Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

LI20101945 |

Pages: 270 |

Apr 2023 |

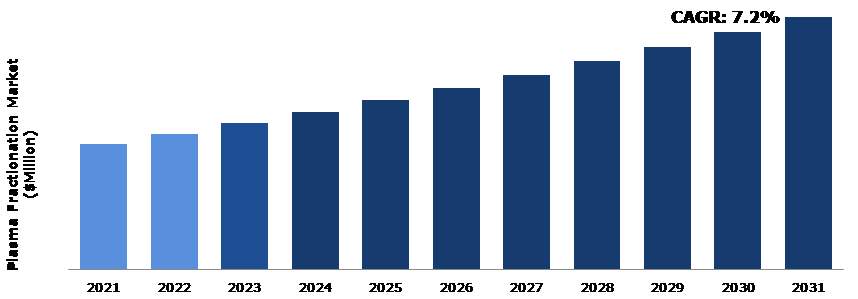

Modern plasma fractionation combines manufacturing steps to isolate the fractions of blood plasma, in a sequential and integrated manner, the crude fractions that are further purified into individual therapeutic products. Growth in population of elderly people around the globe, who are more susceptible to rare disorders that necessitate the use of blood derivatives, is a major driver of the market's expansion. Furthermore, increase in use of immunoglobulins and alpha-1-antitrypsin in various fields of medicine globally is expected to drive the market growth. Another key factor driving the growth of this market is increase in blood collection facilities around the globe.

However, the potential emergence of new pathogenic agents that can withstand current viral inactivation treatments, as well as the potential effect of given purification technologies on the development of immunogenic properties in proteins, are the current major problems in plasma fractionation. In addition, the high cost of plasma therapy prevents the market from expanding. Furthermore, increase in use of recombinant alternatives for the treatment of autoimmune diseases, such as fibrinogen concentration and protease inhibitor, hampers the growth of the plasma fractionation market.

Furthermore, lifestyle such as consumption of alcohol & tobacco and fast food are increasing the risk of inflammatory disorders in the people, which further increases the opportunities for the plasma fractionation market growth. Moreover, various activities by key market players, such as product launches, partnerships, mergers, and acquisitions, to introduce technologically advanced plasma fractionation techniques and products into the market, are expected to drive the market growth. For instance, in January 2022, Octapharma received approval to expand the indications for cutaquig in the European Union (EU). Cutaquig is a human immunoglobulin that is administered subcutaneously. It gives many patients the acquired immune deficiencies flexible treatment options.

According to regional analysis, the Asia-Pacific plasma fractionation market size is anticipated to show the fastest growth by 2031. The presence of governmental bodies that regulate & supervise plasma collection, fractionation, and sales is a significant factor driving the market growth.

Plasma is the most important liquid component of blood, containing high concentration of various proteins. Human plasma contains different proteins; however, only a few of these proteins are useful in the production of therapeutic plasma products. It is mostly water, with trace amounts of minerals, salts, ions, nutrients, and proteins in solution.

Plasma fractionation is the classification of the various components of blood plasma, which is a component of blood collected through blood fractionation. After plasma fractionation, wide range of life-saving products such as immunoglobulins, protease inhibitors, anticoagulants, albumins, and coagulation factors are obtained for preventing, managing, and treating various life-threatening human injuries & illnesses.

The COVID-19 pandemic has impacted every industry on the planet. For instance, after the WHO declared COVID-19 a pandemic, countries around the globe implemented nationwide lockdowns to practice social distancing as a preventative measure. This caused disruption, limitation, challenges, and changes in every industry sector. Similarly, the pandemic had an impact on the plasma fractionation industry. For instance, the COVID-19 pandemic has reduced the number of blood donations and plasma collections, stifling market growth. However, decrease in raw material supply was offset by a drop in demand for plasma derivatives when nationwide lockdowns began, as elective surgical procedures were postponed and treatment for other medical conditions was additionally hampered. Furthermore, while overall plasma supply in countries was maintained, some areas faced shortages. As a result, the viral outbreak harmed the plasma fractionation market.

