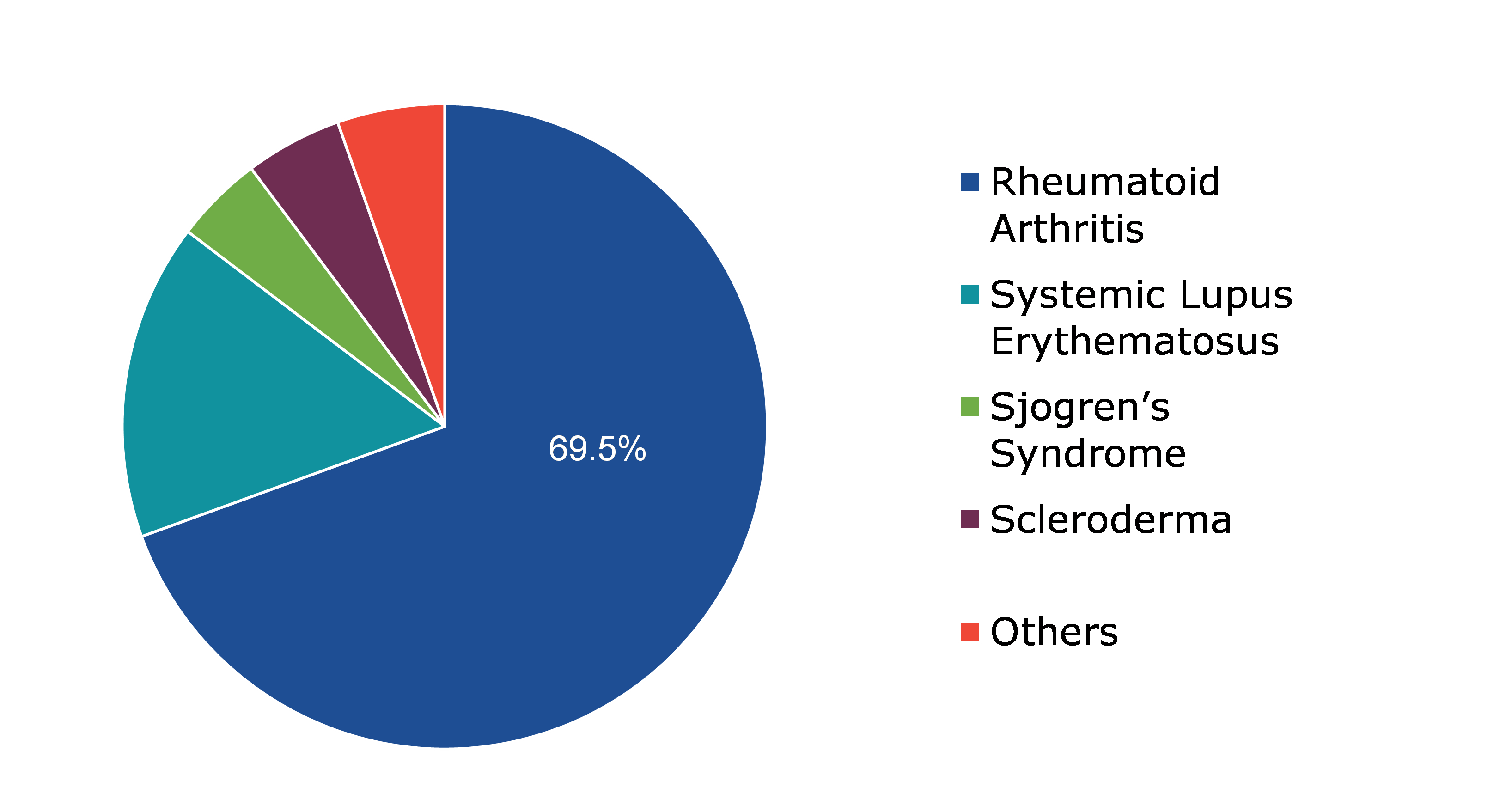

Based on application, the market has been divided into rheumatoid arthritis, systemic lupus erythematosus, sjogren’s syndrome, scleroderma and others. Among these, the rheumatoid arthritis sub-segment accounted for highest revenue share in 2021 and is expected to be the fastest growing sub-segment.

