Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

MA2003153 |

Pages: 240 |

May 2023 |

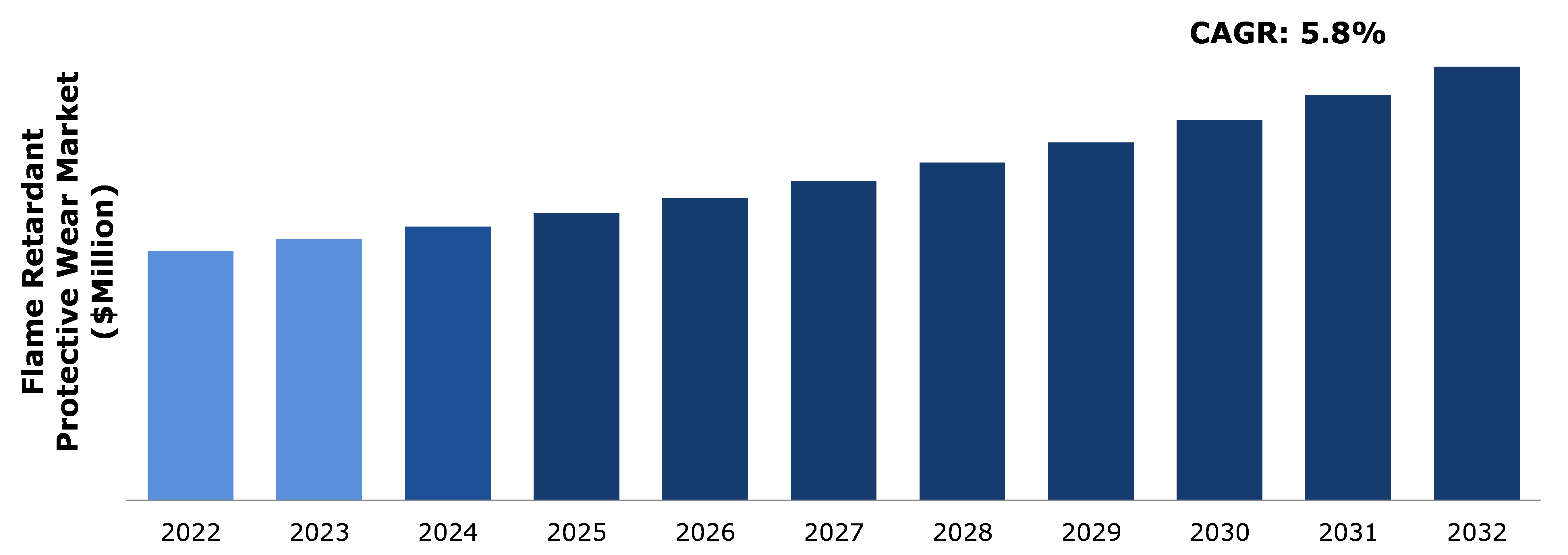

The rapid rise of industrialization has increased the need for workplace safety especially in the industrial and manufacturing sectors. This necessitates the use of flame retardant protective wear materials to ensure the workers safety. Furthermore, in the electronics manufacturing sector, there is the need for flame retardants to reduce the combustibility of semiconductors, as well as the demand for flame retardant fabrics in the chemical sector. This is one of the major factors driving the flame retardant protective wear market growth. In addition, the end-use industries namely automotive, manufacturing, construction, and others use flame retardant protective wear to ensure the safety of workers. These factors are anticipated to boost the flame retardant protective wear market size during the forecast period.

However, rules are essential for guaranteeing safety of customers and employees and can set market-wide standards for efficacy as well as quality. The user needs to note that the flame retardant protective wear are not completely fireproof. In extreme cases, these materials can catch fire causing injuries. All these factors are projected to hamper the flame retardant protective wear industry demand during the forecast years.

Rising demand for flame retardant protective wear from emergency department such as firefighting sector is anticipated to generate excellent opportunities in the market. For instance, the availability of different fabric-fire procedures such as CRIB-5 and BS-476, are expected to benefit the market. In addition, the use of fire-resistant fabrics in firefighters' uniforms and equipment to reduce fire hazards is expected to drive its global demand. Flame retardants (FRs) are available in a variety of materials, including cellulose, PET, polyamides, plastics, polyolefin, wood, cables, and electronic products. The world's rising population, infrastructure, and industrialization all have an impact on the use of flame retardant protective wear. Furthermore, widespread information on disaster preparedness and mitigation, fire legislation, and workplace safety are factors critical for the market growth.

According to regional analysis, the North America flame retardant protective wear market accounted for the highest market size in 2022. The market for flame retardant protective wear is driven by several factors, including government regulations and safety standards, increasing awareness of workplace safety, and the growth of industries such as oil & gas, chemicals, and construction, which require workers to operate in potentially hazardous environments.