However, due to the disruption in the plasma collection process, the market grew slowly. Despite being referred to as ‘essential infrastructure’, plasma collection has been hampered by increase in the number of COVID-19 cases as well as its guidelines such as social distancing & stay-at-home orders. According to CSL Limited's annual report for the fiscal year 2020/2021, COVID-19 impact on plasma fractionation market reduced plasma collection volume while increasing collection costs in terms of donor compensation.

Immunoglobulin is an antibody that is found in immune system cells. It is used to treat conditions such as immunodeficiency diseases, idiopathic thrombocytosis purpura (ITP), Kawasaki disease, and nervous system disorders. Immunoglobulins are further used to treat lupus and vasculitis, both of which are rare diseases. Immunoglobulins, such as IVIG, are used to treat blood diseases such as hemophilia for which no other treatment is available.

Moreover, immunoglobulins are commonly prescribed for people with myasthenia gravis, Guillen-Barre syndrome, multiple myeloma, acquired factor VIII inhibitors syndrome, autoimmune neutropenia, post-transfusion purpose, and polymyositis/dermatomyositis. In addition, they can be used to treat primary & secondary immunodeficiencies. As a result, growth in awareness and widespread adoption of immunoglobulins in medicine drive the plasm fractionation market growth.

To know more about global plasma fractionation market drivers, get in touch with our analysts here.

Many recombinant alternatives for various plasma-driven therapies have been developed in 2020. Recombinase products are used for prophylaxis and are less immunogenic than plasma-derived products, and have significant advantages, such as less frequent administration and greater efficacy in prophylactic use. Growth in use of recombinant factor and its increased use in prophylactic therapies are thus the major factors limiting the adoption of plasma products. In addition, increase in use of recombinant alternatives for the treatment of autoimmune diseases, such as fibrinogen concentration and protease inhibitor, has hampered the growth of the plasma fractionation market. Furthermore, the plasma fractionation market demand is hampered by restrictive medical reimbursement policies.

Increase in government funding and company investments in plasma therapy R&D activities are expected to increase plasma fractionation market share. The COVID-19 pandemic has created numerous opportunities for biotech & biopharma companies to invest in plasma therapy R&D. Many companies started working together to determine the efficacy of plasma therapy on COVID-19 patients. Grifols, a biopharma company specializing in plasma-derived products, for instance, collaborated with the Food and Drug Administration (FDA) and the Biomedical Advanced Research Development Authority (BARDA) in March 2020 to develop plasma therapeutics for COVID-19.

Furthermore, growth in number of plasma collection centers around the globe is a significant factor in the market's growth. For instance, Bio Products Laboratory Ltd (BPL), a leading manufacturer of plasma-derived protein therapies, will open its 29th plasma donation center in April 2022. Furthermore, Freedom Plasma will open its fourth plasma donation center in Ohio, U.S., in October 2022. As a result, the establishment of new plasma centers around the globe is expected to boost production of plasma-based products, thereby boosting market plasma fractionation market opportunity.

To know more about global plasma fractionation market opportunities, get in touch with our analysts here.

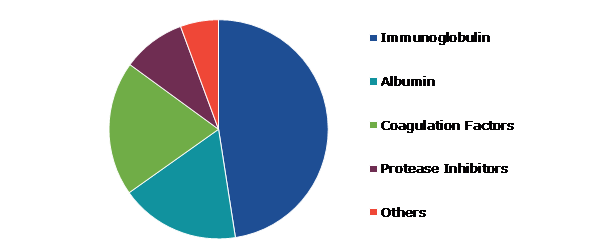

Based on product, the market has been divided into immunoglobulin, albumin, coagulation factors, protease inhibitors, and others. Among these, the immunoglobulin subsegment accounted for the highest market share in 2021 whereas the coagulation subsegment is estimated to show the fastest growth during the forecast period.

