Medical Devices Market Size Share Competitive Landscape And Trend Analysis Report Report

RA00723

Medical Devices Market Size, Share, Competitive Landscape and Trend Analysis Report by Type, End User, and Region: Global Opportunity Analysis and Industry Forecast, 2024-2033

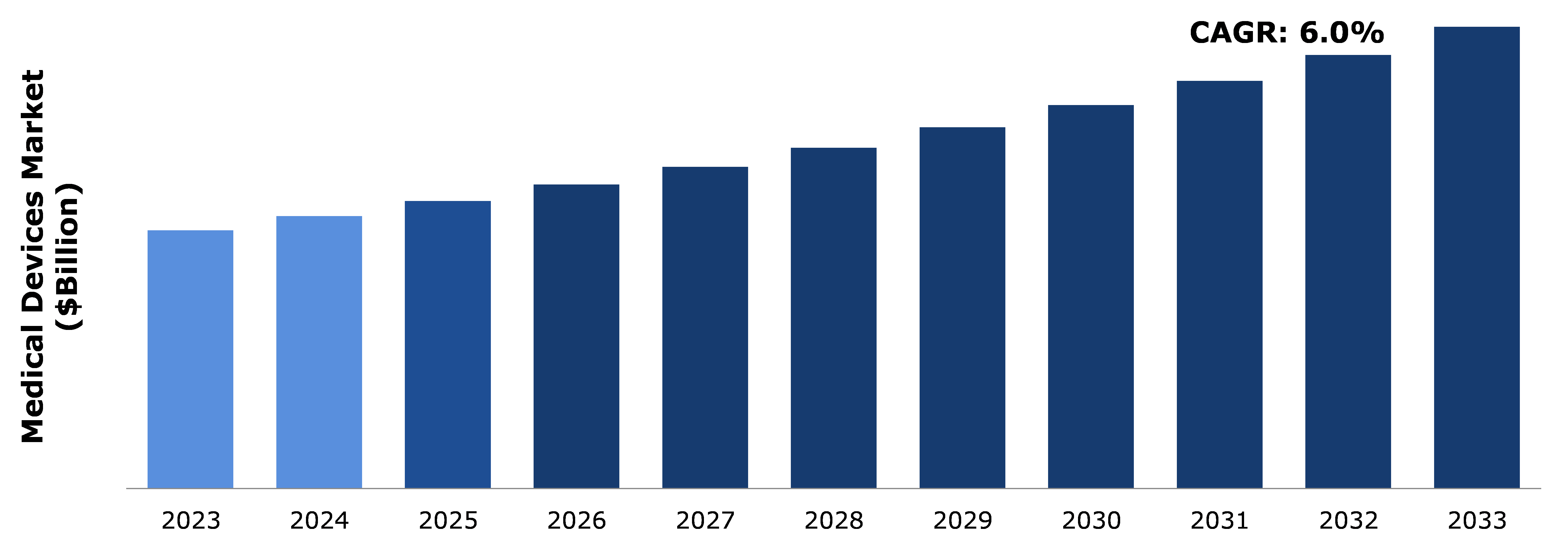

The medical devices market was valued at $531.4 billion in 2023 and is estimated to reach $950.4 billion by 2033, exhibiting a CAGR of 6.0% from 2024 to 2033.

Market Definition and Overview

Medical devices encompass a wide range of tools and technologies crucial for healthcare delivery, spanning from basic items like syringes to advanced systems such as pacemakers and artificial pancreas devices. These devices also include in vitro diagnostic products like blood glucose meters and medical imaging equipment such as ultrasound and CT scanners. Widely used medical devices range from single-use items like catheters to implantable devices like hip prostheses, facilitating various healthcare interventions and treatments. The nomenclature of medical devices serves as a standardized coding and naming system, aiming to classify and identify these diverse products comprehensively. Examples of widely used medical devices include syringes, pacemakers, ultrasound machines, and personal protective equipment like masks & gloves, and others

Key Takeaways

- The medical devices market study covers 20 countries. The research includes a segment analysis of each country in terms of value ($billion) for the projected period from 2024 to 2033.