Flame retardant protective wear comprises of the fabrics and garments that can withstand high temperature, fire, and heat. Flame retardant protective wear is made from meta-aramid fabrics that offers flame and heat resistance. Chemicals or materials used to stop the spread of flames are called flame-retardants. The purpose of flame-retardant protective wear is to reduce the possibility of a fire starting from a heat source, such as a candle, an electrical fault, or a cigarette.

During the COVID-19 pandemic, the market for flame-retardant protective clothing experienced significant supply chain disruptions. A number of factors, such as industrial closures, border restrictions, and raw material shortages, have contributed to these delays. Global supply lines are a common source of materials and components for makers of flame retardant protective clothing. For instance, the shutdown of factories in nations like China, a key producer of textiles and materials that are flame-resistant, resulted in shortages and delays in the manufacturing of these products. Transporting raw materials and finished goods across borders has also been challenging due to border restrictions. Due to this, finished goods and raw materials have been delivered to clients later than expected.

Furthermore, the flame retardant protective wear market demand from the end-use industries namely oil & gas and electronics manufacturing was significantly hampered owing to shutdown of operations. The manufacturers were forced to temporarily shut down their manufacturing facilities. Therefore, the price and quantity chain was interrupted, which had an impact on the market.

The increase in demand from various industries such as automotive, production, and manufacturing are giving a significant boost to the growth of the flame retardant protective wear market. Also, the market is majorly driven by factors such as rising awareness about work safety across the globe and the implementation of government regulations regarding safety at workplace. Large-scale and vertically integrated companies in the flame retardant apparel market maintain a competitive advantage due to easy access to raw materials. Furthermore, by diversifying their product offerings through increased investments in R&D facilities, leading companies are expected to create excellent opportunities in the flame retardant protective wear industry in the upcoming years.

To know more about global flame retardant protective wear market drivers, get in touch with our analysts here.

The high cost of flame retardant fabrics, particularly in developed economies, has been a significant impediment for the flame retardant protective wear manufacturers. The high cost of fabrics and raw materials, as well as the high cost of investment, has resulted in an increase in the cost of flame retardant protective wear products. Furthermore, the high cost of production and testing has added to the cost of manufacturing, raising the cost of flame retardant protective wear. Therefore, the growth of the flame retardant protective wear market has been restrained.

Continuous technological advancements in product manufacturing to improve product quality, performance, and material durability are potential opportunities for the market growth. Furthermore, to attract customers, key market players are focusing on unique product design by incorporating advanced features into their existing product portfolios and using environmentally friendly materials. This factor is expected to drive the market growth in the upcoming years. The rapid expansion of end-use industries is expected to generate a large number of growth opportunities for the flame retardant protective wear industry players in the future.

To know more about global flame retardant protective wear market opportunities, get in touch with our analysts here.

