Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

AU20113321 |

Pages: 245 |

Jun 2021 |

The global mining equipment market is anticipated to garner $170,718.3 million in the 2021–2028 timeframe, growing from $102,471.4 million in 2020 at a healthy CAGR of 6.5%.

Partnership, acquisitions, and product advancements by leading players in the market to increase the demand for mining equipment is estimated to drive the growth of the mining equipment market.

However, the strict government regulations as mining can lead to soil pollution, depletion of natural resources, and loss of biodiversity is estimated to restrain the market growth.

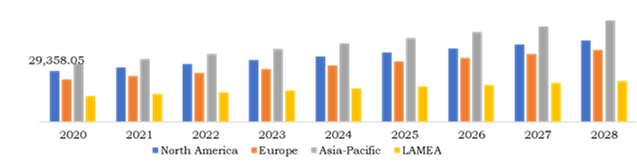

According to the regional analysis of the market, the Asia-Pacific mining equipment market is anticipated to grow at a CAGR of 7.1% by generating a revenue of $58,607.6 million during the review period.

The mining equipment comprises of various machines that help in performing different surface mining and underground mining activities with precision and efficiency. The different types of equipment used for mining are mining drills, blasting tools, earth movers, crushing equipment, screening equipment, feeding, conveying, and analysis equipment.

The COVID-19 outbreak has severely impacted various businesses and the mining equipment market also experienced a negative impact owing to cancellation or postponements of mining projects. Disruptions in the supply chain and unavailability of raw materials due to import-export and travel restrictions has led to drastic decline in the demand for mining equipment. In addition, the livelihoods of many workers became uncertain because of cancellation or postponements of mining projects due to which many workers returned to their hometowns. Due to travel restrictions, people had to face difficulties to commute from their hometowns to workplaces. Furthermore, many mining equipment companies are going through financial recession that has resulted in laying off a lot of their workforce, which had a negative impact on the market growth during the pandemic.

Various government and company initiatives such as measures to protect the employment & labor crime, securing the health of employees & prevent the spread of COVID-19 virus, as well as corporate solidarity funds to bring the global economy on track are helping the society to recover from the chaotic situation. For instance, BHP, the Australia-based mining company has introduced $50 million (AUD) Vital Resources Fund to support the local, regional health workers, and other community services. Many government initiatives to protect the employees’ rights such as obligations for the companies to pay insurance, pension, and health contributions during the pandemic has offered help to the workers. For instance, in Chile, the government has introduced Employment Protection Law in April 2020 to protect the family of people who have lost their jobs during the pandemic.

The rising demand for mineral fertilizers to improve the crop yields in order to feed the growing population is estimated to drive the demand for mining equipment market. The top three nutrients required to boost the crop yields are potassium, nitrogen, and phosphorous. Phosphorous used in mineral fertilizers is mined as phosphate rock. As stated on July 31, 2017, in Triple Pundit, the popular news website, U.S. is the third largest phosphorous consumer as well as producer in the world. Furthermore, the mineral fertilizers can be taken in by the plants instantly and no conversion is required. In addition, the nutritional scheme of mineral fertilizers can be composed based on a plant’s needs. All these benefits are estimated to drive the demand for mining equipment market during the analysis period.

To know more about global mining equipment market drivers, get in touch with our analysts here.

The purchase of new mining equipment is costly which depends on investments as well as economic condition of the countries. The developing countries such as South Africa, Peru, Argentina, and others opt for used mining equipment instead of purchasing new equipment. As the mining equipment have good durability and reliable lifecycle if maintained properly developed countries such as U.S., Germany, UK, France export the used mining equipment to the developing countries such as Middle East countries, South East Asian countries, and South America. This used mining equipment have lower price compared to the new equipment which is estimated to hinder the demand for new mining equipment during the forecast period.

The latest trends in mining technology and shift towards sustainability to ensure modern, safe, and productive mining techniques are estimated to generate huge growth opportunities during the forecast period. For instance, spatial data visualization that facilitates Three-dimensional (3D) modelling and creates viewable and depth perception that facilitates reimagining the mine is estimated to create enormous growth opportunities. In addition, the introduction of Virtual Reality (VR) technology that helps miners to experience the site that they are going to mine without actually being out in the field is anticipated to generate excellent growth opportunities. Furthermore, the Geographic Information Systems (GIS) help the miners in mineral exploration, report generation, geochemical and hydrology data, adhering to sustainability and regulatory compliance, and facility & tailings managements.

To know more about global mining equipment market opportunities, get in touch with our analysts here.

