Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

SE2004156 |

Pages: 220 |

May 2023 |

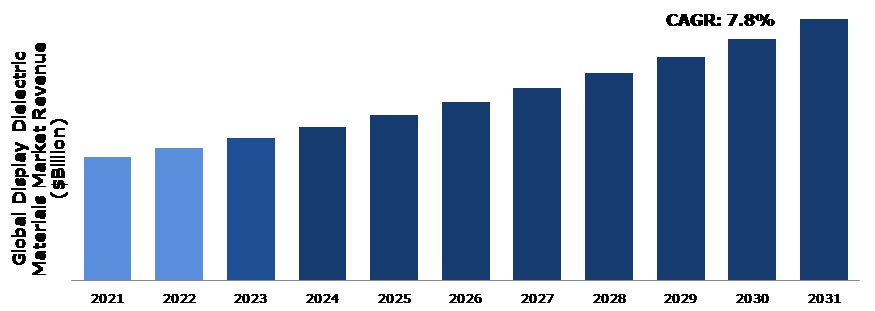

Display dielectric material is utilized in electronic displays such as organic light-emitting diode (OLED) displays and liquid crystal displays (LCDs). The major objective of the display dielectric material is to physically insulate the display. Dielectric materials have high electrical resistance and can store electrical energy in an electric field. The dielectric substance of a display helps in the regulation of the electric fields that are utilized to turn on the pixels. This, in turn, generates images of good quality.

Several types of materials can be used as display dielectrics including ceramics, liquid crystals, paper, mica, dielectric gases, etc. The selection of dielectric materials used in displays depends on various aspects including the performance requirements as well as the manufacturing method. The major characteristics of dielectric materials are breakdown voltage, dielectric constant, dielectric polarization, and thermal stability. Currently, the objective of ongoing research is to develop new dielectric materials with improved capabilities to support cutting-edge display technology.

Source: Research Dive Analysis

The pandemic had a moderate impact on the display dielectric materials market. In the initial months of the outbreak, the demand for dielectric materials was reduced due to a decline in the demand for consumer electronics. Moreover, disruptions in the supply chain, the closure of manufacturing plants, as well as an economic slowdown across several countries also impacted the demand for dielectric materials used in the displays.

However, due to the outbreak, many individuals opted for working and attending school from home. As a result, the demand for monitors and televisions increased significantly. This, in turn, increased the demand for dielectric materials used in display applications. Overall, the impact of the coronavirus outbreak on display dielectric materials has been complex, affecting the sector moderately. The pandemic disrupted the supply chains and production, but it also increased the demand for consumer electronics, which helped to mitigate these issues.

The increasing demand for LCD and OLED displays is one of the main drivers of the display dielectric materials market. As the demand of LCDs and OLEDs continues to grow, the demand for dielectric materials also increases. Dielectric materials play an important role in display manufacturing. They are used to make LEDs, OLEDs, LCDs, and other types of displays. The rising demand for high-resolution screens with good clarity as well as color accuracy is driving the demand for dielectric materials. Highly sensitive and accurate touch screen capacitive displays increasingly utilize dielectric materials with high dielectric constant and low loss tangents. The demand for dielectric materials that can withstand high temperatures and offer better insulation is also being driven by the increasing popularity of flexible displays. The increasing demand for smartphones, televisions, and automotive displays is further expected to boost the demand for dielectric materials during the forecast period.

To know more about global display dielectric materials market drivers, get in touch with our analysts here.

Despite the rising demand for dielectric materials in the display industry, some major barriers can hinder market growth. One such major barrier is the high cost of dielectric materials, which can deter their use in mass production. Advanced dielectric materials are hard to source, which in turn increases costs. Moreover, it is difficult to find dielectric materials needed for the development of novel display technologies with the qualities such as dielectric polarization, dielectric dispersion, and electric susceptibility. Due to the complex production procedures needed, high-performance dielectric materials can be expensive to produce.

The market for display dielectric materials has ample opportunities on account of the rising demand for advanced displays. There is a rising demand for dielectric materials that can withstand repeated bending and stretching without losing their characteristics. The demand for advanced displays with higher frequencies is also being driven by the development of 5G technology, which necessitates the use of dielectric materials with high dielectric constant and low loss tangents. The resolution of displays has increased dramatically in the last several years, generating images that are clearer and more detailed. These displays, which range in quality from Full HD (1920x1080) to 4K (3840x2160) and even 8K (7680x4320), offer improved clarity and finer visual details, creating immersive viewing experiences. Furthermore, display technology is developing at a rapid pace in areas like transparent displays, which have the great potential to completely revolutionize how users interact with digital content. As display technology develops further, new dielectric materials are being developed.