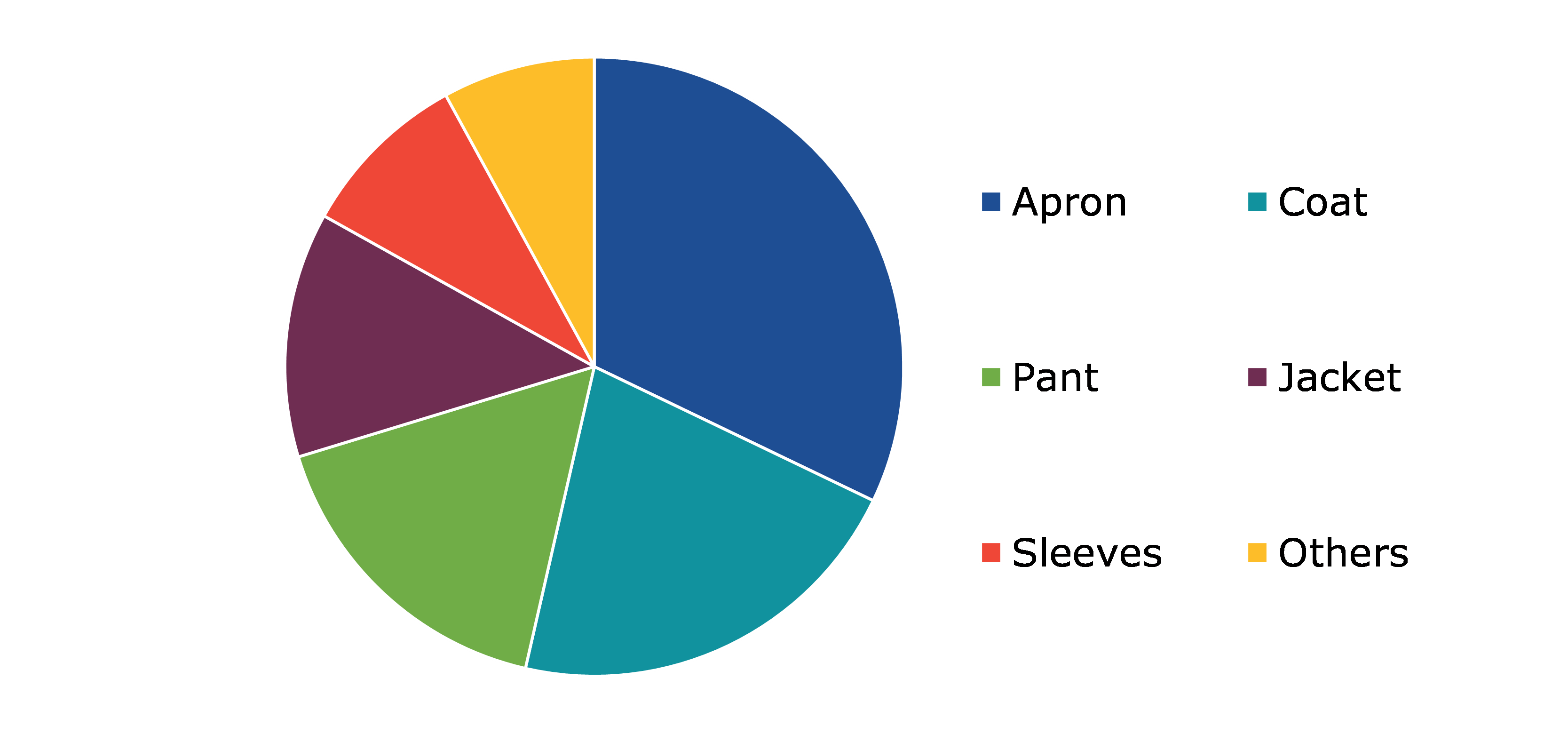

Based on product, the market has been divided into apron, coat, pant, jacket, sleeves, and others. Among these, the apron sub-segment accounted for the highest market share in 2022 and is estimated to show the fastest growth during the forecast period.

Source: Research Dive Analysis

The apron sub-segment accounted for a dominant market size in 2022. This growth is majorly owing to the use of aprons in oil & gas, manufacturing, construction, food processing, and other sectors. Apron is also inherent flame resistant (FR) and this property is permanent and cannot be washed or worn off. In addition, the apron offers excellent protection against molten metal and aluminum splash. The aprons offer excellent safety by suppressing or reducing the ignition of garments specially during fire, flames, slags, or other businesses. Apron offers excellent protection against heat, fire resistance, and exposure to other workplace hazards. These factors are projected to drive the sub-segment growth.