Source: Research Dive Analysis

The immunoglobulin subsegment accounted for a highest plasma fractionation market share in 2021 and is anticipated to show the fastest growth by 2031. Rise in geriatric population coupled with an increase in the prevalence of rare diseases, surge in number of plasma collection centers, expansion in use of immunoglobulins in various therapeutic areas, and various initiatives by key market players are predicted to drive the market during the forecast period. Various applications of immunoglobulin in conditions such as primary and secondary immunological deficiencies, autoimmune diseases, and inflammatory diseases are responsible for the growth of this segment. Another element that drives the expansion of the segment is the global uptick in immunology-related research.

The coagulation factors subsegment accounted for a second highest plasma fractionation market share in 2021. The market for coagulation factors is expanding as a result of factors such as new medication approval, high prevalence of bleeding diseases, and growth in initiatives & donations for people with severe bleeding disorders such as hemophilia. For instance, in April 2019, Grifols International SA, a supplier of plasma-derived therapeutics, provided blood clotting factor medications (100 million international units) for the treatment of hemophilic patients as part of a long-term initiative to support people with hemophilia.

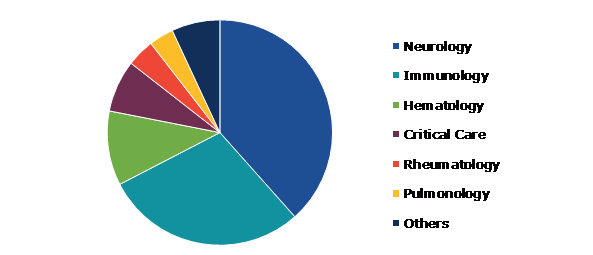

Depending on application, the market has been divided into neurology, immunology, hematology, critical care, rheumatology, pulmonology, and others. Among these, the neurology subsegment accounted for the highest revenue share in 2021.

Source: Research Dive Analysis

The neurology subsegment accounted for the highest plasma fractionation market share in 2021. The global increase in prevalence of neurological disorders is a significant driver of the market growth. For instance, the Centers for Disease Control and Prevention estimates that over 795,000 Americans have a stroke each year. Furthermore, growth in elderly population increases the likelihood of neurovascular illnesses such as stroke. In addition, the risk of having a stroke double after the age of 55, which encourages the use of plasma-based products for treatment and promotes market expansion.

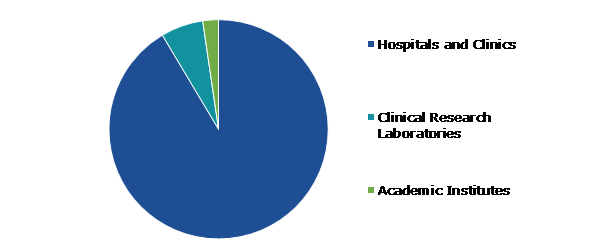

Based on end user, the market has been divided into hospitals & clinics, clinical research laboratories, and academic institutes. Among these, the hospitals & clinics subsegment accounted for the highest revenue share in 2021.

Source: Research Dive Analysis

The hospitals & clinics subsegment accounted for the highest market share in 2021. This is owing to rise in off-label use of plasma fractionation products in hospitals to treat a number of ailments, improved infrastructure, and healthcare services provided by hospitals. Furthermore, there is high demand for plasma fractionation products due to the complicated illnesses that can be addressed in contemporary clinical settings. Moreover, rise in surgical operations and utilization of plasma-derived products both contribute to the market's expansion. According to the NCBI, between January 1, 2019, and January 30, 2021, 13 million surgical procedures were performed in the U.S. These elements are expected to support the market expansion.

