Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

LI2010414 |

Pages: 220 |

Jul 2022 |

As the need for cleanliness and sanitation in the medical sector is rising every day, the market for biohazard bags is becoming more popular. Biohazard bags are recyclable and disposable bags. These bags are available in four different colors for different types of waste which include yellow, blue, black, and red. These bags are used for discarding of infectious waste and the treatment of items such as wound bandages, cotton, used swab collection kits, and others that have been contaminated by infectious waste. Medical waste is collected in these bags for disposal and waste management. Serious health problems may occur due to improper management of the biohazard waste collected in these bags, which may eventually lead to an increase in number of patients in the hospital, drug development research, clinical disease testing, and the pharmaceutical industry. Due to this issue, there will be requirement for proper garbage disposal methods and containers. In order to prevent punctures from sharp things, biohazard waste bags are typically made using materials such as High Density Polyethylene (HPDE). Low Density Polyethylene (LDPE) has a high impact strength and exceptional chemical resistance. These factors are expected to increase the demand for the biohazard bags in the market.

However, some factors such as improper waste management of these biohazard bags can cause health problems and at times this mismanagement of waste can cause chronic diseases such as HIV, tuberculosis, cancer, and even chemical burns.

Due to the healthcare industry’s rapid expansion and increased need for sanitation due to COVID-19, requirement for waste disposal systems is ultimately rising, which is driving a significant global increase in the biohazard bags market growth. These bags are made with durable plastic and these bags are recyclable as well. Low-density polyethylene bags with sterilizing storage are typically used to hold all types of solid and liquid waste. High temperature bags, light-sensitive sample holding bags, and sealable flip bags are varieties available. In the upcoming years, these variables may offer attractive chances for the global biohazard bags market.

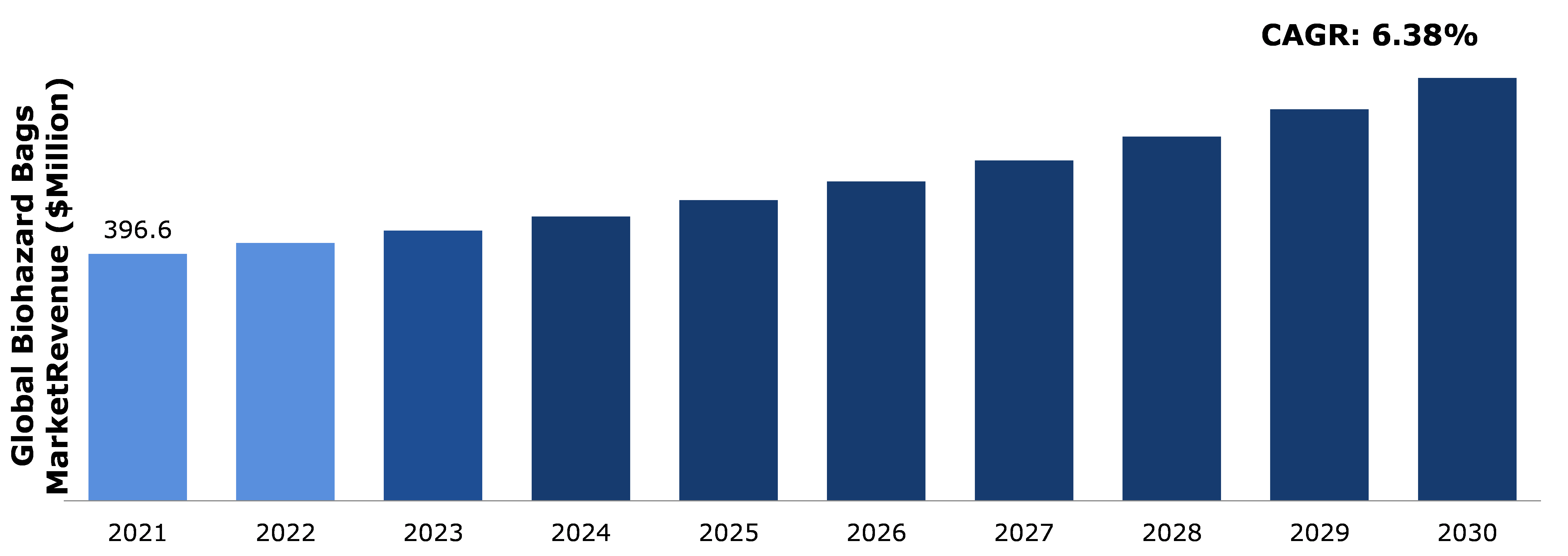

According to regional analysis, the North America biohazard bags market size accounted for $126.1 million in 2021 and is predicted to grow with a CAGR of 5.89% in the projected timeframe.

Biohazard bags are sustainable bags made from strong plastic. Hazardous medical wastes, such as blood products, chemical substances, toxic substances, as well as hazardous compounds among others, are collected and disposed by using biohazard bags. These bags are widely used in hospitals, clinical laboratories as well as research centers to dispose and carry the waste produced in these facilities to the waste management centers and incineration centers.