To know more about global display dielectric materials market opportunities, get in touch with our analysts here.

Source: Research Dive Analysis

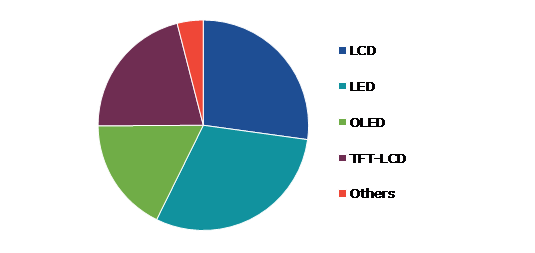

The LED sub-segment accounted for the highest market share in 2022. The demand for high-quality and energy-efficient displays in various applications has been increasing, which has led to an increased demand for LED displays in recent years. There has been increasing adoption of LED displays worldwide in sports events, concerts, as well as in retail, transportation, and hospitality sectors. LED displays offer advantages such as high brightness, vibrant colors, and low power consumption, making them an ideal choice for these applications. Dielectric materials play an important role in LED displays as they aid effective light emission and regulate the movement of electric charge. Indium tin oxide (ITO), which serves as a transparent electrode to apply an electric field to the LED material and permit light emission, is a type of dielectric material utilized in LED displays.

Dielectric materials are employed as insulating substrates in some LED designs to achieve electrical separation between the circuitry beneath the LED, prevent short circuits, and ensure correct gadget operation. Furthermore, to shield the semiconductor layers from external environmental elements such as moisture, dust, and mechanical stress, LEDs require encapsulation materials. Encapsulants are made of dielectric materials including silicone- or epoxy-based compounds, to offer insulation, thermal protection, and mechanical support.

Source: Research Dive Analysis

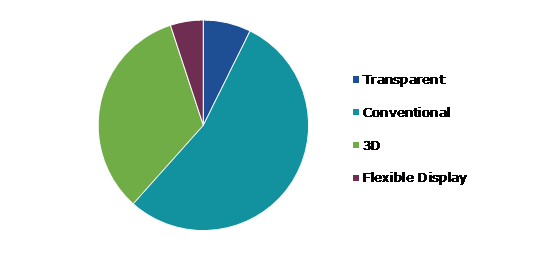

The conventional sub-segment accounted for the highest market share in 2022. To improve the performance of conventional displays such as LCDs, dielectric materials are utilized. In LCDs, these materials are used as an insulating layer between the electrodes and the liquid crystal material. Visual distortion or damage to the display due to the electrical shorts are avoided by maintaining a constant electric field across the liquid crystal layer. Silicon dioxide, aluminum oxide, and silicon nitride are some examples of dielectric materials used in conventional displays. Moreover, dielectric materials are also utilized to enhance the optical properties of the display. Thus, allowing for improved viewing angles and color accuracy.

Source: Research Dive Analysis

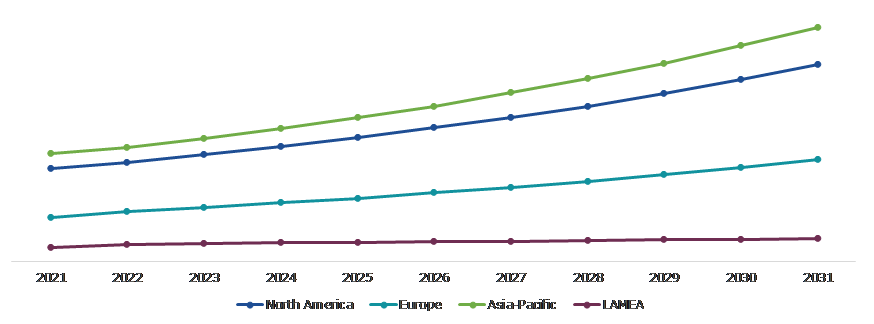

The Asia-Pacific display dielectric materials market generated the highest revenue in 2022. The demand for display dielectric materials in the Asia-Pacific region has been undergoing substantial growth in the last several years on account of the growth in demand for high-quality displays. Moreover, the shift to remote work as well as digitization has contributed to a substantial increase in the usage of laptops and smartphones in this region. Significant laptop sales have taken place in the region, particularly in countries such as Japan, China, South Korea, and India. Moreover, the region is home to some of the world's largest electronics manufacturers and has emerged as a major manufacturing hub for displays. China outperforms every other country in the world when it comes to display manufacturing. In addition, growing consumer electronic sales across this region, especially in India, Japan, and South Korea are expected to offer ample growth opportunities.