Global Antinuclear Antibody Test Market Share, by Application, 2021

Source: Research Dive Analysis

The rheumatoid arthritis sub-segment is anticipated to have a dominant market share and generate a revenue of $3,622.40 million by 2031, growing from $899.40 million in 2021. Rheumatoid arthritis, also known as RA, is an autoimmune and inflammatory condition in which your immune system unintentionally attacks healthy cells in the body, leading to inflammation (painful swelling) in the areas of the body affected. RA primarily targets the joints, typically several joints at once. Most cases of rheumatoid arthritis are in elderly people. The sub-segment market is anticipated to be driven by the growing geriatric population and increasing rheumatoid arthritis incidences.

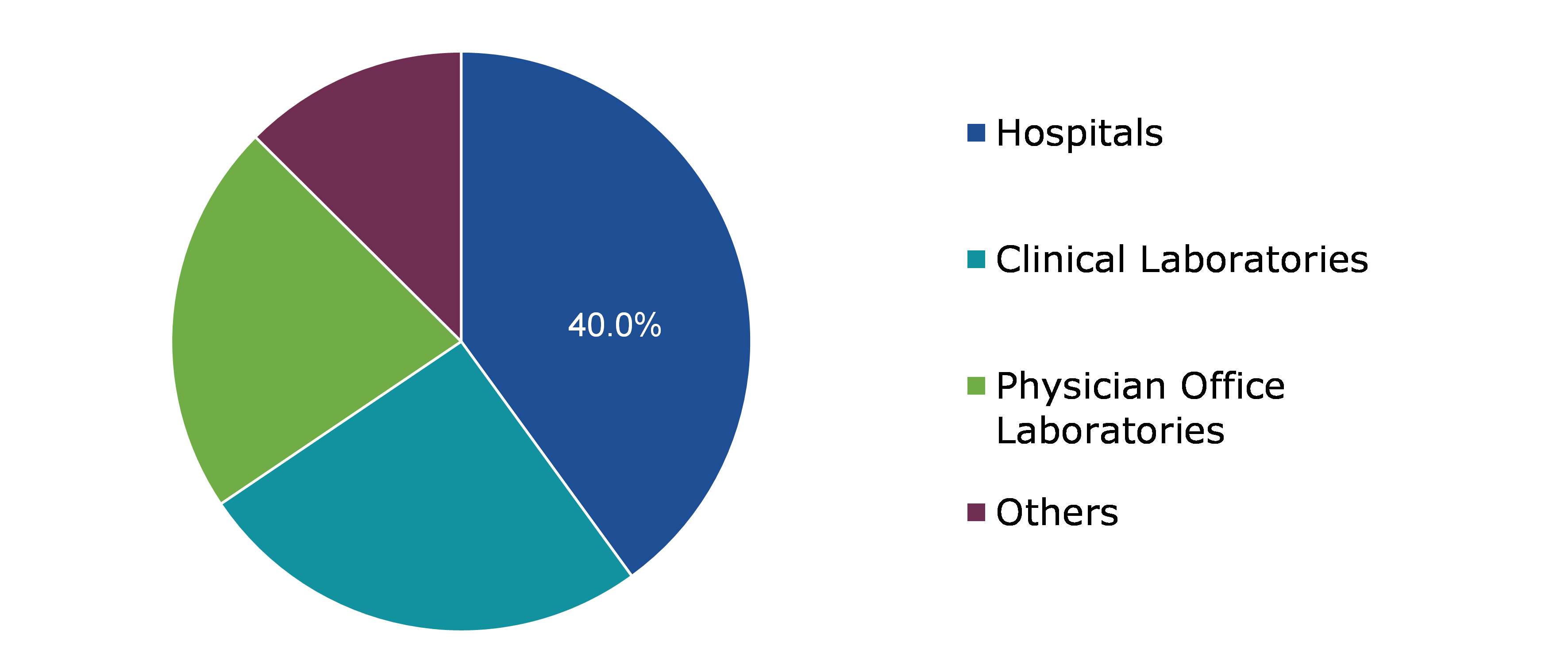

Based on end use, the market has been divided into hospitals, clinical laboratories, physician office laboratories and others. Among these, the hospitals sub-segment accounted for highest revenue share in 2021.