The COVID-19 pandemic's spread has resulted in an increase in demand for biohazard bags due to requirement to preserve hygiene and cleanliness. Ministry of Environment, Forest and Climate Change, India, revised and amended guidelines for biomedical waste management in 2019, by adding and restructuring new rules. Number of governmental and non-governmental organizations, as well as healthcare institutions such as hospitals, clinics, and medical labs, are making considerable efforts to stop the coronavirus from spreading. Increased death rate during the pandemic increased biohazard waste produced at funeral homes as well as autopsy centers, which resulted in increased demand for the biohazard bags for the disposal. As a result, there is a rising need for biohazard bags in the forecast period, which will boost expansion of the global biohazard bags market.

Moreover, there has been an increase in number of safety rules and standards imposed by governments of various countries during the pandemic to avoid spread of COVID-19. Rules such as compulsion on wearing of mask, use of PPE kits, rapid tests or COVID test before traveling were imposed. This lead to increase in the volume of biohazard waste cross the world. Doctors were working throughout the pandemic and were provided with safety kits. These safety kits contained masks, PPE kits, face shield, gloves, caps, and others. These safety gears were onetime use and meant to be disposed after use, resulting in increasing demand for biohazard bags in near future.

In one year from June 2020 – June 2021, India generated 56,898 tons of COVID-19 bio medical waste as per the data released by the Ministry of Environment, Forest and Climate Change. In U.S., more than five million tons of medical waste is produced every year. This waste is produced by hospitals, pathological laboratories, nursing homes, clinics, as well as healthcare facilities and it is important to dispose and manage properly. In the process of disposal of medical waste, biohazard bags play important role to collect, carry, and dispose them. These bags can contain sharp objects used for medical purpose such as needles, scissors, glass bottles, ampules, injections, cotton, wound care bandages, blood, surgical waste, and used safety gears such as masks, gloves, PPE kits, and others. Such waste is produced daily and the volume of this waste production is increasing daily which is resulting in increased requirement of biohazard bags. These factors are expected to boost the global biohazard bags market size in near future.

In countries such as Sri Lanka, Madagascar, Niger, Pakistan, Cambodia, and others awareness regarding use of biohazard bags and their disposal is less. Improper biohazard waste management in these countries can cause serious health issues and chronic diseases as well as can contaminate the environment. These are one of the major restricting factors for revenue growth of the biohazard bags market.

Countries such as India, Brazil, Myanmar, Thailand, Turkey, and others are focusing more on the healthcare sector as it is one of the most important sectors which contributes for the development of nation. In Indian budget 2022, budget of more than $10 billion (86,200 crores) was allocated to the healthcare sector. The COVID-19 pandemic was eye opener calamity for development of healthcare system around the world. Developing healthcare industry around the globe is resulting in increasing volume of the waste produced by these organizations. For the proper management of biomedical waste produced by these organizations, biohazard bags play important role. All the medical and hazardous waste produced can be disposed with the help of biohazard bags and these factors are likely to create growth opportunities for major players in the global biohazard bags market.

