Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

MA20116481 |

Pages: 220 |

Feb 2023 |

Alpha olefins market is gaining significant popularity as it is used for production of polyethylene lubricants, detergents, plasticizers, oil field chemicals, and fine chemicals. Olefins, also referred to as alkenes, are hydrocarbons that have one or more double bonds between two adjacent carbon atoms. This term is typically used to describe hydrocarbons with at least one double bond. The regularity of the hydrocarbon chain and the placement of the double bond at the main, or alpha, position distinguish alpha olefins from other mono-olefins with a similar molecular formula. Alpha olefins are olefins or alkenes having the chemical formula CnH2n. The Alpha olefins market size is expected to increase due to the rise in demand from the automotive industry, which is a significant market driver. These factors are anticipated to boost the alpha olefins industry growth in the upcoming years.

However, the biggest market restraint is believed to be the component's manufacturing process. The process requires extremely high pressures and temperatures. Incorrect pressure and temperature adjustments could lead to a product fault that makes it useless and causes a large loss for the manufacturing company. These factors are anticipated to hinder the alpha olefins market growth.

As alpha olefins are used more often across a variety of industries, there is an increase in global alpha olefin consumption. The major corporations are prepared to invest significantly in the research and development of alpha olefins. Due to their multiple uses in industries such as consumer goods, packaging, and industrial processes, alpha olefins market share are expected to experience growth in the next years.

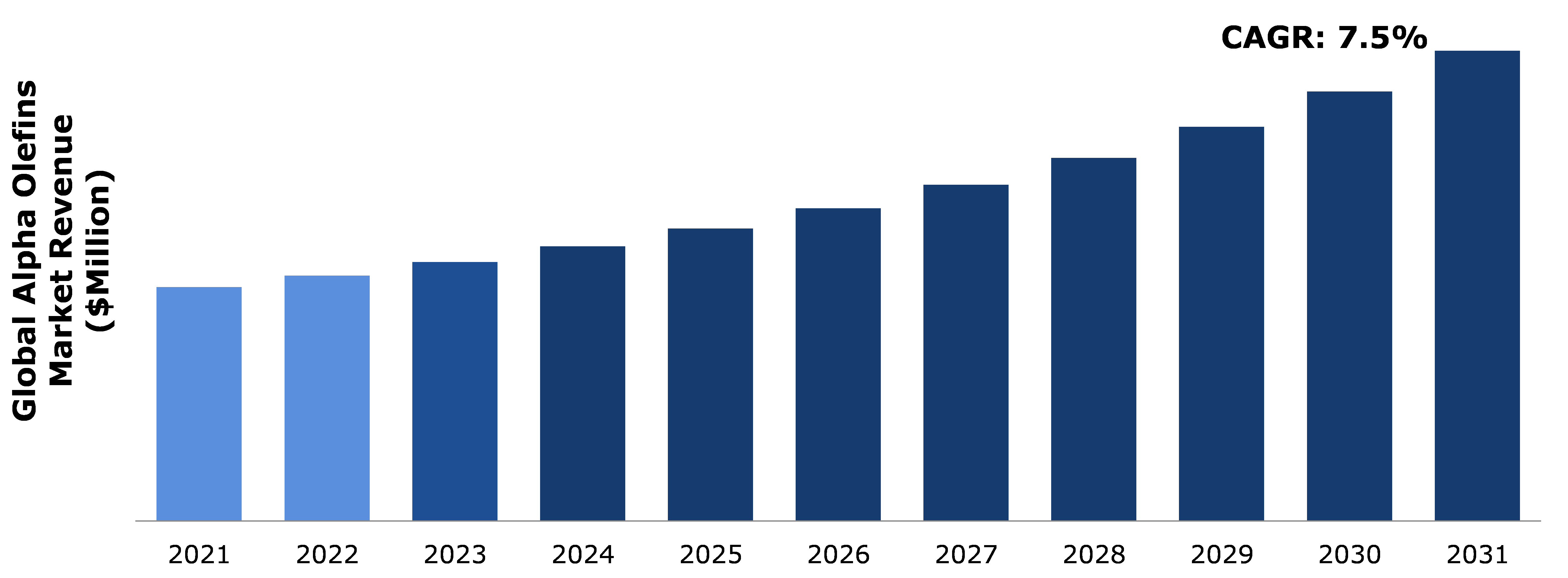

According to regional analysis, the North America alpha olefins market revenue accounted for $1,377.1million in 2021 and is predicted to grow with a CAGR of 8.1% in the projected timeframe.