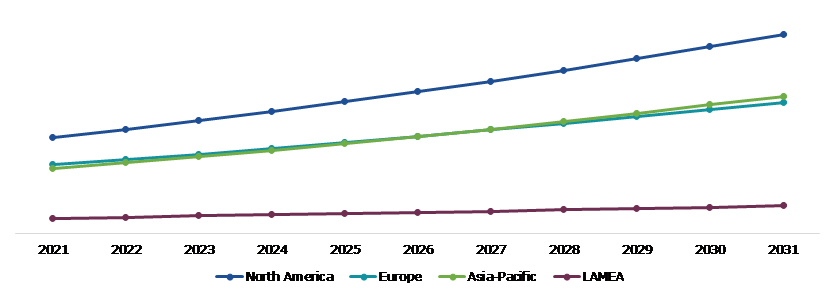

The plasma fractionation market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The North America plasma fractionation market analysis accounted for the highest market share in 2021. Due to the presence of prominent market players, expansion in plasma fractionation-related R&D activities, and growth in geriatric population, the North America is anticipated to account for a sizeable portion of the global plasma fractionation market. Rise in prevalence of various genetic diseases, growth of geriatric population, and rise in healthcare expenditure are all significant factors driving growth in the region. According to the Alzheimer's Association's March 2021 report, approximately 6.2 million people aged 65 and up in the U.S. have Alzheimer's-related dementia. This figure is expected to rise to 13.8 million by 2060. Thus, the high prevalence of Alzheimer's disease and the efficacy of the plasma fractionation product in treatment drive the regional market growth during the forecast period.