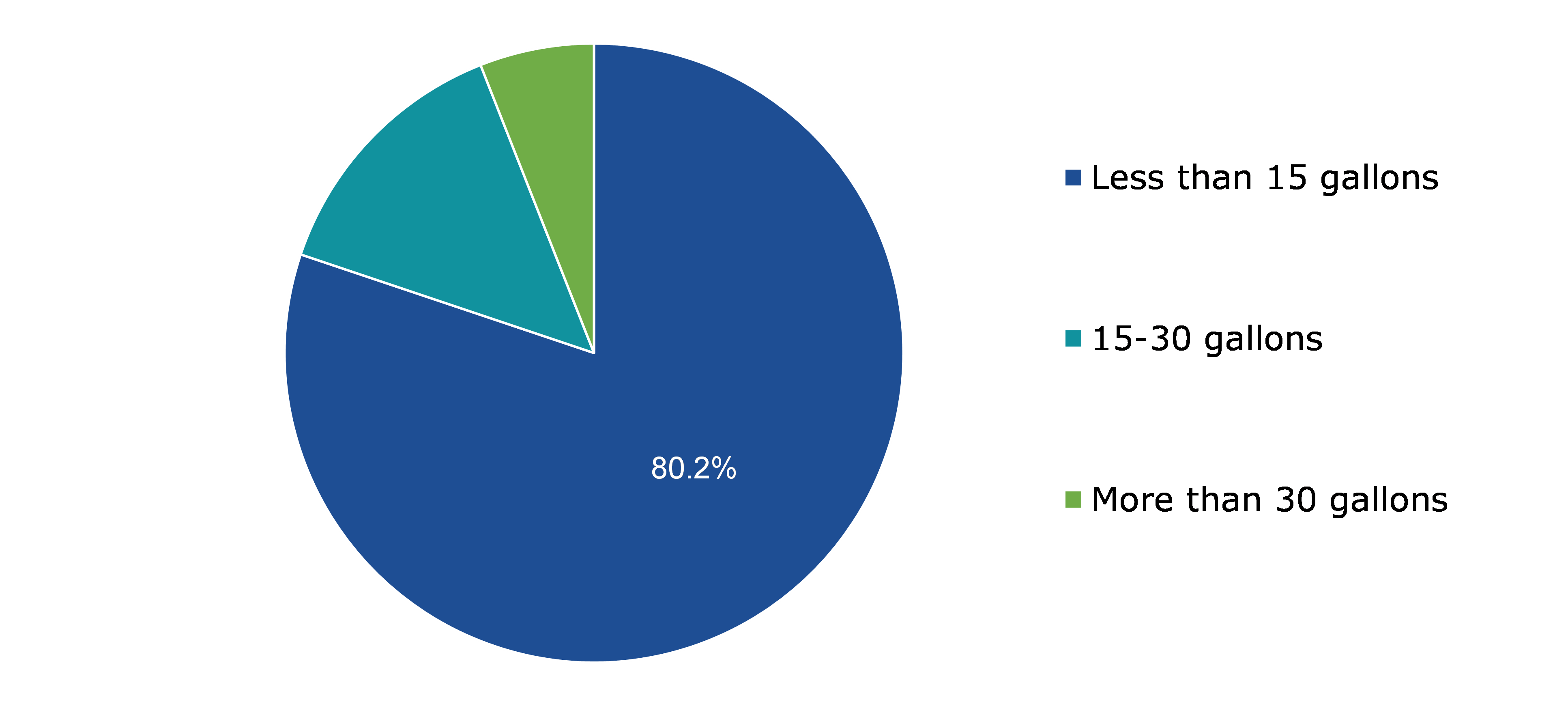

Based on capacity type, biohazard bags market share is further divided into less than 15 gallon, 15 to 35 gallon, and more than 35 gallon. Among these, less than 15 gallon sub-segment is expected to be fastest growing and dominating during the forecast period.

Source: Research Dive Analysis

The less than 15 gallon sub-segment is expected to be fastest growing and generate a revenue of $552.7 million by 2030, growing from $317.9 million in 2021. Less than 15 gallon biohazard bags are mostly used in hospitals, pathological laboratories, medical facilities, and nursing homes. These bags can be used for the effective collection of infectious agents from labs, waste from ill patients, used testing kits, swabs, used bandages, and others.

These bags are made with thick plastic to avoid the leakages and spills. These bags are tough and cannot be easily tore. Less than 15 gallon biohazard bags are printed with the world wide recognized biohazard symbols. Increased use of safety gears and necessity for the rapid test for COVID-19 as well as increasing production medical waste are factors expected to drive the market growth in analysis period.