- More than 1,500 product literatures, industry releases, annual reports, and other such documents of major medical devices industry participants along with authentic industry journals, trade associations' releases, and government websites have been reviewed for generating high-value industry insights.

- The study integrates high-quality data, professional opinions and analysis, and critical independent perspectives. The research approach intends to provide a balanced view of global markets and assist stakeholders in making informed decisions in order to achieve their most ambitious growth objectives.

Industry Trends

- On May 01, 2024, Medline announced its acquisition of Ecolab's global surgical solutions business for $950 million, focusing on sterile drapes and fluid temperature management systems. Ecolab's surgical solutions, including Microtek product lines, generated over $400 million in sales in 2023. The transaction, subject to regulatory approvals, is anticipated to close in the second half of 2024, facilitating Medline's expansion in critical healthcare sectors.

- On May 01, 2024, Senseonics secured FDA's integrated continuous glucose monitoring (iCGM) approval for de novo pathway, enabling integration of its Eversense CGM implant with insulin pumps. The move expands device appeal to a broader patient population. Senseonics plans to pursue partnerships with pump manufacturers for automated insulin delivery systems. First-in-human testing for self-powered versions is expected to begin in the second half of 2024.

- On April 30, 2024, Abbott secured FDA approval for its Esprit resorbable scaffold system, aimed at treating blocked arteries below the knee. Designed to deliver the immunosuppressant everolimus, the device reduces vessel re-narrowing rates compared to balloon angioplasty in patients with chronic limb-threatening ischemia.

Key Market Dynamics

The medical devices market growth is driven by the critical role these devices play in healthcare systems worldwide. For instance, the increasing recognition of medical devices as fundamental components of health systems due to their essential functions in disease prevention, diagnosis, treatment, and rehabilitation, drives their demand. Moreover, the rapid growth of the medical device market is boosted by technological advancements aimed at enhancing patient welfare.

While medical devices play a crucial role in healthcare, their regulation faces inherent complexities. In addition, regulatory processes, such as premarket review and classification, can be time-consuming and costly for manufacturers. Limited access to innovative devices due to high development costs further impedes progress. These factors collectively contribute to restrictions in the regulation and availability of medical devices, impacting patient care and technological advancement.

Technological advancements in the field of medical devices is predicted to generate excellent opportunities in the market. For instance, 3D printing revolutionizes device manufacturing, increasing affordability and accessibility. Advancements in biomedical engineering enable targeted drug delivery and minimally invasive procedures, enhancing patient outcomes. In addition, medical devices play a crucial role in chronic disease management, empowering patients with continuous monitoring and improving overall quality of life.

Global Medical Devices Market Ecosystem Analysis

In the ever-evolving landscape of medical device companies, several industry giants are known for their commitment toward innovation, quality, and global impact. Among these leaders are Medtronic, Abbott Laboratories, Johnson & Johnson MedTech, Siemens Healthineers, and others. These companies have not only reported substantial revenues and net incomes but have also demonstrated impressive investments in R&D. Through strategic acquisitions, groundbreaking product launches, and impactful collaborations, they continue to shape the future of healthcare, driving unprecedented advancements in diagnostic accuracy, patient care, and treatment modalities.

Top Medical Devices Companies Globally by Revenue ($Billion), 2023

Market Segmentation

The medical devices market is segmented into type, end user, and region. On the basis of type, the market is divided into orthopedic devices, diagnostic imaging, in vitro diagnostics (IVD), cardiovascular devices, wound management, minimally invasive surgical (MIS), diabetes care, dental devices, ophthalmic devices, general surgery, and others. Based on end user, the market is divided into hospitals & ambulatory surgery centers (ASCs), clinics, and others. Region wise, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

Country Market Outlook

The Indian medical devices industry is experiencing robust growth, with the market size projected to reach $50 billion by 2025, boasting a steady Compound Annual Growth Rate (CAGR) of 15% over the last three years. The sector encompasses five major segments, including consumables & disposables, diagnostic imaging, dental products, orthopedics & prosthetics, and patient aids. Domestically, the market is largely driven by 750-800 Indian manufacturers, constituting 65% of the industry.