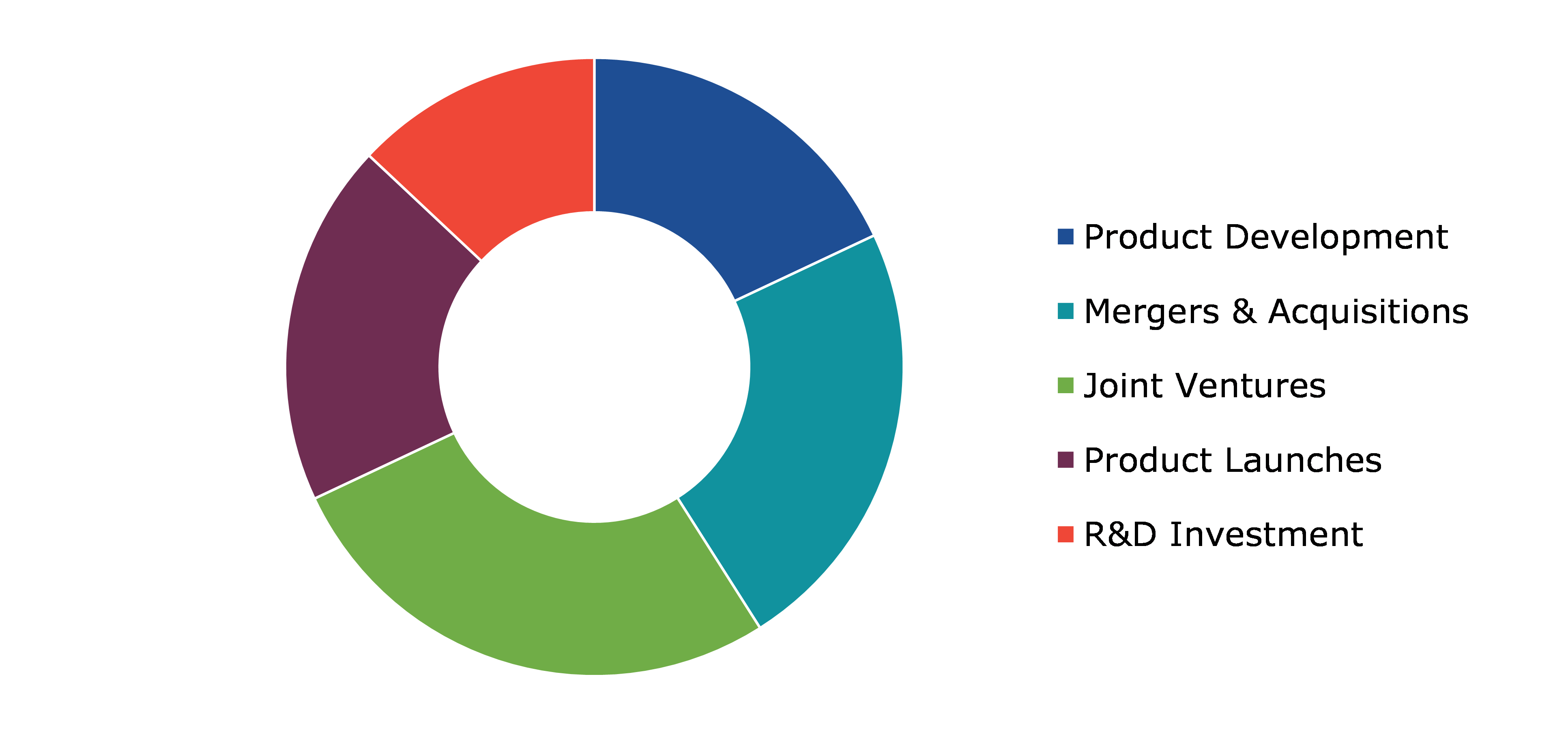

Investment and agreement are common strategies followed by major market players. For instance, in September 2022, the Ministry of Health, Labour and Welfare of Japan granted CSL Behring K.K. manufacturing and marketing approval for Berinert S.C. Injection 2000, a lyophilized human C1-esterase inhibitor concentrate for subcutaneous (SC) injection in plasma derivative, for the prevention of acute hereditary angioedema (HAE) attack.

Source: Research Dive Analysis

Some of the leading plasma fractionation market players are Kedrion S.P.A, Octapharma AG, Japan Blood Products Organization, Biotest AG, CSL Behring, Grifols, S.A., China Biologic Products Holdings, Inc., Takeda Pharmaceutical Company Limited, Bio Products Laboratory Ltd., and LFB Group.

| Aspect | Particulars |

| Historical Market Estimations | 2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Product |

|

| Segmentation by Application |

|

| Segmentation by End User |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global plasma fractionation market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on plasma fractionation market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Plasma Fractionation market Analysis, by Product

5.1.Overview

5.2.Immunoglobulin

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region,2021-2031

5.2.3.Market share analysis, by country,2021-2031

5.3.Albumin

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region,2021-2031

5.3.3.Market share analysis, by country,2021-2031

5.4.Coagulation Factors

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region,2021-2031

5.4.3.Market share analysis, by country,2021-2031

5.5.Protease Inhibitors

5.5.1.Definition, key trends, growth factors, and opportunities

5.5.2.Market size analysis, by region,2021-2031

5.5.3.Market share analysis, by country,2021-2031

5.6.Others

5.6.1.Definition, key trends, growth factors, and opportunities

5.6.2.Market size analysis, by region,2021-2031

5.6.3.Market share analysis, by country,2021-2031

5.7.Research Dive Exclusive Insights

5.7.1.Market attractiveness