Source: Research Dive Analysis

The surface mining sub-type is anticipated to have a dominant market share and generate a revenue of $68,655.1 million by 2028, growing from $41,766.8 million in 2020. The surface mining is the most common mining type which is safer and has low operating cost. The surface mining operations are easy to control as we can increase or decrease the rate of production. Also, this type of mining requires less workforce. With surface mining, the geological information can be improved and grade control becomes easier. Hence, surface mining is cheaper and can recover more resources by using large-scale mining equipment that offer higher production rates.

The underground mining sub-type is anticipated to witness the fastest growth and generate a revenue of $60,697.9 million by 2028, growing from $34,570.0 million in 2020. The underground mining is suitable to mine minerals, coal that are located at depth below the earth’s surface. Hence, with deeper mineral or coal deposits it becomes difficult to remove them with the help of surface mining. The underground mining is largely used to mine the coal and precious metals such as gold and copper.

Source: Research Dive Analysis

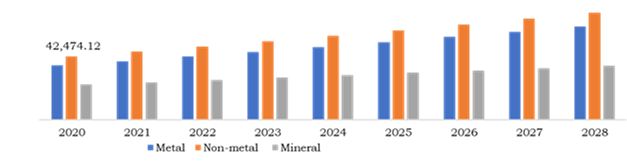

The non-metal sub-segment of the global mining equipment market is estimated to have a dominant market share and surpass $71,764.8 million by 2028, with an increase from $42,474.1 million in 2020. The non-metal mining extracts different minerals from earth’s surface such as stone, sand, rock, coal, sand, clay, and others. The non-metals obtained via mining are used in various applications such as preparation of cement, lime products, manufacturing of glass, ceramics, and other products. Furthermore, the non-metal mining is used in construction materials, sanitary ware, tableware, and decorative items which is anticipated to drive the growth of non-metals sub-segment of the mining equipment market during the forecast period.

The metal sub-segment of the global mining equipment market is anticipated to witness the fastest growth and surpass $62,658.6 million by 2028, with an increase from $36,420.3 million in 2020. This is majorly owing to the extraction of precious metals such as gold, silver, platinum and industrial metals such as copper, steel, aluminum. The precious metals have higher economic value whereas the industrial metals are used in industrial applications including manufacturing, construction, and technological industries. For instance, palladium is used in the electronic industry.

Source: Research Dive Analysis

The Asia-Pacific mining equipment market accounted $33,590.1 million in 2020 and is projected to register a revenue of $58,607.6 million by 2028. This is majorly owing to high demand for mineral reserves across the world. Asia-Pacific countries have some of the largest coal mine reserves in the world. For instance, as stated on October 7, 2019, in NS Energy, the international magazine, coal is widely used for power generation across various industries. Also, coal is used as a fuel in extraction of iron from iron ore and in manufacturing of cement. Some of the largest coal mines in the world are located in China. Haerwusu Coal Mine, located in China has more than 1.7 billion tons of coal reserves. In addition, Hei Dai Gou coal mine is also located in China that has more than 1.5 billion tons of coal reserves that has a capacity to produce 30 million tons of coal every year. In addition, Peak Downs coal mine located in Australia has coal reserves of 1,063 million tons. Another largest coal mine is located in New South Wales, Australia named as Mt Arthur coal mine that has coal reserves of 1,049 million tons. Furthermore, as stated on November 27, 2020 in the NS Energy, the international magazine, Australia is one of the top countries in the world that has largest gold mine reserves in the world. The gold mine reserves of this country are 10,000 tons. The BHP is largest mining company with its headquarters in Melbourne, Australia. All these factors are estimated to drive the demand for mining equipment in the Asia-Pacific region during the forecast period.

Source: Research Dive Analysis

Some of the leading mining equipment market players are Caterpillar Inc., Komatsu Ltd., Volvo Group, Terex Corporation, Sandvik AB, Deere & Company, Liebherr, Hitachi, Ltd., Epiroc AB, and Doosan Corporation.