Olefins are hydrocarbons with one or more double bonds between two adjacent carbon atoms, often known as alkenes. In most cases, this word is used to refer to hydrocarbons that include at least one double bond. Alpha-olefins are a class of organic compounds with the chemical formula CxH2x that are alkenes. They are differentiated by having a double bond in the primary position. The compound's increased reactivity at this site of a double bond makes it suitable for a variety of uses. Alpha-olefins are important building blocks in the production of various industrial chemicals. Detergents and plasticizers are produced mostly from medium- or long-chain derivatives.

The COVID-19 pandemic created several uncertainties, resulting in significant economic losses as various businesses around the world came to a halt. This has ultimately lowered the demand for alpha olefins due to disruptions in supply chain, closure of manufacturing plants, and economic slowdown across several countries. In addition, the import-export restrictions were laid down on major alpha olefins producing countries such as the U.S. and China. Furthermore, the automotive sector suffered the greatest impact in terms of sales and project acquisition, resulting in a significant decrease in alpha olefins demand. For instance, in construction industry, several construction projects were postponed or cancelled due to shortages of raw materials, labor, fear of contracting the COVID-19 virus among workers, as well as travel restrictions. Similarly, in the automotive sector, alpha olefins are used as lubricant and for making various components of automobile. However, disruptions in the exports of automotive parts from China as well as closure of automotive assembly and manufacturing units have hampered the alpha olefins market share during the pandemic.

Alpha olefins are excellent materials for producing a variety of goods because they have easily accessible terminal double bonds. Regular alpha olefins or their derivatives are widely employed as plasticizers, surfactants, automotive additives, synthetic motor oils, lubricants, paper sizes, and in a variety of specialized applications. The market for liner alpha olefins is thought to be primarily driven by rise in polyethylene use and surge in alpha olefin demand from the automotive industry. Alpha olefin end products are mostly used in the automotive industry. The alpha olefin's final products, which are utilized in the automotive industry for managing and keeping spare components in motor vehicles, include plasticizers, lubricants, surfactants, and oil chemicals. These spare parts are utilized in cars to increase their longevity.

The process used to manufacture the component is thought to be the main market constraint. Extreme pressure and temperature requirements are part of the process. Implementing incorrect pressure and temperature variations might result in a product flaw that renders it worthless and results in a significant loss for the production organization. The alpha olefins sector is thought to be greatly impacted by changes in raw material pricing. The cost of production will increase as a result of the rise in price of raw materials, which will also drive up the cost of manufacturing as a whole. Therefore, the growth of the alpha olefins industry will be hampered by the increase in manufacturing costs caused by the increase in the price of alpha olefin.

The main usage of alpha olefins is as co-monomers in the manufacture of polyethylene, Alpha olefins also have significant uses as synthetic lubricants, detergent intermediates, plasticizers, oil-field chemicals, and paper sizing chemicals. Every end-use or application market differs in terms of growth, per capita consumption, regional or national coverage, customer base, required levels of quality, available distribution channels, and off-take volumes. This makes the alpha olefins industry tough and complex because manufacturers must balance the need to supply the alpha olefins end markets with the need to maximize income throughout the full range of all alpha olefin product fractions. The higher demand for alpha olefins demonstrates regional variations in market volume and the ratio of higher alpha olefins for detergent and lubricant applications.

To know more about global alpha olefins market opportunities, get in touch with our analysts here.