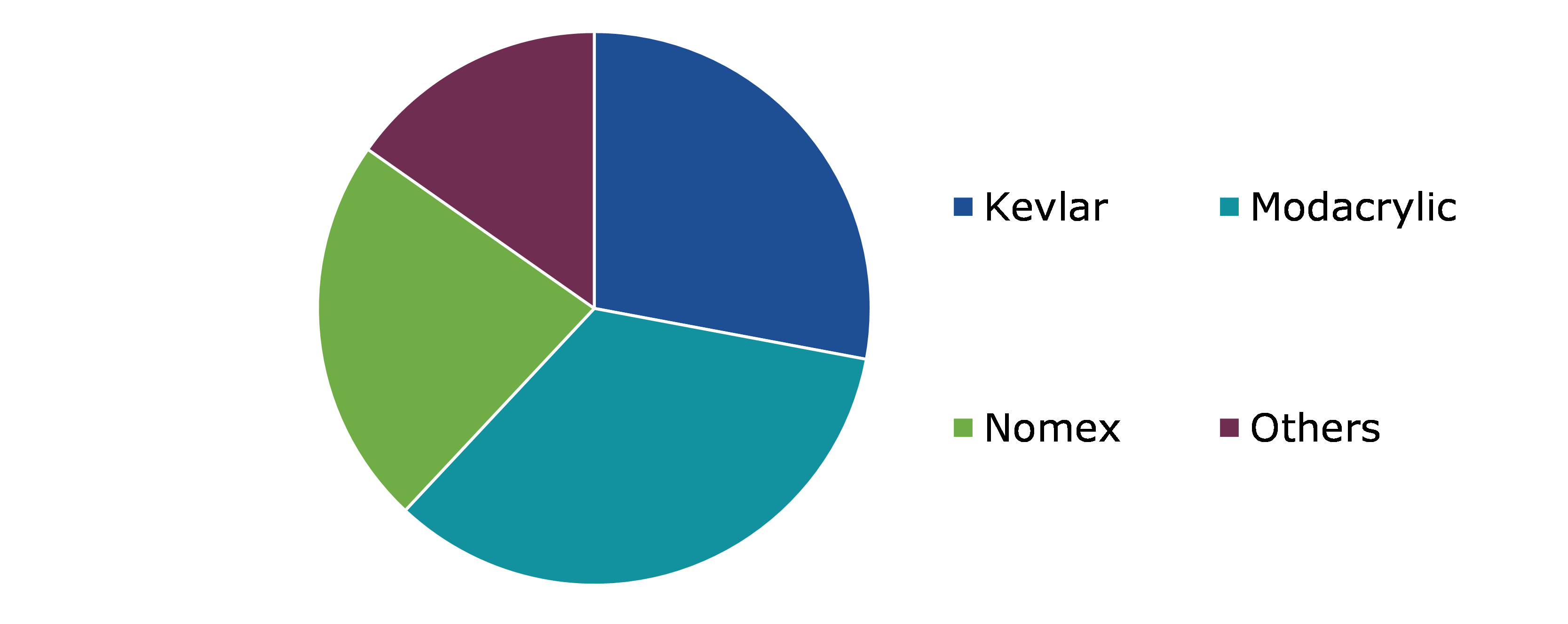

Based on material, the market has been divided into kevlar, modacrylic, nomex, and others. Among these, the modacrylic sub-segment accounted for the highest revenue share in 2022.

Source: Research Dive Analysis

The modacrylic sub-segment accounted for a dominant market share in 2022. Modacrylic fibers are made from resins that are acrylonitrile copolymers with other materials like vinylidene chloride, vinyl chloride, or vinyl bromide. These materials are added to the fiber to improve its flame resistance. Modacrylic fiber is widely used in high-performance protective clothing, such as firefighting turnout gear owing to its flame resistance combined with other desirable textile properties, such as durability and a good hand feel.

Technological advancements in the artificial fur industry have encouraged fashion designers, retailers, and apparel manufacturers to switch from using animal fur to using synthetic fur, such as faux fur, in the production of their products. The increasing standardization and industrialization are also anticipated to accelerate the need for modacrylic based flame retardant protective wear.