Several growth factors drive this expansion, including India's growing population, increasing life expectancy, and the rising burden of non-communicable diseases (NCDs). Also, changing preferences towards preventive healthcare, rise of health insurance coverage and medical tourism contribute to the industry's upward trajectory, complemented by infrastructural developments such as the establishment of medical device parks. For instance, the country's manufacturing landscape is evolving with the development of dedicated medical device manufacturing clusters and parks in states like Himachal Pradesh, Tamil Nadu, Madhya Pradesh, and Uttar Pradesh. These factors collectively position India's medical devices industry as a vital player in the global healthcare market.

Competitive Landscape

Some of the major players operating in the medical devices market include Medtronic, Koninklijke Philips N.V., Johnson & Johnson Services, Inc., Abbott, Siemens Healthineers AG, Stryker, GE Healthcare, BD, Cardinal Health, and Boston Scientific Corporation, and others.

Recent Key Strategies and Developments

- On May 13, 2024, Siemens Healthineers announced a $270 million (£250m) investment in a new UK facility focused on producing superconducting magnets for MRI devices. Located in North Oxfordshire, the site aims to create 1,300 jobs and minimize helium usage, utilizing DryCool technology to reduce helium requirement to under a liter per MRI scanner. Scheduled to open in 2026, the 56,000m2 facility will be carbon-neutral.

- On May 07, 2024, KKR, an investment company, has agreed to acquire Indian medical devices company Healthium MedTech, valued at $838.60 million (INR 70 billion). The deal involves KKR-managed funds acquiring Healthium from an affiliate of Apax Partners. Healthium, founded in 1992, specializes in surgical products globally, including arthroscopy and wound closure items.

- In January 2024, India introduced the National Single Window System (NSWS), a centralized portal aimed at streamlining the management of medical devices. Developed by Tata Consultancy Services (TCS), NSWS replaces existing portals and facilitates applications for registration, licenses, and various approvals required for medical device manufacturing and importation. With India's medical device demand projected to hit $50 billion by 2030, NSWS aims to enhance ease of doing business by providing a unified interface for investors, eliminating the need for multiple platforms and authorities.

Key Sources Referred

- World Health Organization

- National Library of Medicine

- ELF European Lung Foundation

- National Health Council

- U.S. Department of Health & Human Services

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the medical devices market segments, current trends, estimations, and dynamics of the medical devices market analysis from 2023 to 2033 to identify the prevailing medical devices market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the medical devices market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global medical devices market statistics.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global medical devices market trends, key players, market segments, application areas, and market growth strategies.

The report offers comprehensive analysis of key players operating in the global market by analyzing their business performance, product portfolio, business segments, revenue, and strategic moves to showcase the competitive scenario in the industry.

| Aspect | Particulars |

| Historical Market Estimations | 2021-2022 |

| Base Year for Market Estimation | 2023 |

| Forecast Timeline for Market Projection | 2024-2033 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Type |

|

| Segmentation by End User |

|

| Key Companies Profiled |

|

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.5. Market size estimation

1.5.1. Top-down approach

1.5.2. Bottom-up approach

2. Report Scope

2.1. Market Definition

2.2. Key objectives of the study

2.3. Market segmentation

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Growth impact forces

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.3. Market value chain analysis