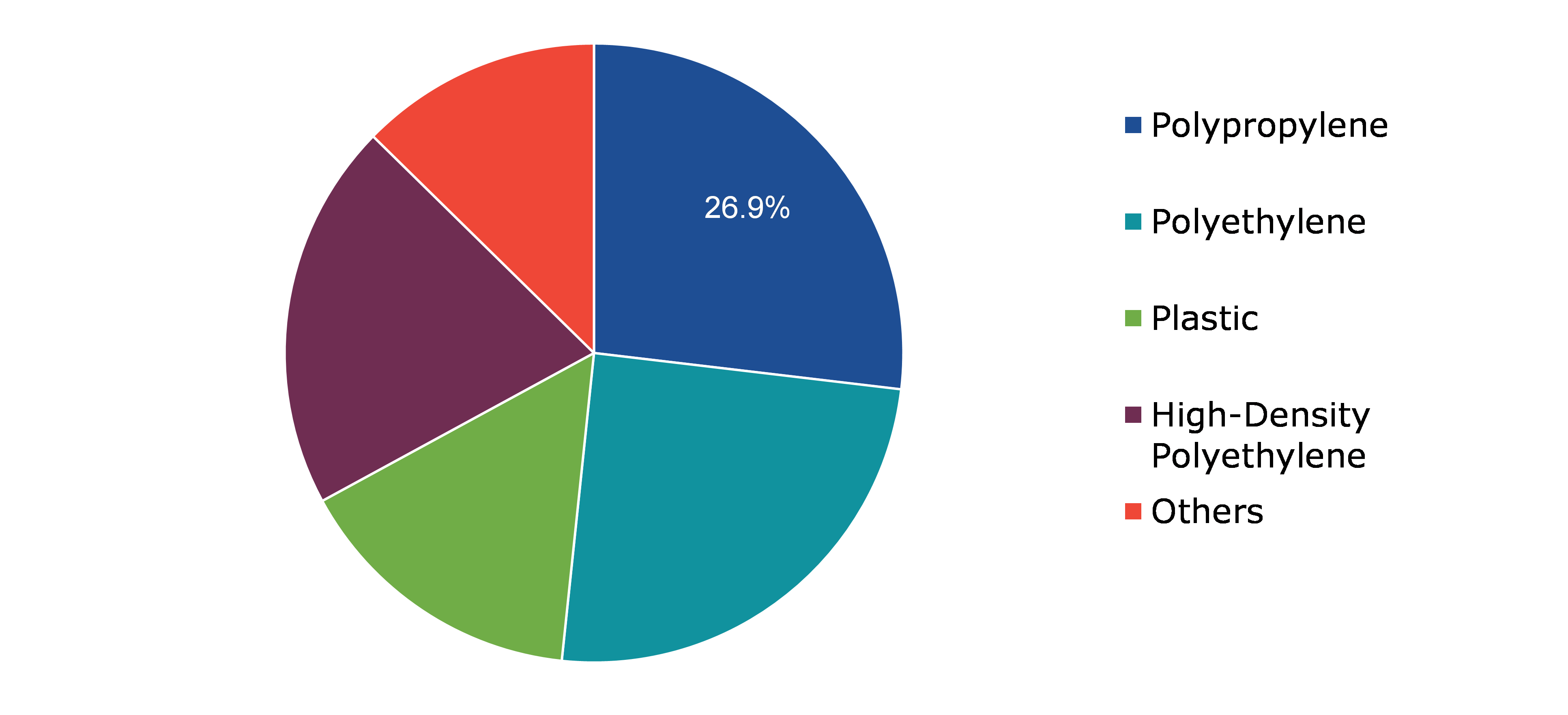

Based on material type, the global biohazard bags market has been divided into polypropylene, polyethylene, plastic, high-density polyethylene, and others. Among these, polypropylene sub-segment expected to account for highest revenue share whereas polyethylene is expected to be the fastest growing during the forecast period.

Source: Research Dive Analysis

The polypropylene sub-segment is expected to have highest market share during forecast period and generate a revenue of $175 million by 2030, growing from $106.6 million in 2021. Polypropylene is widely used plastic polymer for biohazard bags manufacturing as it offers excellent chemical impact resistance properties as well as it is leakage proof and can be heat sealed. Polypropylene is lightweight, durable, flexible, and recyclable material which makes these polymers perfect material for the biohazard bags. These factors are expected to majorly attribute to growth of the sub-segment.

The polyethylene sub-segment is expected to be fastest growing during forecast period and may generate a revenue of $176.6 million by 2030, growing from $98.3 million in 2021. Lightweight, functional synthetic polymer created from the polymerization of ethylene is called polyethylene (PE). Polyethylene (PE) ensures that the content is well-preserved because it is strong and resistant to outside effects. Polyethylene is incredibly flexible and adaptable. For a more personalized alternative, it also provides numerous thicknesses, clarities, and designer colors in addition to the protection. These factors are expected to majorly attribute to growth of the sub-segment.