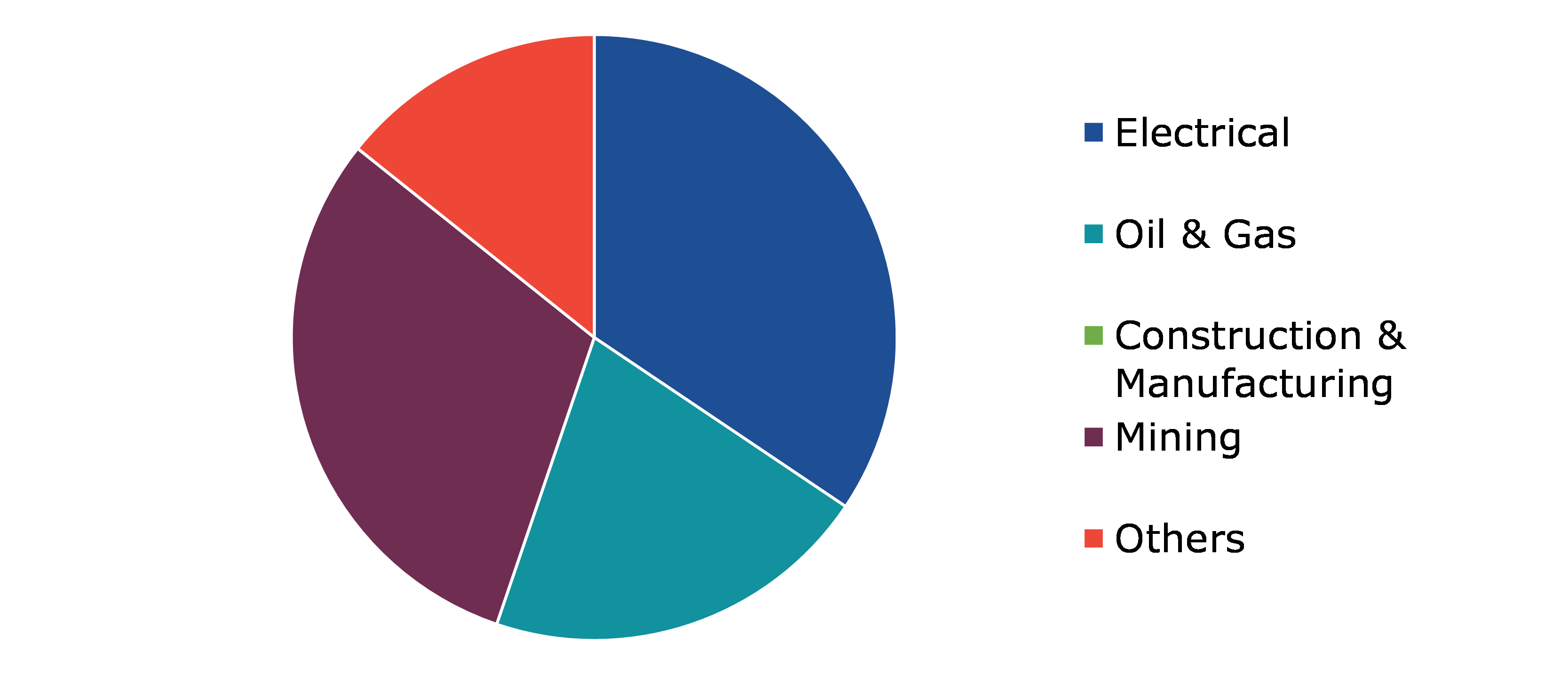

Based on end-use industry, the market has been divided into electrical, oil & gas, construction & manufacturing, mining, and others. Among these, the electrical sub-segment accounted for the highest revenue share in 2022.

Source: Research Dive Analysis

The electrical sub-segment accounted for a dominant market share in 2022. In the electrical industry, flame retardant protective wear plays a vital role in preventing the injuries due to electric arc, flash, explosion, and fire. This clothing reduces the risk of fire and explosion when the workers come in contact with electrical equipment. The electronics industry works with governments, standards-setting bodies, and other stakeholders to continuously evaluate the materials it uses in its products to ensure safety standards and environmental stewardship requirements are met. Flame retardant clothing is necessary for a number of industries, such as manufacturing and engineering. Welders, electricians, and anyone who works around open flames need to wear suitable flame retardant clothing and Personal Protective Equipment (PPE).

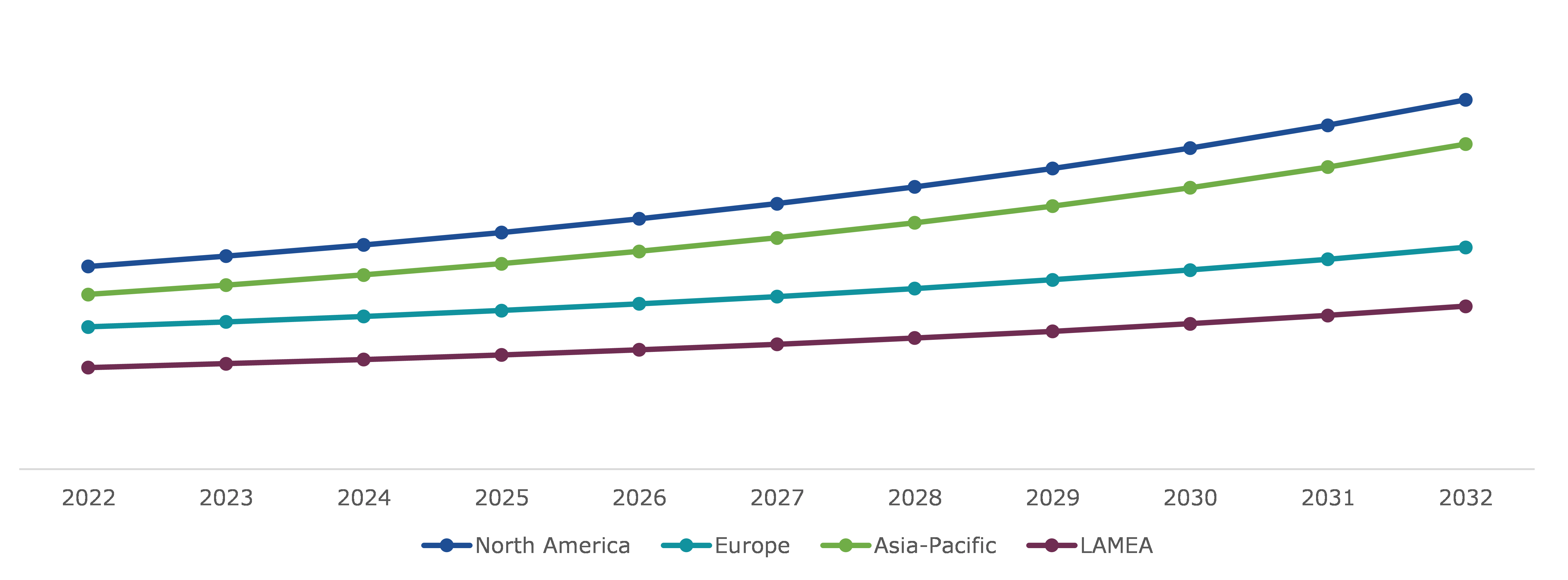

The flame retardant protective wear market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The North America flame retardant protective wear market is expected to experience significant growth opportunities and generate significant revenue during the forecast period. Flame retardant protective clothing is used to protect workers in end-use industries such as construction, mining, petrochemical, and manufacturing, which are expected to create numerous opportunities in the North America market. The global market is dominated by the North America region and is expected to continue its dominance during the forecast period. This is mainly due to various regulations executed in North America for flame retardant protective wear for workplace safety.