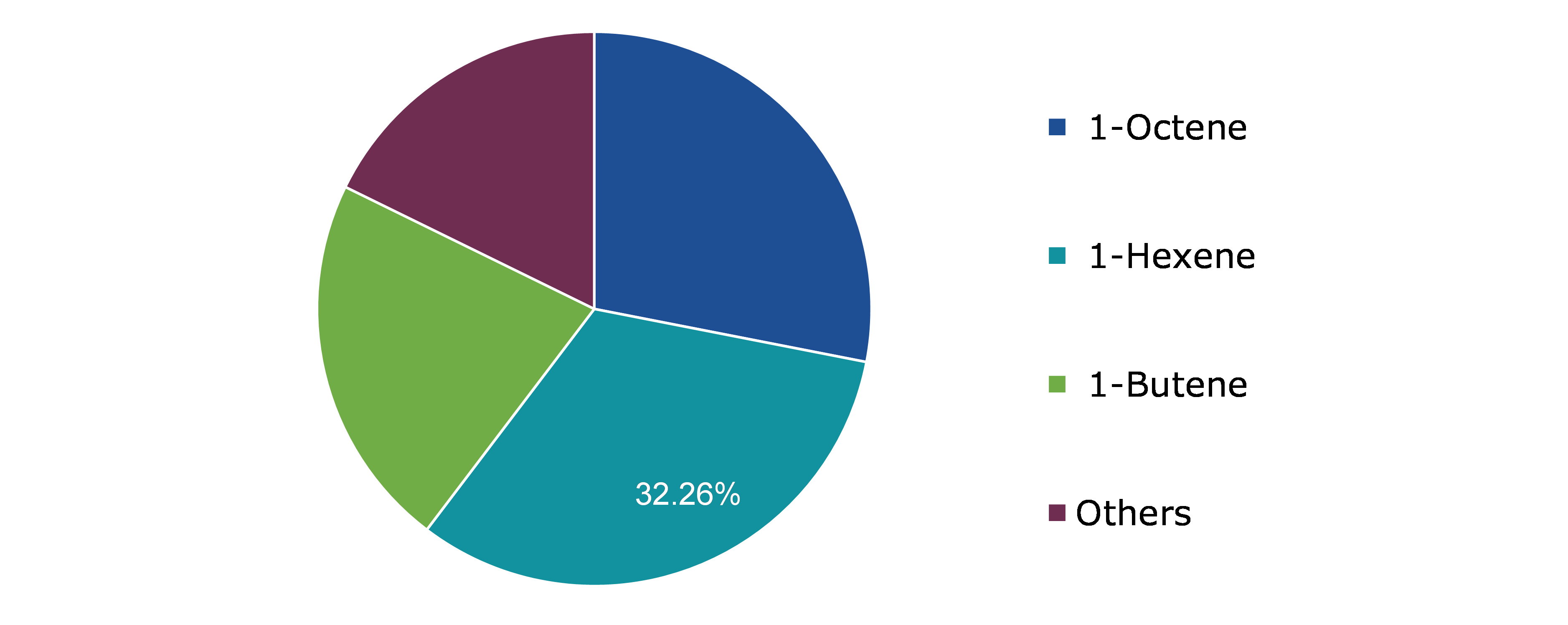

Based on product, the market has been divided into 1-Octene, 1-Hexene, 1-Butene, and Others. Among these, the 1-Hexene sub-segment accounted for the highest market share in 2021, whereas the coal sub-segment is estimated to show the fastest growth during the forecast period.

Source: Research Dive Analysis

The 1-Hexene sub-type is anticipated to have a dominant market share in 2021.1-hexene is an alpha-olefin with an alpha double bond, providing the compound increased with reactivity and thus beneficial chemical properties. A significant linear alpha olefin for commerce is 1-hexene, which is primarily used as a comonomer in the production of polyethene. Making linear aldehyde through hydroformylation and then converting it into the short-chain fatty acid heptanoic acid is another significant use of 1-hexene. In addition to being used to make synthetic fatty acids and oxy alcohols, 1-hexene is also primarily used in the synthesis of polyethylene and plasticizers. Thus, it is anticipated that the hexane sector will benefit from the rising demand for polyethylene caused by expansion in the packaging industry.