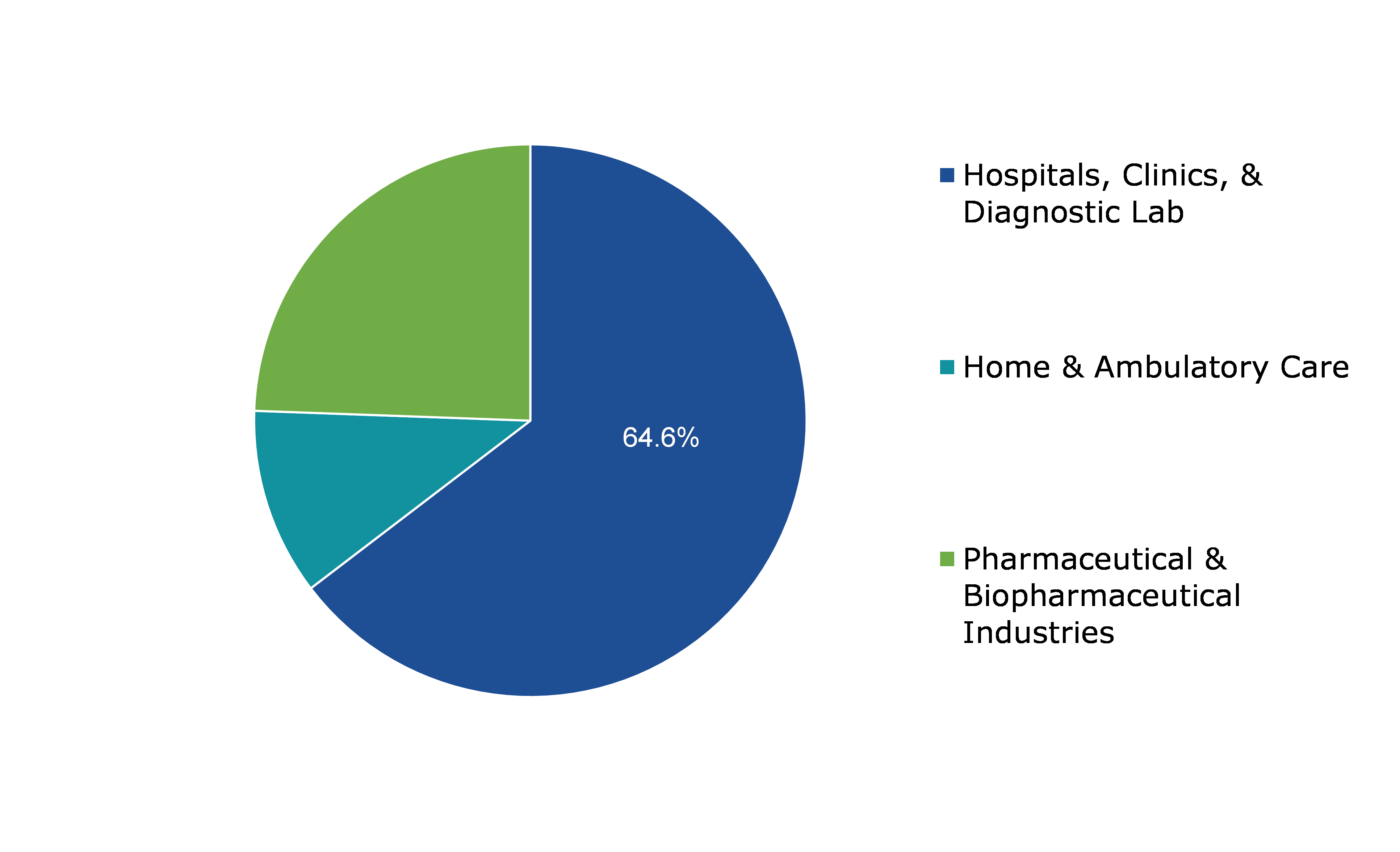

Based on end-use, the global biohazard bags market is further divided into hospitals, clinics & diagnostic labs, home & ambulatory care, and pharmaceutical & biopharmaceutical industries. Among these, hospitals, clinics & diagnostic labs sub-segment is expected to account for highest revenue share during the forecast period.

Source: Research Dive Analysis

The hospitals, clinics, & diagnostic lab sub-segment is expected to have highest market share and generate a revenue of $256.3 million by 2030, growing from $442.8 million in 2021.As per data from Word Health Organization (WHO), more than eight billion doses of vaccine have been administered worldwide which produced 144,000 tons of waste in the form of needles and syringes between March 2020 and November 2021. During the same time period, it is estimated that approximately 87,000 tons of waste from Personal Protective Equipment (PPE) was generated. Most of these types of waste are generated in hospitals. These factors are expected to increase demand for biohazard bags, which may result in the increased market share during analysis period.

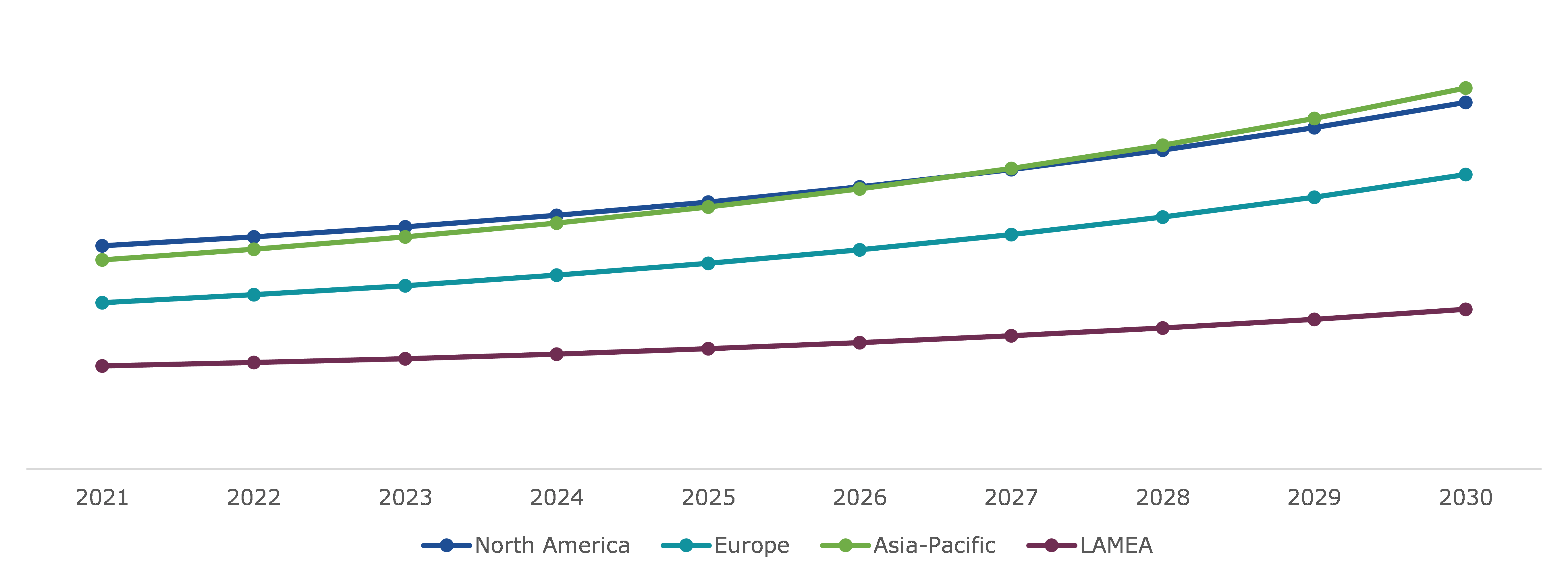

The global biohazard bags market was investigated across Europe, North America, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The biohazard bags market size in North America accounted $126.1 million in 2021 and it is projected grow with a CAGR of 5.89%. The market for biohazard bags in North America has experienced significant expansion, mostly due to important factors such need for properly disposing of medical waste and significant investments made by market participants. Increasing ageing population and growing patient population in these regions are few of all reasons that are predicted to fuel the biohazard bags market expansion in the North America region.