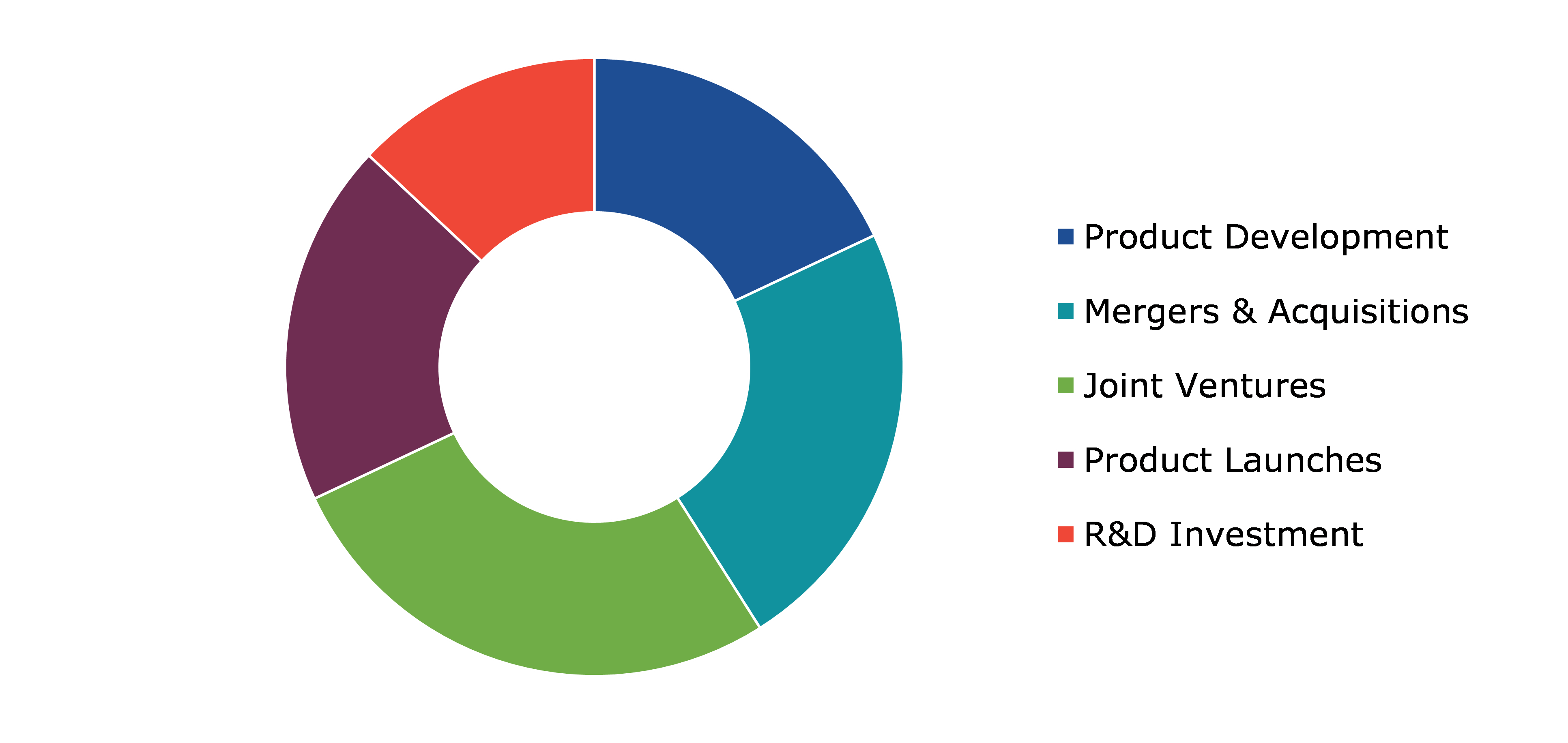

Investment and agreement are common strategies followed by major market players. For instance, in July 2019, Wearwell, the leading company in protective wear launched cutting-edge new multi-norm arc flash protection and flame-resistant clothing range.