Source: Research Dive Analysis

The hospitals sub-segment is anticipated to have a dominant market share and generate a revenue of $1,907.60 million by 2031, growing from $517.90 million in 2021. High revenue share can be attributed to elements like rising autoimmune disease prevalence and the rising need for fast diagnosis. The hospital sub-segment market is anticipated to be driven by an increase in patient satisfaction, outpatient services, and enhanced home care facilities offered by hospitals throughout the forecasted period.

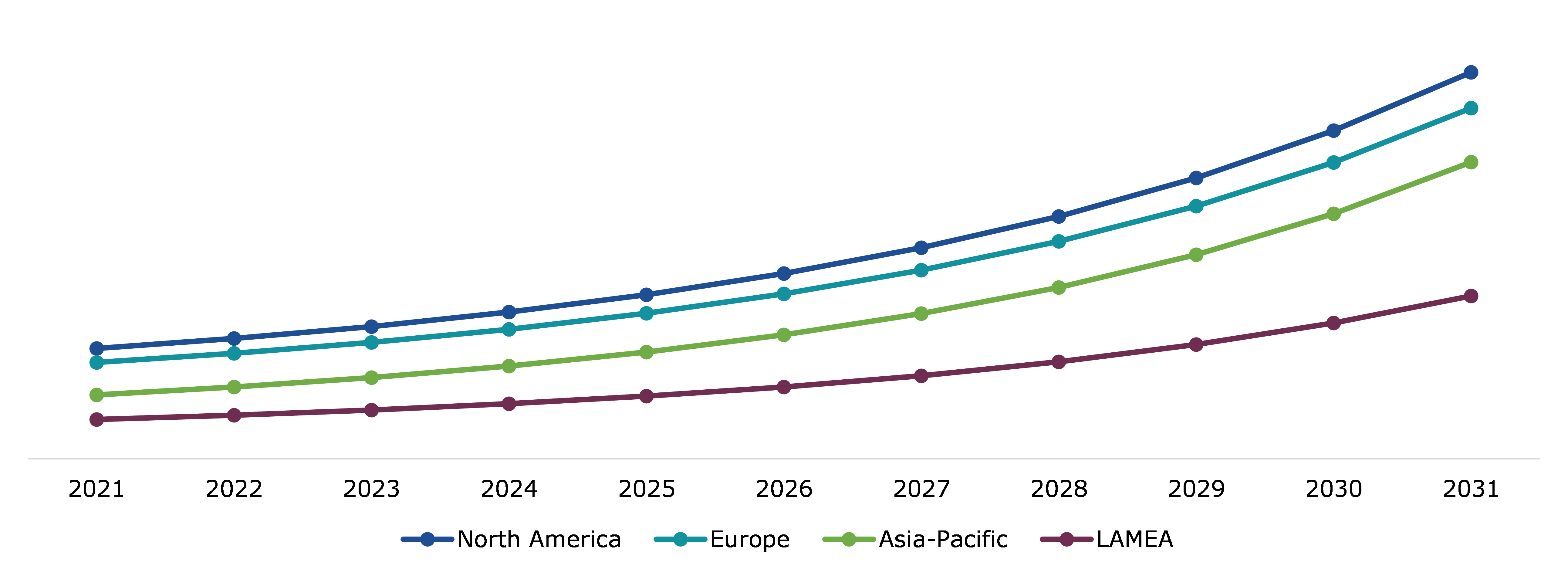

The antinuclear antibody test market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The North America antinuclear antibody test market accounted for $461.00 million in 2021 and is projected to grow with a CAGR of 13.85%. Throughout the entire projection period, North America is anticipated to lead the ANA market. The largest market share within the North American region is anticipated to be held by the United States over the study period. The region has a high demand for early diagnosis and efficient treatment due to several variables, including an aging population that is more susceptible to diseases due to weakened immunity.

The growing investment in the nation will accelerate progress in creating antinuclear antibody tests, further fueling market expansion during the study period. For instance, in November 2021, with the opening of the Colton Center for Autoimmunity in Pennsylvania, Stewart and Judy Colton donated US$10 million to the Perelman School of Medicine at the University of Pennsylvania to support ongoing autoimmune research and care. Increasing the number of ANA testing and rising R&D spending to develop novel tests will drive the market.