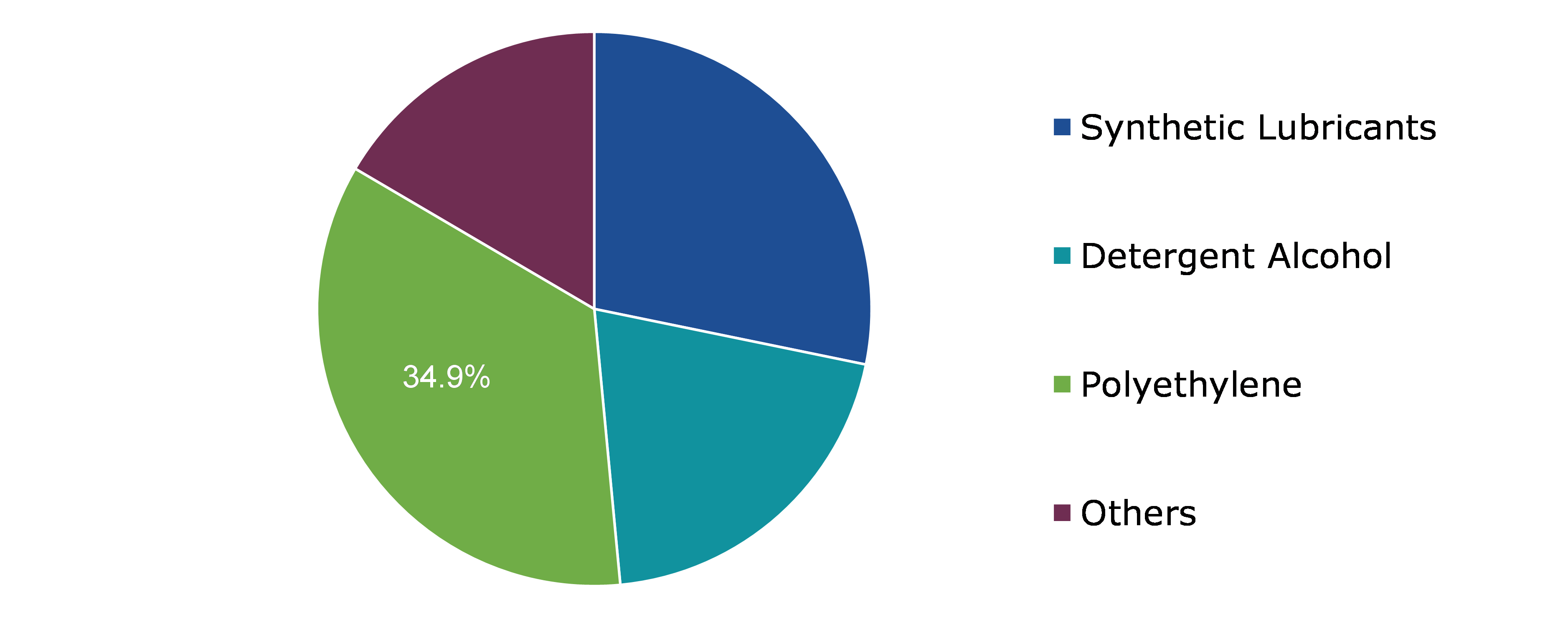

Based on application, the market has been divided into synthetic lubricants, detergent alcohol, polyethylene, and others. Among these, the synthetic lubricants sub-segment accounted for the highest revenue share in 2021.

Source: Research Dive Analysis

The polyethylene sub-segment is anticipated to have a dominant market share in 2021. Polyethylene has become the most significant polyolefin plastic due to its outstanding mechanical, processing, and chemical stability. It is employed in the creation of pipe, packing, and film. One of the top five synthetic resins produced and consumed worldwide is polyethylene. Polyethylene is a synthetic polymer that is often used in packaging materials such plastic bottles, films, bags, and containers. These factors are anticipated to boost the growth of automotive sub-segment during the analysis timeframe.