4.3.1. List of suppliers

4.3.2. List of manufacturers

4.3.3. List of distributors

4.4. Innovation & sustainability matrices

4.4.1. Technology matrix

4.4.2. Regulatory matrix

4.5. Porter’s five forces analysis

4.5.1. Bargaining power of suppliers

4.5.2. Bargaining power of consumers

4.5.3. Threat of substitutes

4.5.4. Threat of new entrants

4.5.5. Competitive Rivalry Intensity

4.6. PESTLE analysis

4.6.1. Political

4.6.2. Economical

4.6.3. Social

4.6.4. Technological

4.6.5. Legal

4.6.6. Environmental

4.7. Impact of COVID-19 on the Medical Devices Market

4.7.1. Pre-covid market scenario

4.7.2. Post-covid market scenario

5. Medical Devices Market Analysis, by Type

5.1. Overview

5.2. Orthopedic Devices

5.2.1. Definition, key trends, growth factors, and opportunities

5.2.2. Market size analysis, by region, 2023-2033

5.2.3. Market share analysis, by country, 2023-2033

5.3. In Vitro Diagnostics (IVD)

5.3.1. Definition, key trends, growth factors, and opportunities

5.3.2. Market size analysis, by region, 2023-2033

5.3.3. Market share analysis, by country, 2023-2033

5.4. Cardiovascular Devices

5.4.1. Definition, key trends, growth factors, and opportunities

5.4.2. Market size analysis, by region, 2023-2033

5.4.3. Market share analysis, by country, 2023-2033

5.5. Wound Management

5.5.1. Definition, key trends, growth factors, and opportunities

5.5.2. Market size analysis, by region, 2023-2033

5.5.3. Market share analysis, by country, 2023-2033

5.6. Minimally Invasive Surgical (MIS)

5.6.1. Definition, key trends, growth factors, and opportunities

5.6.2. Market size analysis, by region, 2023-2033

5.6.3. Market share analysis, by country, 2023-2033

5.7. Diabetes Care

5.7.1. Definition, key trends, growth factors, and opportunities

5.7.2. Market size analysis, by region, 2023-2033

5.7.3. Market share analysis, by country, 2023-2033

5.8. Dental Devices

5.8.1. Definition, key trends, growth factors, and opportunities

5.8.2. Market size analysis, by region, 2023-2033

5.8.3. Market share analysis, by country, 2023-2033

5.9. Ophthalmic Devices

5.9.1. Definition, key trends, growth factors, and opportunities

5.9.2. Market size analysis, by region, 2023-2033

5.9.3. Market share analysis, by country, 2023-2033

5.10. General Surgery

5.10.1. Definition, key trends, growth factors, and opportunities

5.10.2. Market size analysis, by region, 2023-2033

5.10.3. Market share analysis, by country, 2023-2033

5.11. Others

5.11.1. Definition, key trends, growth factors, and opportunities

5.11.2. Market size analysis, by region, 2023-2033

5.11.3. Market share analysis, by country, 2023-2033

5.12. Research Dive Exclusive Insights

5.12.1. Market attractiveness

5.12.2. Competition heatmap

6. Medical Devices Market Analysis, by End User

6.1. Overview

6.2. Hospitals & Ambulatory Surgery Centers (ASCs)

6.2.1. Definition, key trends, growth factors, and opportunities

6.2.2. Market size analysis, by region, 2023-2033

6.2.3. Market share analysis, by country, 2023-2033

6.3. Clinics

6.3.1. Definition, key trends, growth factors, and opportunities

6.3.2. Market size analysis, by region, 2023-2033

6.3.3. Market share analysis, by country, 2023-2033

6.4. Others

6.4.1. Definition, key trends, growth factors, and opportunities

6.4.2. Market size analysis, by region, 2023-2033

6.4.3. Market share analysis, by country, 2023-2033

6.5. Research Dive Exclusive Insights

6.5.1. Market attractiveness

6.5.2. Competition heatmap

7. Medical Devices Market, by Region

7.1. North America

7.1.1. U.S.