Investment and agreement are common strategies followed by major market players. For instance, In June 2022, THERADIAG entered into an agreement with Quotient Limited, a commercial-stage diagnostics company, under which the two companies will partner to advance autoimmune diagnostics by leveraging Quotient’s MosaiQ platform.

Source: Research Dive Analysis

Some of the leading antinuclear antibody test market players are Erba Diagnostics, Bio-Rad Laboratories, Inc., Trinity Biotech Plc., Thermo Fisher Scientific, Antibodies Incorporated, EUROIMMUN Medizinische Labordiagnostika AG, Immuno Concepts NA Ltd., Inova Diagnostics, Inc., Alere Inc. and ZEUS Scientific, Inc.

| Aspect | Particulars |

| Historical Market Estimations | 2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Product |

|

| Segmentation by Technique |

|

| Segmentation by Application |

|

| Segmentation by End-use Industry |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global antinuclear antibody test market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on antinuclear antibody test market

4.7.1.Pre-COVID market scenario

4.7.2.Post-COVID market scenario

5.Antinuclear Antibody Test Market Analysis, by Product

5.1.Overview

5.2.Reagents & Assay Kits

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region, 2021-2031

5.2.3.Market share analysis, by country, 2021-2031

5.3.Systems

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region, 2021-2031

5.3.3.Market share analysis, by country, 2021-2031

5.4.Software & Services

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region, 2021-2031

5.4.3.Market share analysis, by country, 2021-2031

5.5.Research Dive Exclusive Insights

5.5.1.Market attractiveness

5.5.2.Competition heatmap

6.Antinuclear Antibody Test Market Analysis, by Technique

6.1.ELISA

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region, 2021-2031

6.1.3.Market share analysis, by country, 2021-2031

6.2.Immunofluorescence Assay

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region, 2021-2031

6.2.3.Market share analysis, by country, 2021-2031

6.3.Multiplex Assay

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.2.Market size analysis, by region, 2021-2031

6.3.3.Market share analysis, by country, 2021-2031

6.4.Research Dive Exclusive Insights

6.4.1.Market attractiveness

6.4.2.Competition heatmap

7.Antinuclear Antibody Test Market Analysis, by Application

7.1.Rheumatoid Arthritis

7.1.1.Definition, key trends, growth factors, and opportunities

7.1.2.Market size analysis, by region, 2021-2031

7.1.3.Market share analysis, by country, 2021-2031

7.2.Systemic Lupus Erythematosus

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region, 2021-2031

7.2.3.Market share analysis, by country, 2021-2031

7.3.Sjogren’s Syndrome

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region, 2021-2031

7.3.3.Market share analysis, by country, 2021-2031

7.4.Scleroderma

7.4.1.Definition, key trends, growth factors, and opportunities

7.4.2.Market size analysis, by region, 2021-2031

7.4.3.Market share analysis, by country, 2021-2031

7.5.Others

7.5.1.Definition, key trends, growth factors, and opportunities

7.5.2.Market size analysis, by region, 2021-2031

7.5.3.Market share analysis, by country, 2021-2031

7.6.Research Dive Exclusive Insights

7.6.1.Market attractiveness

7.6.2.Competition heatmap

8.Antinuclear Antibody Test Market Analysis, by End-use

8.1.Hospitals

8.1.1.Definition, key trends, growth factors, and opportunities

8.1.2.Market size analysis, by region, 2021-2031

8.1.3.Market share analysis, by country, 2021-2031

8.2. Clinical Laboratories

8.2.1.Definition, key trends, growth factors, and opportunities

8.2.2.Market size analysis, by region, 2021-2031

8.2.3.Market share analysis, by country, 2021-2031

8.3.Physician Office Laboratories

8.3.1.Definition, key trends, growth factors, and opportunities

8.3.2.Market size analysis, by region, 2021-2031

8.3.3.Market share analysis, by country, 2021-2031

8.4.Others

8.4.1.Definition, key trends, growth factors, and opportunities

8.4.2.Market size analysis, by region, 2021-2031

8.4.3.Market share analysis, by country, 2021-2031

8.5.Research Dive Exclusive Insights

8.5.1.Market attractiveness

8.5.2.Competition heatmap

9.Antinuclear Antibody Test Market, by Region

9.1.North America

9.1.1.U.S.