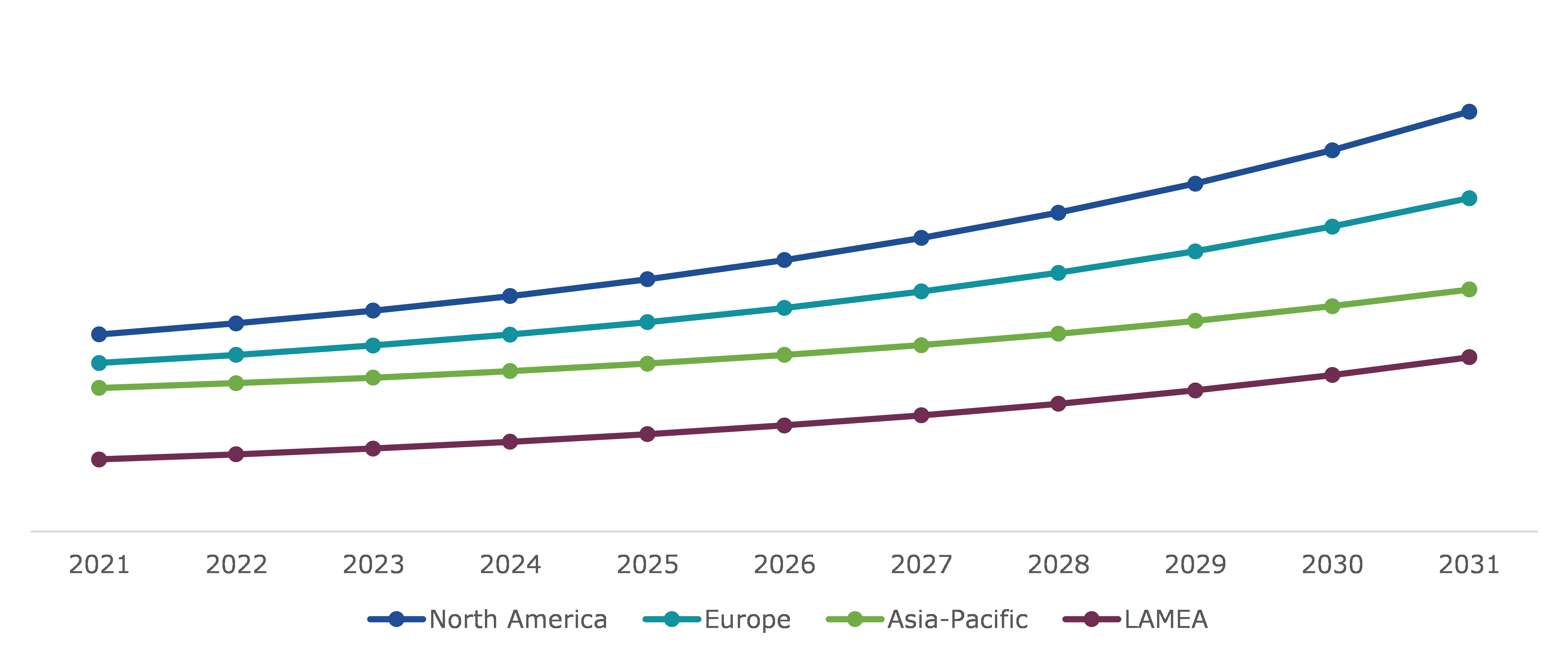

The alpha olefins market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

North America accounted for the largest market for alpha olefins, and the demand for polyethylene is driven by sectors such as the automotive, packaging, and electrical & electronics industries. To fulfill the growing demand and improve profit margins, the alpha olefins sector is implementing a number of technological advancements and expansions. Due to the extraction of shale gas and the availability of cheap raw materials, the market in this area has a high growth potential. For instance, on March 23, 2022, ExxonMobil announced plans to build the unit at its integrated petrochemical facility in Baytown, Texas, in the U.S. The new unit will start up commercially in 2023 and generate about 350,000 metric tons of linear alpha olefins annually.

Investment and agreement are common strategies followed by major market players. For instance, Chevron Phillips Chemical has made plans to grow its alpha olefins business by constructing a second, large-scale facility to create 1-Hexene for specific uses. This facility is expected to be operational by 2023.