Porter’s Five Forces Analysis for the Global Mining Equipment Market:

| Aspect | Particulars |

| Historical Market Estimations | 2019-2020 |

| Base Year for Market Estimation | 2020 |

| Forecast Timeline for Market Projection | 2021-2028 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Mining Type |

|

| Segmentation by End Use |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.4.1.Assumptions

1.4.2.Forecast parameters

1.5.Data sources

1.5.1.Primary

1.5.2.Secondary

2.Executive Summary

2.1.360° summary

2.2.Mining Type trends

2.3.End Use trends

3.Market overview

3.1.Market segmentation & definitions

3.2.Key takeaways

3.2.1.Top investment pockets

3.2.2.Top winning strategies

3.3.Porter’s five forces analysis

3.3.1.Bargaining power of consumers

3.3.2.Bargaining power of suppliers

3.3.3.Threat of new entrants

3.3.4.Threat of substitutes

3.3.5.Competitive rivalry in the market

3.4.Market dynamics

3.4.1.Drivers

3.4.2.Restraints

3.4.3.Opportunities

3.5.End Use landscape

3.6.Regulatory landscape

3.7.Patent landscape

3.8.Market value chain analysis

3.9.Strategic overview

4.Mining Equipment Market, by Mining Type

4.1.Surface

4.1.1.Market size and forecast, by region, 2020-2028

4.1.2.Comparative market share analysis, 2020 & 2028

4.2.Underground

4.2.1.Market size and forecast, by region, 2020-2028

4.2.2.Comparative market share analysis, 2020 & 2028

4.3.Others

4.3.1.Market size and forecast, by region, 2020-2028

4.3.2.Comparative market share analysis, 2020 & 2028

5.Mining Equipment Market, by End Use

5.1.Metal

5.1.1.Market size and forecast, by region, 2020-2028

5.1.2.Comparative market share analysis, 2020 & 2028

5.2.Non-metal

5.2.1.Market size and forecast, by region, 2020-2028

5.2.2.Comparative market share analysis, 2020 & 2028

5.3.Mineral

5.3.1.Market size and forecast, by region, 2020-2028

5.3.2.Comparative market share analysis, 2020 & 2028

6.Mining Equipment Market, by Region

6.1.North America

6.1.1.Market size and forecast, by Mining Type, 2020-2028

6.1.2.Market size and forecast, by End Use, 2020-2028

6.1.3.Market size and forecast, by country, 2020-2028

6.1.4.Comparative market share analysis, 2020 & 2028

6.1.5.U.S.