Source: Research Dive Analysis

Some of the leading flame retardant protective wear market players are ANSELL LTD, 3M, VF CORPORATION, Honeywell International Inc., Lakeland Inc, Kimberly Clark Corp, DuPont, SOLVAY, International Enviroguard, and W. L. Gore & Associates Inc.

| Aspect | Particulars |

| Historical Market Estimations | 2021 |

| Base Year for Market Estimation | 2022 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Product |

|

| Segmentation by Material |

|

| Segmentation by End-use Industry |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global flame retardant protective wear market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on flame retardant protective wear market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Flame Retardant Protective Wear Market Analysis, by Product

5.1.Overview

5.2.Apron

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region

5.2.3.Market share analysis, by country

5.3.Coat

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region

5.3.3.Market share analysis, by country

5.4.Pant

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region

5.4.3.Market share analysis, by country

5.5.Jacket

5.5.1.Definition, key trends, growth factors, and opportunities

5.5.2.Market size analysis, by region

5.5.3.Market share analysis, by country

5.6.Sleeves

5.6.1.Definition, key trends, growth factors, and opportunities

5.6.2.Market size analysis, by region

5.6.3.Market share analysis, by country

5.6.4.Research Dive Exclusive Insights

5.7.Others

5.7.1.Definition, key trends, growth factors, and opportunities

5.7.2.Market size analysis, by region

5.7.3.Market share analysis, by country

5.7.4.Research Dive Exclusive Insight

5.8.Research Dive Exclusive Insights

5.8.1.Market attractiveness

5.8.2.Competition heatmap

6.Flame Retardant Protective Wear Market Analysis, by Material

6.1.Kevlar

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region

6.1.3.Market share analysis, by country

6.2.Modacrylic

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region

6.2.3.Market share analysis, by country

6.3.Nomex

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.2.Market size analysis, by region

6.3.3.Market share analysis, by country

6.4.Others

6.4.1.Definition, key trends, growth factors, and opportunities

6.4.2.Market size analysis, by region

6.4.3.Market share analysis, by country

6.5.Research Dive Exclusive Insights

6.5.1.Market attractiveness

6.5.2.Competition heatmap

7.Flame Retardant Protective Wear Market Analysis, by End-use Industry

7.1.Electrical

7.1.1.Definition, key trends, growth factors, and opportunities

7.1.2.Market size analysis, by region

7.1.3.Market share analysis, by country

7.2.Oil & Gas

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region

7.2.3.Market share analysis, by country

7.3.Construction & Manufacturing

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region

7.3.3.Market share analysis, by country

7.4.Mining

7.4.1.Definition, key trends, growth factors, and opportunities

7.4.2.Market size analysis, by region

7.4.3.Market share analysis, by country

7.5.Others

7.5.1.Definition, key trends, growth factors, and opportunities

7.5.2.Market size analysis, by region

7.5.3.Market share analysis, by country

8.Flame Retardant Protective Wear Market, by Region

8.1.North America

8.1.1.U.S.