Source: Research Dive Analysis

Some of the leading alpha olefins market players are Qatar Chemical Company Ltd. (Q-chem)., Chevron Phillips Chemical Company LLC, Mitsubishi Chemical Corp, Exxon Mobil Corporation, INEOS Oligomers, Petrochemicals Sdn. Bhd., Royal Dutch Shell, Evonik Industries, and JAM Petrochemicals Company.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Product |

|

| Segmentation by Application |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global alpha olefins market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on alpha olefins market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Alpha Olefins Market Analysis, by Product

5.1.Overview

5.2.1-Octane

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.1.1.Market size analysis, by region, 2022-2031

5.2.1.2.Market share analysis, by country, 2022-2031

5.3.1-Hexene

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.1.1.Market size analysis, by region, 2022-2031

5.3.1.2.Market share analysis, by country, 2022-2031

5.4.1-Butene

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.1.1.Market size analysis, by region, 2022-2031

5.4.1.2.Market share analysis, by country, 2022-2031

5.5.Others

5.5.1.Definition, key trends, growth factors, and opportunities

5.5.1.1.Market size analysis, by region, 2022-2031

5.5.1.2.Market share analysis, by country, 2022-2031

5.6.Research Dive Exclusive Insights

5.6.1.Market attractiveness

5.6.2.Competition heatmap

6.Alpha Olefins Analysis, by Application

6.1.Synthetic Lubricants

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.1.1.Market size analysis, by region, 2022-2031

6.1.1.2.Market share analysis, by country, 2022-2031

6.2.Detergent Alcohol

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.1.1.Market size analysis, by region, 2022-2031

6.2.1.2.Market share analysis, by country, 2022-2031

6.3.Polyethylene

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.1.1.Market size analysis, by region, 2022-2031

6.3.1.2.Market share analysis, by country, 2022-2031

6.4.Others

6.4.1.Definition, key trends, growth factors, and opportunities

6.4.1.1.Market size analysis, by region, 2022-2031

6.4.1.2.Market share analysis, by country, 2022-2031

6.5.Research Dive Exclusive Insights

6.5.1.Market attractiveness

6.5.2.Competition heatmap

7.Methanol Market, by Region

7.1.North America

7.1.1.U.S.