Investment and agreement are common strategies followed by major market players.

Source: Research Dive Analysis

Some of the leading display dielectric materials market players are Corning Incorporated, Merck KGaA, DuPont, SAMSUNG SDI CO., LTD., Nippon Chemical Industrial CO., LTD., SAKAI CHEMICAL INDUSTRY CO., LTD., LG Chem, DONGJIN SEMICHEM CO LTD., Nitto Denko Corporation, and ENF Technology.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2022 |

| Base Year for Market Estimation | 2023 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Technology |

|

| Segmentation by Application |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global display dielectric materials market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on display dielectric materials market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Display Dielectric Materials Market Analysis, by Technology

5.1.Overview

5.2.LCD

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region, 2022-2032

5.2.3.Market share analysis, by country, 2022-2032

5.3.LED

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region, 2022-2032

5.3.3.Market share analysis, by country, 2022-2032

5.4.OLED

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region, 2022-2032

5.4.3.Market share analysis, by country, 2022-2032

5.5.TFT-LCD

5.5.1.Definition, key trends, growth factors, and opportunities

5.5.2.Market size analysis, by region, 2022-2032

5.5.3.Market share analysis, by country, 2022-2032

5.6.Research Dive Exclusive Insights

5.6.1.Market attractiveness

5.6.2.Competition heatmap

6.Display Dielectric Materials Market Analysis, by Application

6.1.Transparent

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region, 2022-2032

6.1.3.Market share analysis, by country, 2022-2032

6.2.Conventional

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region, 2022-2032

6.2.3.Market share analysis, by country, 2022-2032

6.3.3D

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.2.Market size analysis, by region, 2022-2032

6.3.3.Market share analysis, by country, 2022-2032

6.4.Flexible Display

6.4.1.Definition, key trends, growth factors, and opportunities

6.4.2.Market size analysis, by region, 2022-2032

6.4.3.Market share analysis, by country, 2022-2032

6.5.Research Dive Exclusive Insights

6.5.1.Market attractiveness

6.5.2.Competition heatmap

7.Display Dielectric Materials Market, by Region

7.1.North America

7.1.1.U.S.