9.1.1.1.Market size analysis, by Product, 2021-2031

9.1.1.2.Market size analysis, by Technique, 2021-2031

9.1.1.3.Market size analysis, by Application, 2021-2031

9.1.1.4.Market size analysis, by End-use, 2021-2031

9.1.2.Canada

9.1.2.1.Market size analysis, by Product, 2021-2031

9.1.2.2.Market size analysis, by Technique, 2021-2031

9.1.2.3.Market size analysis, by Application, 2021-2031

9.1.2.4.Market size analysis, by End-use, 2021-2031

9.1.3.Mexico

9.1.3.1.Market size analysis, by Product, 2021-2031

9.1.3.2.Market size analysis, by Technique, 2021-2031

9.1.3.3.Market size analysis, by Application, 2021-2031

9.1.3.4.Market size analysis, by End-use, 2021-2031

9.1.4.Research Dive Exclusive Insights

9.1.4.1.Market attractiveness

9.1.4.2.Competition heatmap

9.2.Europe

9.2.1.Germany

9.2.1.1.Market size analysis, by Product, 2021-2031

9.2.1.2.Market size analysis, by Technique, 2021-2031

9.2.1.3.Market size analysis, by Application, 2021-2031

9.2.1.4.Market size analysis, by End-use, 2021-2031

9.2.2.UK

9.2.2.1.Market size analysis, by Product, 2021-2031

9.2.2.2.Market size analysis, by Technique, 2021-2031

9.2.2.3.Market size analysis, by Application, 2021-2031

9.2.2.4.Market size analysis, by End-use, 2021-2031

9.2.3.France

9.2.3.1.Market size analysis, by Product, 2021-2031

9.2.3.2.Market size analysis, by Technique, 2021-2031

9.2.3.3.Market size analysis, by Application, 2021-2031

9.2.3.4.Market size analysis, by End-use, 2021-2031

9.2.4.Spain

9.2.4.1.Market size analysis, by Product, 2021-2031

9.2.4.2.Market size analysis, by Technique, 2021-2031

9.2.4.3.Market size analysis, by Application, 2021-2031

9.2.4.4.Market size analysis, by End-use, 2021-2031

9.2.5.Italy

9.2.5.1.Market size analysis, by Product, 2021-2031

9.2.5.2.Market size analysis, by Technique, 2021-2031

9.2.5.3.Market size analysis, by Application, 2021-2031

9.2.5.4.Market size analysis, by End-use, 2021-2031

9.2.6.Rest of Europe

9.2.6.1.Market size analysis, by Product, 2021-2031

9.2.6.2.Market size analysis, by Technique, 2021-2031

9.2.6.3.Market size analysis, by Application, 2021-2031

9.2.6.4.Market size analysis, by End-use, 2021-2031

9.2.7.Research Dive Exclusive Insights

9.2.7.1.Market attractiveness

9.2.7.2.Competition heatmap

9.3.Asia-Pacific

9.3.1.China

9.3.1.1.Market size analysis, by Product, 2021-2031

9.3.1.2.Market size analysis, by Technique, 2021-2031