Source: Research Dive Analysis

Leading companies in biohazard bags market are Transcendia, Daniels Health, BioMedical Waste Solutions, LLC., International Plastics Inc., SP Bel-Art, Thermo Fisher Scientific, MiniGrip, Abdos Labtech Private Limited, VEOLIA, and Stericycle.

| Aspect | Particulars |

| | 2020-2021 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2030 |

| Geographical Scope | Europe, North America, Asia-Pacific, LAMEA |

| Segmentation by Capacity Type |

|

| Segmentation by Material Type |

|

| Segmentation by End-use |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global Biohazard Bags Market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on Biohazard Bags Market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Biohazard Bags Market Analysis, by Capacity Type

5.1.Overview

5.2.Less than 15 Gallon

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region,2021-2030

5.2.3.Market share analysis, by country,2021-2030

5.3.15 to 35 Gallon

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region,2021-2030

5.3.3.Market share analysis, by country,2021-2030

5.4.More than 35 Gallon

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region,2021-2030

5.4.3.Market share analysis, by country,2021-2030

5.5.Research Dive Exclusive Insights

5.5.1.Market attractiveness

5.5.2.Competition heatmap

6.Biohazard Bags Market Analysis, by Material Type

6.1.Overview

6.2.Polypropylene

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region,2021-2030

6.2.3.Market share analysis, by country,2021-2030

6.3.Polyethylene

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.2.Market size analysis, by region,2021-2030

6.3.3.Market share analysis, by country,2021-2030

6.4.Plastic

6.4.1.Definition, key trends, growth factors, and opportunities

6.4.2.Market size analysis, by region,2021-2030

6.4.3.Market share analysis, by country,2021-2030

6.5.High-density Polyethylene

6.5.1.Definition, key trends, growth factors, and opportunities

6.5.2.Market size analysis, by region,2021-2030

6.5.3.Market share analysis, by country,2021-2030

6.6.Information & Technology

6.6.1.Definition, key trends, growth factors, and opportunities

6.6.2.Market size analysis, by region,2021-2030

6.6.3.Market share analysis, by country,2021-2030

6.7.Others

6.7.1.Definition, key trends, growth factors, and opportunities

6.7.2.Market size analysis, by region,2021-2030

6.7.3.Market share analysis, by country,2021-2030

6.8.Research Dive Exclusive Insights

6.8.1.Market attractiveness

6.8.2.Competition heatmap

7.Biohazard Bags Market Analysis, by End-use

7.1.Overview

7.2.Hospitals

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region,2021-2030

7.2.3.Market share analysis, by country,2021-2030

7.3.Laboratories & Research Centers

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region,2021-2030

7.3.3.Market share analysis, by country,2021-2030

7.4.Pharmaceutical & Biotech Companies

7.4.1.Definition, key trends, growth factors, and opportunities

7.4.2.Market size analysis, by region,2021-2030

7.4.3.Market share analysis, by country,2021-2030

7.5.Chemical Industry

7.5.1.Definition, key trends, growth factors, and opportunities

7.5.2.Market size analysis, by region,2021-2030

7.5.3.Market share analysis, by country,2021-2030

7.6.Others

7.6.1.Definition, key trends, growth factors, and opportunities

7.6.2.Market size analysis, by region,2021-2030

7.6.3.Market share analysis, by country,2021-2030

7.7.Research Dive Exclusive Insights

7.7.1.Market attractiveness

7.7.2.Competition heatmap

8.Biohazard Bags Market, by Region

8.1.North America

8.1.1.U.S.

8.1.1.1.Market size analysis, by Capacity Type,2021-2030

8.1.1.2.Market size analysis, by Material Type,2021-2030

8.1.1.3.Market size analysis, by End-use,2021-2030

8.1.2.Canada

8.1.2.1.Market size analysis, by Capacity Type,2021-2030

8.1.2.2.Market size analysis, by Material Type,2021-2030

8.1.2.3.Market size analysis, by End-use,2021-2030

8.1.3.Mexico

8.1.3.1.Market size analysis, by Capacity Type,2021-2030

8.1.3.2.Market size analysis, by Material Type,2021-2030

8.1.3.3.Market size analysis, by End-use,2021-2030

8.1.4.Research Dive Exclusive Insights

8.1.4.1.Market attractiveness

8.1.4.2.Competition heatmap

8.2.Europe

8.2.1.Germany

8.2.1.1.Market size analysis, by Capacity Type,2021-2030

8.2.1.2.Market size analysis, by Material Type,2021-2030

8.2.1.3.Market size analysis, by End-use,2021-2030

8.2.2.U.K.