5.7.2.Competition heatmap

6.Plasma Fractionation market Analysis, by Application

6.1.Overview

6.2.Neurology

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region,2021-2031

6.2.3.Market share analysis, by country,2021-2031

6.3.Immunology

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.2.Market size analysis, by region,2021-2031

6.3.3.Market share analysis, by country,2021-2031

6.4.Hematology

6.4.1.Definition, key trends, growth factors, and opportunities

6.4.2.Market size analysis, by region,2021-2031

6.4.3.Market share analysis, by country,2021-2031

6.5.Critical care

6.5.1.Definition, key trends, growth factors, and opportunities

6.5.2.Market size analysis, by region,2021-2031

6.5.3.Market share analysis, by country,2021-2031

6.6.Rheumatology

6.6.1.Definition, key trends, growth factors, and opportunities

6.6.2.Market size analysis, by region,2021-2031

6.6.3.Market share analysis, by country,2021-2031

6.7.Pulmonology

6.7.1.Definition, key trends, growth factors, and opportunities

6.7.2.Market size analysis, by region,2021-2031

6.7.3.Market share analysis, by country,2021-2031

6.8.Others

6.8.1.Definition, key trends, growth factors, and opportunities

6.8.2.Market size analysis, by region,2021-2031

6.8.3.Market share analysis, by country,2021-2031

6.9.Research Dive Exclusive Insights

6.9.1.Market attractiveness

6.9.2.Competition heatmap

7.Plasma Fractionation Market Analysis, by End-user

7.1.Hospitals and Clinics

7.1.1.Definition, key trends, growth factors, and opportunities

7.1.2.Market size analysis, by region,2021-2031

7.1.3.Market share analysis, by country,2021-2031

7.2.Clinical Research Laboratories

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region,2021-2031

7.2.3.Market share analysis, by country,2021-2031

7.3.Academic Institutes

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region,2021-2031

7.3.3.Market share analysis, by country,2021-2031

7.4.Research Dive Exclusive Insights

7.4.1.Market attractiveness

7.4.2.Competition heatmap

8.Plasma Fractionation Market, by region

8.1.North America

8.1.1.U.S.