7.1.1.1.Market size analysis, by Technology, 2022-2032

7.1.1.2.Market size analysis, by Application, 2022-2032

7.1.2.Canada

7.1.2.1.Market size analysis, by Technology, 2022-2032

7.1.2.2.Market size analysis, by Application, 2022-2032

7.1.3.Mexico

7.1.3.1.Market size analysis, by Technology, 2022-2032

7.1.3.2.Market size analysis, by Application, 2022-2032

7.1.4.Research Dive Exclusive Insights

7.1.4.1.Market attractiveness

7.1.4.2.Competition heatmap

7.2.Europe

7.2.1.Germany

7.2.1.1.Market size analysis, by Technology, 2022-2032

7.2.1.2.Market size analysis, by Application, 2022-2032

7.2.2.UK

7.2.2.1.Market size analysis, by Technology, 2022-2032

7.2.2.2.Market size analysis, by Application, 2022-2032

7.2.3.France

7.2.3.1.Market size analysis, by Technology, 2022-2032

7.2.3.2.Market size analysis, by Application, 2022-2032

7.2.4.Spain

7.2.4.1.Market size analysis, by Technology, 2022-2032

7.2.4.2.Market size analysis, by Application, 2022-2032

7.2.5.Italy

7.2.5.1.Market size analysis, by Technology, 2022-2032

7.2.5.2.Market size analysis, by Application, 2022-2032

7.2.6.Rest of Europe

7.2.6.1.Market size analysis, by Technology, 2022-2032

7.2.6.2.Market size analysis, by Application, 2022-2032

7.2.7.Research Dive Exclusive Insights

7.2.7.1.Market attractiveness

7.2.7.2.Competition heatmap

7.3.Asia Pacific

7.3.1.China

7.3.1.1.Market size analysis, by Technology, 2022-2032

7.3.1.2.Market size analysis, by Application, 2022-2032

7.3.2.Japan

7.3.2.1.Market size analysis, by Technology, 2022-2032

7.3.2.2.Market size analysis, by Application, 2022-2032

7.3.3.India

7.3.3.1.Market size analysis, by Technology, 2022-2032

7.3.3.2.Market size analysis, by Application, 2022-2032

7.3.4.Australia

7.3.4.1.Market size analysis, by Technology, 2022-2032

7.3.4.2.Market size analysis, by Application, 2022-2032

7.3.5.South Korea

7.3.5.1.Market size analysis, by Technology, 2022-2032

7.3.5.2.Market size analysis, by Application, 2022-2032

7.3.6.Rest of Asia Pacific

7.3.6.1.Market size analysis, by Technology, 2022-2032

7.3.6.2.Market size analysis, by Application, 2022-2032

7.3.7.Research Dive Exclusive Insights

7.3.7.1.Market attractiveness

7.3.7.2.Competition heatmap

7.4.LAMEA

7.4.1.Brazil

7.4.1.1.Market size analysis, by Technology, 2022-2032

7.4.1.2.Market size analysis, by Application, 2022-2032

7.4.2.Saudi Arabia

7.4.2.1.Market size analysis, by Technology, 2022-2032

7.4.2.2.Market size analysis, by Application, 2022-2032

7.4.3.UAE

7.4.3.1.Market size analysis, by Technology, 2022-2032

7.4.3.2.Market size analysis, by Application, 2022-2032

7.4.4.South Africa

7.4.4.1.Market size analysis, by Technology, 2022-2032

7.4.4.2.Market size analysis, by Application, 2022-2032

7.4.5.Rest of LAMEA

7.4.5.1.Market size analysis, by Technology, 2022-2032

7.4.5.2.Market size analysis, by Application, 2022-2032

7.4.6.Research Dive Exclusive Insights

7.4.6.1.Market attractiveness

7.4.6.2.Competition heatmap

8.Competitive Landscape

8.1.Top winning strategies, 2022

8.1.1.By strategy

8.1.2.By year

8.2.Strategic overview

8.3.Market share analysis, 2022

9.Company Profiles

9.1.Corning Incorporated

9.1.1.Overview

9.1.2.Business segments

9.1.3.Product portfolio

9.1.4.Financial performance

9.1.5.Recent developments

9.1.6.SWOT analysis

9.2.Merck KGaA

9.2.1.Overview

9.2.2.Business segments

9.2.3.Product portfolio

9.2.4.Financial performance

9.2.5.Recent developments

9.2.6.SWOT analysis

9.3.DuPont

9.3.1.Overview

9.3.2.Business segments

9.3.3.Product portfolio

9.3.4.Financial performance

9.3.5.Recent developments

9.3.6.SWOT analysis

9.4.SAMSUNG SDI CO.,LTD.

9.4.1.Overview

9.4.2.Business segments

9.4.3.Product portfolio

9.4.4.Financial performance

9.4.5.Recent developments

9.4.6.SWOT analysis

9.5.Nippon Chemical Industrial CO., LTD.

9.5.1.Overview

9.5.2.Business segments

9.5.3.Product portfolio

9.5.4.Financial performance

9.5.5.Recent developments

9.5.6.SWOT analysis

9.6.SAKAI CHEMICAL INDUSTRY CO.,LTD.

9.6.1.Overview

9.6.2.Business segments

9.6.3.Product portfolio

9.6.4.Financial performance

9.6.5.Recent developments

9.6.6.SWOT analysis

9.7.LG Chem

9.7.1.Overview

9.7.2.Business segments

9.7.3.Product portfolio

9.7.4.Financial performance

9.7.5.Recent developments

9.7.6.SWOT analysis

9.8.DONGJIN SEMICHEM CO LTD.

9.8.1.Overview

9.8.2.Business segments

9.8.3.Product portfolio

9.8.4.Financial performance

9.8.5.Recent developments

9.8.6.SWOT analysis

9.9.Nitto Denko Corporation

9.9.1.Overview

9.9.2.Business segments

9.9.3.Product portfolio

9.9.4.Financial performance

9.9.5.Recent developments

9.9.6.SWOT analysis

9.10.ENF Technology

9.10.1.Overview

9.10.2.Business segments

9.10.3.Product portfolio

9.10.4.Financial performance

9.10.5.Recent developments

9.10.6.SWOT analysis

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}