8.2.2.1.Market size analysis, by Capacity Type,2021-2030

8.2.2.2.Market size analysis, by Material Type,2021-2030

8.2.2.3.Market size analysis, by End-use,2021-2030

8.2.3.France

8.2.3.1.Market size analysis, by Capacity Type,2021-2030

8.2.3.2.Market size analysis, by Material Type,2021-2030

8.2.3.3.Market size analysis, by End-use,2021-2030

8.2.4.Spain

8.2.4.1.Market size analysis, by Capacity Type,2021-2030

8.2.4.2.Market size analysis, by Material Type,2021-2030

8.2.4.3.Market size analysis, by End-use,2021-2030

8.2.5.Italy

8.2.5.1.Market size analysis, by Capacity Type,2021-2030

8.2.5.2.Market size analysis, by Material Type,2021-2030

8.2.5.3.Market size analysis, by End-use,2021-2030

8.2.6.Rest of Europe

8.2.6.1.Market size analysis, by Capacity Type,2021-2030

8.2.6.2.Market size analysis, by Material Type,2021-2030

8.2.6.3.Market size analysis, by End-use,2021-2030

8.2.7.Research Dive Exclusive Insights

8.2.7.1.Market attractiveness

8.2.7.2.Competition heatmap

8.3.Asia-Pacific

8.3.1.China

8.3.1.1.Market size analysis, by Capacity Type,2021-2030

8.3.1.2.Market size analysis, by Material Type,2021-2030

8.3.1.3.Market size analysis, by End-use,2021-2030

8.3.2.Japan

8.3.2.1.Market size analysis, by Capacity Type,2021-2030

8.3.2.2.Market size analysis, by Material Type,2021-2030

8.3.2.3.Market size analysis, by End-use,2021-2030

8.3.3.India

8.3.3.1.Market size analysis, by Capacity Type,2021-2030

8.3.3.2.Market size analysis, by Material Type,2021-2030

8.3.3.3.Market size analysis, by End-use,2021-2030

8.3.4.Australia

8.3.4.1.Market size analysis, by Capacity Type,2021-2030

8.3.4.2.Market size analysis, by Material Type,2021-2030

8.3.4.3.Market size analysis, by End-use,2021-2030

8.3.5.South Korea

8.3.5.1.Market size analysis, by Capacity Type,2021-2030

8.3.5.2.Market size analysis, by Material Type,2021-2030

8.3.5.3.Market size analysis, by End-use,2021-2030

8.3.6.Rest of Asia Pacific

8.3.6.1.Market size analysis, by Capacity Type,2021-2030

8.3.6.2.Market size analysis, by Material Type,2021-2030

8.3.6.3.Market size analysis, by End-use,2021-2030

8.3.7.Research Dive Exclusive Insights

8.3.7.1.Market attractiveness

8.3.7.2.Competition heatmap

8.4.LAMEA

8.4.1.Brazil

8.4.1.1.Market size analysis, by Capacity Type,2021-2030

8.4.1.2.Market size analysis, by Material Type,2021-2030

8.4.1.3.Market size analysis, by End-use,2021-2030

8.4.2.Saudi Arabia

8.4.2.1.Market size analysis, by Capacity Type,2021-2030

8.4.2.2.Market size analysis, by Material Type,2021-2030

8.4.2.3.Market size analysis, by End-use,2021-2030

8.4.3.UAE

8.4.3.1.Market size analysis, by Capacity Type,2021-2030