8.1.1.1.Market size analysis, by Product

8.1.1.2.Market size analysis, by Material

8.1.1.3.Market size analysis, by End-use Industry

8.1.2.Canada

8.1.2.1.Market size analysis, by Product

8.1.2.2.Market size analysis, by Material

8.1.2.3.Market size analysis, by End-use Industry

8.1.3.Mexico

8.1.3.1.Market size analysis, by Product

8.1.3.2.Market size analysis, by Material

8.1.3.3.Market size analysis, by End-use Industry

8.1.4.Research Dive Exclusive Insights

8.1.4.1.Market attractiveness

8.1.4.2.Competition heatmap

8.2.Europe

8.2.1.Germany

8.2.1.1.Market size analysis, by Product

8.2.1.2.Market size analysis, by Material

8.2.1.3.Market size analysis, by End-use Industry

8.2.2.UK

8.2.2.1.Market size analysis, by Product

8.2.2.2.Market size analysis, by Material

8.2.2.3.Market size analysis, by End-use Industry

8.2.3.France

8.2.3.1.Market size analysis, by Product

8.2.3.2.Market size analysis, by End-use Industry

8.2.4.Spain

8.2.4.1.Market size analysis, by Product

8.2.4.2.Market size analysis, by Material

8.2.4.3.Market size analysis, by End-use Industry

8.2.5.Italy

8.2.5.1.Market size analysis, by Product

8.2.5.2.Market size analysis, by Material

8.2.5.3.Market size analysis, by End-use Industry

8.2.6.Rest of Europe

8.2.6.1.Market size analysis, by Product

8.2.6.2.Market size analysis, by Material

8.2.6.3.Market size analysis, by End-use Industry

8.2.7.Research Dive Exclusive Insights

8.2.7.1.Market attractiveness

8.2.7.2.Competition heatmap

8.3.Asia-Pacific

8.3.1.China

8.3.1.1.Market size analysis, by Product

8.3.1.2.Market size analysis, by Material

8.3.1.3.Market size analysis, by End-use Industry

8.3.2.Japan

8.3.2.1.Market size analysis, by Product

8.3.2.2.Market size analysis, by Material

8.3.2.3.Market size analysis, by End-use Industry

8.3.3.India

8.3.3.1.Market size analysis, by Product

8.3.3.2.Market size analysis, by Material

8.3.3.3.Market size analysis, by End-use Industry

8.3.4.Australia

8.3.4.1.Market size analysis, by Product

8.3.4.2.Market size analysis, by Material

8.3.4.3.Market size analysis, by End-use Industry

8.3.5.South Korea

8.3.5.1.Market size analysis, by Product

8.3.5.2.Market size analysis, by Material

8.3.5.3.Market size analysis, by End-use Industry

8.3.6.Rest of Asia-Pacific

8.3.6.1.Market size analysis, by Product

8.3.6.2.Market size analysis, by Material

8.3.6.3.Market size analysis, by End-use Industry

8.3.7.Research Dive Exclusive Insights

8.3.7.1.Market attractiveness

8.3.7.2.Competition heatmap

8.4.LAMEA

8.4.1.Brazil

8.4.1.1.Market size analysis, by Product

8.4.1.2.Market size analysis, by Material

8.4.1.3.Market size analysis, by End-use Industry

8.4.2.Saudi Arabia

8.4.2.1.Market size analysis, by Product

8.4.2.2.Market size analysis, by Material

8.4.2.3.Market size analysis, by End-use Industry

8.4.3.UAE

8.4.3.1.Market size analysis, by Product

8.4.3.2.Market size analysis, by Material

8.4.3.3.Market size analysis, by End-use Industry

8.4.4.South Africa

8.4.4.1.Market size analysis, by Product

8.4.4.2.Market size analysis, by Material

8.4.4.3.Market size analysis, by End-use Industry

8.4.5.Rest of LAMEA

8.4.5.1.Market size analysis, by Product

8.4.5.2.Market size analysis, by Material

8.4.5.3.Market size analysis, by End-use Industry

8.4.6.Research Dive Exclusive Insights

8.4.6.1.Market attractiveness

8.4.6.2.Competition heatmap

9.Competitive Landscape

9.1.Top winning strategies, 2021

9.1.1.By strategy

9.1.2.By year

9.2.Strategic overview

9.3.Market share analysis, 2021

10.Company Profiles

10.1.ANSELL LTD.

10.1.1.Overview

10.1.2.Business segments

10.1.3.Product portfolio

10.1.4.Financial performance

10.1.5.Recent developments

10.1.6.SWOT analysis

10.2.3M

10.2.1.Overview

10.2.2.Business segments

10.2.3.Product portfolio

10.2.4.Financial performance

10.2.5.Recent developments

10.2.6.SWOT analysis

10.3.VF CORPORATION

10.3.1.Overview

10.3.2.Business segments

10.3.3.Product portfolio

10.3.4.Financial performance

10.3.5.Recent developments

10.3.6.SWOT analysis

10.4.Honeywell International Inc.,

10.4.1.Overview

10.4.2.Business segments

10.4.3.Product portfolio

10.4.4.Financial performance

10.4.5.Recent developments

10.4.6.SWOT analysis

10.5.Lakeland Inc.

10.5.1.Overview

10.5.2.Business segments

10.5.3.Product portfolio

10.5.4.Financial performance

10.5.5.Recent developments

10.5.6.SWOT analysis

10.6.Kimberly Clark Corp

10.6.1.Overview

10.6.2.Business segments

10.6.3.Product portfolio

10.6.4.Financial performance

10.6.5.Recent developments

10.6.6.SWOT analysis

10.7.DuPont

10.7.1.Overview

10.7.2.Business segments

10.7.3.Product portfolio

10.7.4.Financial performance

10.7.5.Recent developments

10.7.6.SWOT analysis

10.8.SOLVAY

10.8.1.Overview

10.8.2.Business segments

10.8.3.Product portfolio

10.8.4.Financial performance

10.8.5.Recent developments

10.8.6.SWOT analysis

10.9.International Enviroguard

10.9.1.Overview

10.9.2.Business segments

10.9.3.Product portfolio

10.9.4.Financial performance

10.9.5.Recent developments

10.9.6.SWOT analysis

10.10.W. L. Gore & Associates Inc

10.10.1.Overview

10.10.2.Business segments

10.10.3.Product portfolio

10.10.4.Financial performance

10.10.5.Recent developments

10.10.6.SWOT analysis

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}