7.1.1.1.Market size analysis, by Product, 2022-2031

7.1.1.2.Market size analysis, by Application, 2022-2031

7.1.2.Canada

7.1.2.1.Market size analysis, by Product, 2022-2031

7.1.2.2.Market size analysis, by Application, 2022-2031

7.1.3.Mexico

7.1.3.1.Market size analysis, by Product, 2022-2031

7.1.3.2.Market size analysis, by Application, 2022-2031

7.1.4.Research Dive Exclusive Insights

7.1.4.1.Market attractiveness

7.1.4.2.Competition heatmap

7.2.Europe

7.2.1.Germany

7.2.1.1.Market size analysis, by Product, 2022-2031

7.2.1.2.Market size analysis, by Application, 2022-2031

7.2.2.UK

7.2.2.1.Market size analysis, by Product, 2022-2031

7.2.2.2.Market size analysis, by Application, 2022-2031

7.2.3.France

7.2.3.1.Market size analysis, by Product, 2022-2031

7.2.3.2.Market size analysis, by Application, 2022-2031

7.2.4.Spain

7.2.4.1.Market size analysis, by Product, 2022-2031

7.2.4.2.Market size analysis, by Application, 2022-2031

7.2.5.Italy

7.2.5.1.Market size analysis, by Product, 2022-2031

7.2.5.2.Market size analysis, by Application, 2022-2031

7.2.6.Rest of Europe

7.2.6.1.Market size analysis, by Product, 2022-2031

7.2.6.2.Market size analysis, by Application, 2022-2031

7.2.7.Research Dive Exclusive Insights

7.2.7.1.Market attractiveness

7.2.7.2.Competition heatmap

7.3.Asia Pacific

7.3.1.China

7.3.1.1.Market size analysis, by Product, 2022-2031

7.3.1.2.Market size analysis, by Application, 2022-2031

7.3.2.Japan

7.3.2.1.Market size analysis, by Product, 2022-2031

7.3.2.2.Market size analysis, by Application, 2022-2031

7.3.3.India

7.3.3.1.Market size analysis, by Product, 2022-2031

7.3.3.2.Market size analysis, by Application, 2022-2031

7.3.4.Australia

7.3.4.1.Market size analysis, by Product, 2022-2031

7.3.4.2.Market size analysis, by Application, 2022-2031

7.3.5.South Korea

7.3.5.1.Market size analysis, by Product, 2022-2031

7.3.5.2.Market size analysis, by Application, 2022-2031

7.3.6.Rest of Asia Pacific

7.3.6.1.Market size analysis, by Product, 2022-2031

7.3.6.2.Market size analysis, by Application, 2022-2031

7.3.7.Research Dive Exclusive Insights

7.3.7.1.Market attractiveness

7.3.7.2.Competition heatmap

7.4.LAMEA

7.4.1.Brazil

7.4.1.1.Market size analysis, by Product, 2022-2031

7.4.1.2.Market size analysis, by Application, 2022-2031

7.4.2.Saudi Arabia

7.4.2.1.Market size analysis, by Product, 2022-2031

7.4.2.2.Market size analysis, by Application, 2022-2031

7.4.3.UAE

7.4.3.1.Market size analysis, by Product, 2022-2031

7.4.3.2.Market size analysis, by Application, 2022-2031

7.4.4.South Africa

7.4.4.1.Market size analysis, by Product, 2022-2031

7.4.4.2.Market size analysis, by Application, 2022-2031

7.4.5.Rest of LAMEA

7.4.5.1.Market size analysis, by Product, 2022-2031

7.4.5.2.Market size analysis, by Application, 2022-2031

7.4.6.Research Dive Exclusive Insights

7.4.6.1.Market attractiveness

7.4.6.2.Competition heatmap

8.Competitive Landscape

8.1.Top winning strategies, 2021

8.1.1.By strategy

8.1.2.By year

8.2.Strategic overview

8.3.Market share analysis, 2021

9.Company Profiles

9.1.Qatar Chemical Company Ltd (Q-chem).

9.1.1.Overview

9.1.2.Business segments

9.1.3.Product portfolio

9.1.4.Financial performance

9.1.5.Recent developments

9.1.6.SWOT analysis

9.2.Chevron Phillips Chemical Company LLC

9.2.1.Overview

9.2.2.Business segments

9.2.3.Product portfolio

9.2.4.Financial performance

9.2.5.Recent developments

9.2.6.SWOT analysis

9.3.Mitsubishi Chemical Corp

9.3.1.Overview

9.3.2.Business segments

9.3.3.Product portfolio

9.3.4.Financial performance

9.3.5.Recent developments

9.3.6.SWOT analysis

9.4.Exxon Mobil Corporation

9.4.1.Overview

9.4.2.Business segments

9.4.3.Product portfolio

9.4.4.Financial performance

9.4.5.Recent developments

9.4.6.SWOT analysis

9.5.INEOS Oligomers

9.5.1.Overview

9.5.2.Business segments

9.5.3.Product portfolio

9.5.4.Financial performance

9.5.5.Recent developments

9.5.6.SWOT analysis

9.6.Petrochemicals Sdn. Bhd

9.6.1.Overview

9.6.2.Business segments

9.6.3.Product portfolio

9.6.4.Financial performance

9.6.5.Recent developments

9.6.6.SWOT analysis

9.7.Royal Dutch Shell

9.7.1.Overview

9.7.2.Business segments

9.7.3.Product portfolio

9.7.4.Financial performance

9.7.5.Recent developments

9.7.6.SWOT analysis

9.8.Evonik Industries

9.8.1.Overview

9.8.2.Business segments

9.8.3.Product portfolio

9.8.4.Financial performance

9.8.5.Recent developments

9.8.6.SWOT analysis

9.9.JAM Petrochemicals

9.9.1.Overview

9.9.2.Business segments

9.9.3.Product portfolio

9.9.4.Financial performance

9.9.5.Recent developments

9.9.6.SWOT analysis

10.Appendix

10.1.Parent & peer market analysis

10.2.Premium insights from industry experts

10.3.Related reports

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}