8.4.3.2.Market size analysis, by Material Type,2021-2030

8.4.3.3.Market size analysis, by End-use,2021-2030

8.4.4.South Africa

8.4.4.1.Market size analysis, by Capacity Type,2021-2030

8.4.4.2.Market size analysis, by Material Type,2021-2030

8.4.4.3.Market size analysis, by End-use,2021-2030

8.4.5.Rest of LAMEA

8.4.5.1.Market size analysis, by Capacity Type,2021-2030

8.4.5.2.Market size analysis, by Material Type,2021-2030

8.4.5.3.Market size analysis, by End-use,2021-2030

8.4.6.Research Dive Exclusive Insights

8.4.6.1.Market attractiveness

8.4.6.2.Competition heatmap

9.Competitive Landscape

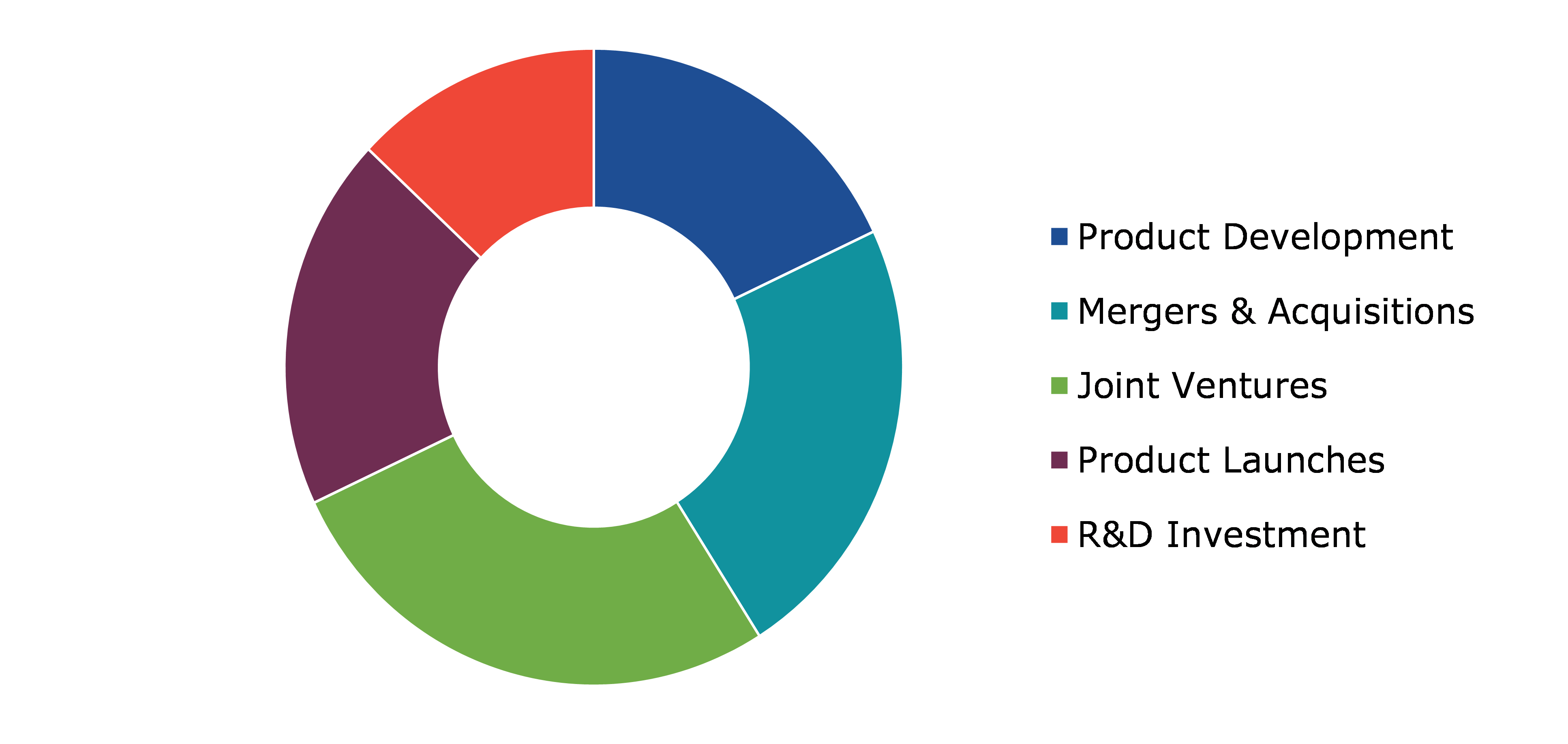

9.1.Top winning strategies, 2021

9.1.1.By strategy

9.1.2.By year

9.2.Strategic overview

9.3.Market share analysis, 2021

10.Company Profiles

10.1.Daniels Health

10.1.1.Overview

10.1.2.Business segments

10.1.3.Product portfolio

10.1.4.Financial performance

10.1.5.Recent developments

10.1.6.SWOT analysis

10.2.Stericycle

10.2.1.Overview

10.2.2.Business segments

10.2.3.Product portfolio

10.2.4.Financial performance

10.2.5.Recent developments

10.2.6.SWOT analysis

10.3.VEOLIA 10.3.1.Overview

10.3.2.Business segments

10.3.3.Product portfolio

10.3.4.Financial performance

10.3.5.Recent developments

10.3.6.SWOT analysis

10.4.Abdos Labtech Private Limited

10.4.1.Overview

10.4.2.Business segments

10.4.3.Product portfolio

10.4.4.Financial performance

10.4.5.Recent developments

10.4.6.SWOT analysis

10.5.MiniGrip

10.5.1.Overview

10.5.2.Business segments

10.5.3.Product portfolio

10.5.4.Financial performance

10.5.5.Recent developments

10.5.6.SWOT analysis

10.6.BioMedical Waste Solutions, LLC.

10.6.1.Overview

10.6.2.Business segments

10.6.3.Product portfolio

10.6.4.Financial performance

10.6.5.Recent developments

10.6.6.SWOT analysis

10.7.Transcendia

10.7.1.Overview

10.7.2.Business segments

10.7.3.Product portfolio

10.7.4.Financial performance

10.7.5.Recent developments

10.7.6.SWOT analysis

10.8.Thermo Fisher Scientific

10.8.1.Overview

10.8.2.Business segments

10.8.3.Product portfolio

10.8.4.Financial performance

10.8.5.Recent developments

10.8.6.SWOT analysis

10.9.SP Bel-Art

10.9.1.Overview

10.9.2.Business segments

10.9.3.Product portfolio

10.9.4.Financial performance

10.9.5.Recent developments

10.9.6.SWOT analysis

10.10.International Plastics Inc.

10.10.1.Overview

10.10.2.Business segments

10.10.3.Product portfolio

10.10.4.Financial performance

10.10.5.Recent developments

10.10.6.SWOT analysis

11.Appendix

11.1.Parent & peer market analysis

11.2.Premium insights from industry experts

11.3.Related reports

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}