9.3.1.3.Market size analysis, by Application, 2021-2031

9.3.1.4.Market size analysis, by End-use, 2021-2031

9.3.2.Japan

9.3.2.1.Market size analysis, by Product, 2021-2031

9.3.2.2.Market size analysis, by Technique, 2021-2031

9.3.2.3.Market size analysis, by Application, 2021-2031

9.3.2.4.Market size analysis, by End-use, 2021-2031

9.3.3.India

9.3.3.1.Market size analysis, by Product, 2021-2031

9.3.3.2.Market size analysis, by Technique, 2021-2031

9.3.3.3.Market size analysis, by Application, 2021-2031

9.3.3.4.Market size analysis, by End-use, 2021-2031

9.3.4.Australia

9.3.4.1.Market size analysis, by Product, 2021-2031

9.3.4.2.Market size analysis, by Technique, 2021-2031

9.3.4.3.Market size analysis, by Application, 2021-2031

9.3.4.4.Market size analysis, by End-use, 2021-2031

9.3.5.South Korea

9.3.5.1.Market size analysis, by Product, 2021-2031

9.3.5.2.Market size analysis, by Technique, 2021-2031

9.3.5.3.Market size analysis, by Application, 2021-2031

9.3.5.4.Market size analysis, by End-use, 2021-2031

9.3.6.Rest of Asia-Pacific

9.3.6.1.Market size analysis, by Product, 2021-2031

9.3.6.2.Market size analysis, by Technique, 2021-2031

9.3.6.3.Market size analysis, by Application, 2021-2031

9.3.6.4.Market size analysis, by End-use, 2021-2031

9.3.7.Research Dive Exclusive Insights

9.3.7.1.Market attractiveness

9.3.7.2.Competition heatmap

9.4.LAMEA

9.4.1.Brazil

9.4.1.1.Market size analysis, by Product, 2021-2031

9.4.1.2.Market size analysis, by Technique, 2021-2031

9.4.1.3.Market size analysis, by Application, 2021-2031

9.4.1.4.Market size analysis, by End-use, 2021-2031

9.4.2.Saudi Arabia

9.4.2.1.Market size analysis, by Product, 2021-2031

9.4.2.2.Market size analysis, by Technique, 2021-2031

9.4.2.3.Market size analysis, by Application, 2021-2031

9.4.2.4.Market size analysis, by End-use, 2021-2031

9.4.3.UAE

9.4.3.1.Market size analysis, by Product, 2021-2031

9.4.3.2.Market size analysis, by Technique, 2021-2031

9.4.3.3.Market size analysis, by Application, 2021-2031

9.4.3.4.Market size analysis, by End-use, 2021-2031

9.4.4.South Africa

9.4.4.1.Market size analysis, by Product, 2021-2031

9.4.4.2.Market size analysis, by Technique, 2021-2031

9.4.4.3.Market size analysis, by Application, 2021-2031

9.4.4.4.Market size analysis, by End-use, 2021-2031

9.4.5.Rest of LAMEA

9.4.5.1.Market size analysis, by Product, 2021-2031