8.1.1.1.Market size analysis, by Product, 2021-2031

8.1.1.2.Market size analysis, by Application, 2021-2031

8.1.1.3.Market size analysis, by End-user, 2021-2031

8.1.2.Canada

8.1.2.1.Market size analysis, by Product, 2021-2031

8.1.2.2.Market size analysis, by Application, 2021-2031

8.1.2.3.Market size analysis, by End-user, 2021-2031

8.1.3.Mexico

8.1.3.1.Market size analysis, by Product, 2021-2031

8.1.3.2.Market size analysis, by Application, 2021-2031

8.1.3.3.Market size analysis, by End-user, 2021-2031

8.1.4.Research Dive Exclusive Insights

8.1.4.1.Market attractiveness

8.1.4.2.Competition heatmap

8.2.Europe

8.2.1.Germany

8.2.1.1.Market size analysis, by Product, 2021-2031

8.2.1.2.Market size analysis, by Application, 2021-2031

8.2.1.3.Market size analysis, by End-user, 2021-2031

8.2.2.UK

8.2.2.1.Market size analysis, by Product, 2021-2031

8.2.2.2.Market size analysis, by Application, 2021-2031

8.2.2.3.Market size analysis, by End-user, 2021-2031

8.2.3.France

8.2.3.1.Market size analysis, by Product, 2021-2031

8.2.3.2.Market size analysis, by Application, 2021-2031

8.2.3.3.Market size analysis, by End-user, 2021-2031

8.2.4.Spain

8.2.4.1.Market size analysis, by Product, 2021-2031

8.2.4.2.Market size analysis, by Application, 2021-2031

8.2.4.3.Market size analysis, by End-user, 2021-2031

8.2.5.Italy

8.2.5.1.Market size analysis, by Product, 2021-2031

8.2.5.2.Market size analysis, by Application, 2021-2031

8.2.5.3.Market size analysis, by End-user, 2021-2031

8.2.6.Rest of Europe

8.2.6.1.Market size analysis, by Product, 2021-2031

8.2.6.2.Market size analysis, by Application, 2021-2031

8.2.6.3.Market size analysis, by End-user, 2021-2031

8.2.7.Research Dive Exclusive Insights

8.2.7.1.Market attractiveness

8.2.7.2.Competition heatmap

8.3.Asia Pacific

8.3.1.China

8.3.1.1.Market size analysis, by Product, 2021-2031

8.3.1.2.Market size analysis, by Application, 2021-2031

8.3.1.3.Market size analysis, by End-user, 2021-2031

8.3.2.Japan

8.3.2.1.Market size analysis, by Product, 2021-2031

8.3.2.2.Market size analysis, by Application, 2021-2031

8.3.2.3.Market size analysis, by End-user, 2021-2031

8.3.3.India

8.3.3.1.Market size analysis, by Product, 2021-2031

8.3.3.2.Market size analysis, by Application, 2021-2031

8.3.3.3.Market size analysis, by End-user, 2021-2031

8.3.4.Australia

8.3.4.1.Market size analysis, by Product, 2021-2031

8.3.4.2.Market size analysis, by Application, 2021-2031

8.3.4.3.Market size analysis, by End-user, 2021-2031

8.3.5.South Korea

8.3.5.1.Market size analysis, by Product, 2021-2031

8.3.5.2.Market size analysis, by Application, 2021-2031

8.3.5.3.Market size analysis, by End-user, 2021-2031

8.3.6.Rest of Asia Pacific

8.3.6.1.Market size analysis, by product, 2021-2031

8.3.6.2.Market size analysis, by Application, 2021-2031

8.3.6.3.Market size analysis, by End-user, 2021-2031

8.3.7.Research Dive Exclusive Insights

8.3.7.1.Market attractiveness

8.3.7.2.Competition heatmap

8.4.LAMEA

8.4.1.Brazil

8.4.1.1.Market size analysis, by product, 2021-2031

8.4.1.2.Market size analysis, by Application, 2021-2031

8.4.1.3.Market size analysis, by End-user, 2021-2031

8.4.2.Saudi Arabia

8.4.2.1.Market size analysis, by Product, 2021-2031

8.4.2.2.Market size analysis, by Application, 2021-2031

8.4.2.3.Market size analysis, by End-user, 2021-2031

8.4.3.UAE

8.4.3.1.Market size analysis, by Product, 2021-2031

8.4.3.2.Market size analysis, by Application, 2021-2031

8.4.3.3.Market size analysis, by End-user, 2021-2031

8.4.4.South Africa

8.4.4.1.Market size analysis, by Product, 2021-2031

8.4.4.2.Market size analysis, by Application, 2021-2031

8.4.4.3.Market size analysis, by End-user, 2021-2031

8.4.5.Rest of LAMEA

8.4.5.1.Market size analysis, by Product, 2021-2031

8.4.5.2.Market size analysis, by Application, 2021-2031

8.4.5.3.Market size analysis, by End-user, 2021-2031

8.4.6.Research Dive Exclusive Insights

8.4.6.1.Market attractiveness

8.4.6.2.Competition heatmap

9.Competitive Landscape

9.1.Top winning strategies, 2021

9.1.1.By strategy

9.1.2.By year

9.2.Strategic overview

9.3.Market share analysis, 2021

10.Company Profiles

10.1.Kedrion S.P.A

10.1.1.Overview

10.1.2.Business segments

10.1.3.Product portfolio

10.1.4.Financial performance

10.1.5.Recent developments

10.1.6.SWOT analysis

10.2.Octapharma AG

10.2.1.Overview

10.2.2.Business segments

10.2.3.Product portfolio

10.2.4.Financial performance

10.2.5.Recent developments

10.2.6.SWOT analysis

10.3.Japan Blood Products Organization

10.3.1.Overview

10.3.2.Business segments

10.3.3.Product portfolio

10.3.4.Financial performance

10.3.5.Recent developments

10.3.6.SWOT analysis

10.4.Biotest AG

10.4.1.Overview

10.4.2.Business segments

10.4.3.Product portfolio

10.4.4.Financial performance

10.4.5.Recent developments

10.4.6.SWOT analysis

10.5.CSL Behring

10.5.1.Overview

10.5.2.Business segments

10.5.3.Product portfolio

10.5.4.Financial performance

10.5.5.Recent developments

10.5.6.SWOT analysis

10.6.Grifols, S.A.

10.6.1.Overview

10.6.2.Business segments

10.6.3.Product portfolio

10.6.4.Financial performance

10.6.5.Recent developments

10.6.6.SWOT analysis

10.7.China Biologic Products Holdings, Inc.

10.7.1.Overview

10.7.2.Business segments

10.7.3.Product portfolio

10.7.4.Financial performance

10.7.5.Recent developments

10.7.6.SWOT analysis

10.8.Takeda Pharmaceutical Company Limited

10.8.1.Overview

10.8.2.Business segments

10.8.3.Product portfolio

10.8.4.Financial performance

10.8.5.Recent developments

10.8.6.SWOT analysis

10.9.Bio Products Laboratory Ltd.

10.9.1.Overview

10.9.2.Business segments

10.9.3.Product portfolio

10.9.4.Financial performance

10.9.5.Recent developments

10.9.6.SWOT analysis

10.10.LFB Group

10.10.1.Overview

10.10.2.Business segments

10.10.3.Product portfolio

10.10.4.Financial performance

10.10.5.Recent developments

10.10.6.SWOT analysis

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}