6.1.5.1.Market size and forecast, by Mining Type, 2020-2028

6.1.5.2.Market size and forecast, by End Use, 2020-2028

6.1.5.3.Comparative market share analysis, 2020 & 2028

6.1.6.Canada

6.1.6.1.Market size and forecast, by Mining Type, 2020-2028

6.1.6.2.Market size and forecast, by End Use, 2020-2028

6.1.6.3.Comparative market share analysis, 2020 & 2028

6.1.7.Mexico

6.1.7.1.Market size and forecast, by Mining Type, 2020-2028

6.1.7.2.Market size and forecast, by End Use, 2020-2028

6.1.7.3.Comparative market share analysis, 2020 & 2028

6.2.Europe

6.2.1.Market size and forecast, by Mining Type, 2020-2028

6.2.2.Market size and forecast, by End Use, 2020-2028

6.2.3.Market size and forecast, by country, 2020-2028

6.2.4.Comparative market share analysis, 2020 & 2028

6.2.5.Germany

6.2.5.1.Market size and forecast, by Mining Type, 2020-2028

6.2.5.2.Market size and forecast, by End Use, 2020-2028

6.2.5.3.Comparative market share analysis, 2020 & 2028

6.2.6.UK

6.2.6.1.Market size and forecast, by Mining Type, 2020-2028

6.2.6.2.Market size and forecast, by End Use, 2020-2028

6.2.6.3.Comparative market share analysis, 2020 & 2028

6.2.7.France

6.2.7.1.Market size and forecast, by Mining Type, 2020-2028

6.2.7.2.Market size and forecast, by End Use, 2020-2028

6.2.7.3.Comparative market share analysis, 2020 & 2028

6.2.8.Russia

6.2.8.1.Market size and forecast, by Mining Type, 2020-2028

6.2.8.2.Market size and forecast, by End Use, 2020-2028

6.2.8.3.Comparative market share analysis, 2020 & 2028

6.2.9.Italy

6.2.9.1.Market size and forecast, by Mining Type, 2020-2028

6.2.9.2.Market size and forecast, by End Use, 2020-2028

6.2.9.3.Comparative market share analysis, 2020 & 2028

6.2.10.Rest of Europe

6.2.10.1.Market size and forecast, by Mining Type, 2020-2028

6.2.10.2.Market size and forecast, by End Use, 2020-2028

6.2.10.3.Comparative market share analysis, 2020 & 2028

6.3.Asia Pacific

6.3.1.Market size and forecast, by Mining Type, 2020-2028

6.3.2.Market size and forecast, by End Use, 2020-2028

6.3.3.Market size and forecast, by country, 2020-2028

6.3.4.Comparative market share analysis, 2020 & 2028

6.3.5.China

6.3.5.1.Market size and forecast, by Mining Type, 2020-2028

6.3.5.2.Market size and forecast, by End Use, 2020-2028

6.3.5.3.Comparative market share analysis, 2020 & 2028

6.3.6.Japan

6.3.6.1.Market size and forecast, by Mining Type, 2020-2028

6.3.6.2.Market size and forecast, by End Use, 2020-2028

6.3.6.3.Comparative market share analysis, 2020 & 2028

6.3.7.India

6.3.7.1.Market size and forecast, by Mining Type, 2020-2028

6.3.7.2.Market size and forecast, by End Use, 2020-2028

6.3.7.3.Comparative market share analysis, 2020 & 2028

6.3.8.Australia

6.3.8.1.Market size and forecast, by Mining Type, 2020-2028

6.3.8.2.Market size and forecast, by End Use, 2020-2028

6.3.8.3.Comparative market share analysis, 2020 & 2028

6.3.9.South Korea

6.3.9.1.Market size and forecast, by Mining Type, 2020-2028

6.3.9.2.Market size and forecast, by End Use, 2020-2028

6.3.9.3.Comparative market share analysis, 2020 & 2028

6.3.10.Rest of Asia-Pacific

6.3.10.1.Market size and forecast, by Mining Type, 2020-2028

6.3.10.2.Market size and forecast, by End Use, 2020-2028

6.3.10.3.Comparative market share analysis, 2020 & 2028

6.4.LAMEA

6.4.1.Market size and forecast, by Mining Type, 2020-2028

6.4.2.Market size and forecast, by End Use, 2020-2028

6.4.3.Market size and forecast, by country, 2020-2028

6.4.4.Comparative market share analysis, 2020 & 2028

6.4.5.Latin America

6.4.5.1.Market size and forecast, by Mining Type, 2020-2028

6.4.5.2.Market size and forecast, by End Use, 2020-2028

6.4.5.3.Comparative market share analysis, 2020 & 2028

6.4.6.Middle East

6.4.6.1.Market size and forecast, by Mining Type, 2020-2028

6.4.6.2.Market size and forecast, by End Use, 2020-2028

6.4.6.3.Comparative market share analysis, 2020 & 2028

6.4.7.Africa

6.4.7.1.Market size and forecast, by Mining Type, 2020-2028

6.4.7.2.Market size and forecast, by End Use, 2020-2028

6.4.7.3.Comparative market share analysis, 2020 & 2028

7.Company profiles

7.1.Caterpillar Inc.

7.1.1.Business overview

7.1.2.Financial performance

7.1.3.Product portfolio

7.1.4.Recent strategic moves & developments

7.1.5.SWOT analysis

7.2.Komatsu Ltd.

7.2.1.Business overview

7.2.2.Financial performance

7.2.3.Product portfolio

7.2.4.Recent strategic moves & developments

7.2.5.SWOT analysis

7.3.Volvo Group

7.3.1.Business overview

7.3.2.Financial performance

7.3.3.Product portfolio

7.3.4.Recent strategic moves & developments

7.3.5.SWOT analysis

7.4.Terex Corporation

7.4.1.Business overview

7.4.2.Financial performance

7.4.3.Product portfolio

7.4.4.Recent strategic moves & developments

7.4.5.SWOT analysis

7.5.Sandvik AB

7.5.1.Business overview

7.5.2.Financial performance

7.5.3.Product portfolio

7.5.4.Recent strategic moves & developments

7.5.5.SWOT analysis

7.6.Deere & Company

7.6.1.Business overview

7.6.2.Financial performance

7.6.3.Product portfolio

7.6.4.Recent strategic moves & developments

7.6.5.SWOT analysis

7.7.Liebherr

7.7.1.Business overview

7.7.2.Financial performance

7.7.3.Product portfolio

7.7.4.Recent strategic moves & developments

7.7.5.SWOT analysis

7.8.Hitachi, Ltd.

7.8.1.Business overview

7.8.2.Financial performance

7.8.3.Product portfolio

7.8.4.Recent strategic moves & developments

7.8.5.SWOT analysis

7.9.Epiroc AB

7.9.1.Business overview

7.9.2.Financial performance

7.9.3.Product portfolio

7.9.4.Recent strategic moves & developments

7.9.5.SWOT analysis

7.10.Doosan Corporation

7.10.1.Business overview

7.10.2.Financial performance

7.10.3.Product portfolio

7.10.4.Recent strategic moves & developments

7.10.5.SWOT analysis

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}