9.4.5.2.Market size analysis, by Technique, 2021-2031

9.4.5.3.Market size analysis, by Application, 2021-2031

9.4.5.4.Market size analysis, by End-use, 2021-2031

9.4.6.Research Dive Exclusive Insights

9.4.6.1.Market attractiveness

9.4.6.2.Competition heatmap

10.Competitive Landscape

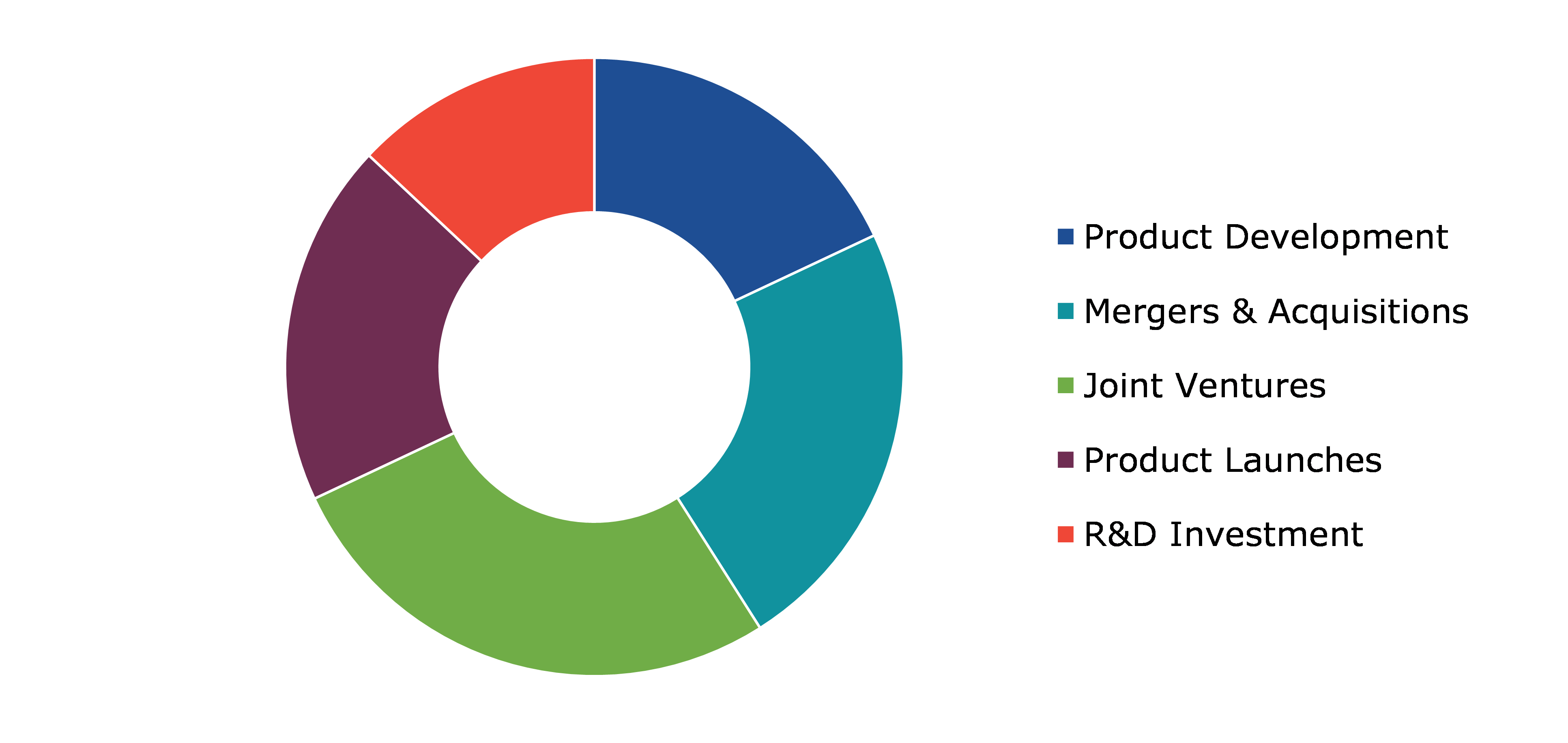

10.1.Top winning strategies, 2021

10.1.1.By strategy

10.1.2.By year

10.2.Strategic overview

10.3.Market share analysis, 2021

11.Company Profiles

11.1.Erba Diagnostics

11.1.1.Overview

11.1.2.Business segments

11.1.3.Product portfolio

11.1.4.Financial performance

11.1.5.Recent developments

11.1.6.SWOT analysis

11.2.Bio-Rad Laboratories, Inc.

11.2.1.Overview

11.2.2.Business segments

11.2.3.Product portfolio

11.2.4.Financial performance

11.2.5.Recent developments

11.2.6.SWOT analysis

11.3.Trinity Biotech Plc.

11.3.1.Overview

11.3.2.Business segments

11.3.3.Product portfolio

11.3.4.Financial performance

11.3.5.Recent developments

11.3.6.SWOT analysis

11.4.Thermo Fisher Scientific

11.4.1.Overview

11.4.2.Business segments

11.4.3.Product portfolio

11.4.4.Financial performance

11.4.5.Recent developments

11.4.6.SWOT analysis

11.5.Antibodies Incorporated

11.5.1.Overview

11.5.2.Business segments

11.5.3.Product portfolio

11.5.4.Financial performance

11.5.5.Recent developments

11.5.6.SWOT analysis

11.6.EUROIMMUN Medizinische Labordiagnostika AG

11.6.1.Overview

11.6.2.Business segments

11.6.3.Product portfolio

11.6.4.Financial performance

11.6.5.Recent developments

11.6.6.SWOT analysis

11.7.Immuno Concepts NA Ltd.

11.7.1.Overview

11.7.2.Business segments

11.7.3.Product portfolio

11.7.4.Financial performance

11.7.5.Recent developments

11.7.6.SWOT analysis

11.8.Inova Diagnostics, Inc.

11.8.1.Overview

11.8.2.Business segments

11.8.3.Product portfolio

11.8.4.Financial performance

11.8.5.Recent developments

11.8.6.SWOT analysis

11.9.ZEUS Scientific, Inc.

11.9.1.Overview

11.9.2.Business segments

11.9.3.Product portfolio

11.9.4.Financial performance

11.9.5.Recent developments

11.9.6.SWOT analysis

11.10.Alere Inc.

11.10.1.Overview

11.10.2.Business segments

11.10.3.Product portfolio

11.10.4.Financial performance

11.10.5.Recent developments

11.10.6.SWOT analysis

12.Appendix

12.1.Parent & peer market analysis

12.2.Premium insights from industry experts

12.3.Related reports

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}