7.1.1.1. Market size analysis, by Type, 2023-2033

7.1.1.2. Market size analysis, by End User, 2023-2033

7.1.2. Canada

7.1.2.1. Market size analysis, by Type, 2023-2033

7.1.2.2. Market size analysis, by End User, 2023-2033

7.1.3. Mexico

7.1.3.1. Market size analysis, by Type, 2023-2033

7.1.3.2. Market size analysis, by End User, 2023-2033

7.1.4. Research Dive Exclusive Insights

7.1.4.1. Market attractiveness

7.1.4.2. Competition heatmap

7.2. Europe

7.2.1. Germany

7.2.1.1. Market size analysis, by Type, 2023-2033

7.2.1.2. Market size analysis, by End User, 2023-2033

7.2.2. UK

7.2.2.1. Market size analysis, by Type, 2023-2033

7.2.2.2. Market size analysis, by End User, 2023-2033

7.2.3. France

7.2.3.1. Market size analysis, by Type, 2023-2033

7.2.3.2. Market size analysis, by End User, 2023-2033

7.2.4. Spain

7.2.4.1. Market size analysis, by Type, 2023-2033

7.2.4.2. Market size analysis, by End User, 2023-2033

7.2.5. Italy

7.2.5.1. Market size analysis, by Type, 2023-2033

7.2.5.2. Market size analysis, by End User, 2023-2033

7.2.6. Rest of Europe

7.2.6.1. Market size analysis, by Type, 2023-2033

7.2.6.2. Market size analysis, by End User, 2023-2033

7.2.7. Research Dive Exclusive Insights

7.2.7.1. Market attractiveness

7.2.7.2. Competition heatmap

7.3. Asia-Pacific

7.3.1. China

7.3.1.1. Market size analysis, by Type, 2023-2033

7.3.1.2. Market size analysis, by End User, 2023-2033

7.3.2. Japan

7.3.2.1. Market size analysis, by Type, 2023-2033

7.3.2.2. Market size analysis, by End User, 2023-2033

7.3.3. India

7.3.3.1. Market size analysis, by Type, 2023-2033

7.3.3.2. Market size analysis, by End User, 2023-2033

7.3.4. Australia

7.3.4.1. Market size analysis, by Type, 2023-2033

7.3.4.2. Market size analysis, by End User, 2023-2033

7.3.5. South Korea

7.3.5.1. Market size analysis, by Type, 2023-2033

7.3.5.2. Market size analysis, by End User, 2023-2033

7.3.6. Rest of Asia-Pacific

7.3.6.1. Market size analysis, by Type, 2023-2033

7.3.6.2. Market size analysis, by End User, 2023-2033

7.3.7. Research Dive Exclusive Insights

7.3.7.1. Market attractiveness

7.3.7.2. Competition heatmap

7.4. LAMEA

7.4.1. Brazil

7.4.1.1. Market size analysis, by Type, 2023-2033

7.4.1.2. Market size analysis, by End User, 2023-2033

7.4.2. UAE

7.4.2.1. Market size analysis, by Type, 2023-2033

7.4.2.2. Market size analysis, by End User, 2023-2033

7.4.3. Saudi Arabia

7.4.3.1. Market size analysis, by Type, 2023-2033

7.4.3.2. Market size analysis, by End User, 2023-2033

7.4.4. South Africa

7.4.4.1. Market size analysis, by Type, 2023-2033

7.4.4.2. Market size analysis, by End User, 2023-2033

7.4.5. Rest of LAMEA

7.4.5.1. Market size analysis, by Type, 2023-2033

7.4.5.2. Market size analysis, by End User, 2023-2033

7.4.6. Research Dive Exclusive Insights

7.4.6.1. Market attractiveness

7.4.6.2. Competition heatmap

8. Competitive Landscape

8.1. Top winning strategies, 2023

8.1.1. By strategy

8.1.2. By year

8.2. Strategic overview

8.3. Market share analysis, 2023

9. Company Profiles

9.1. Medtronic

9.1.1. Overview

9.1.2. Business segments

9.1.3. Product portfolio

9.1.4. Financial performance

9.1.5. Recent developments

9.1.6. SWOT analysis

9.2. Koninklijke Philips N.V.

9.2.1. Overview

9.2.2. Business segments

9.2.3. Product portfolio

9.2.4. Financial performance

9.2.5. Recent developments

9.2.6. SWOT analysis

9.3. Johnson & Johnson Services, Inc.

9.3.1. Overview

9.3.2. Business segments

9.3.3. Product portfolio

9.3.4. Financial performance

9.3.5. Recent developments

9.3.6. SWOT analysis

9.4. Abbott

9.4.1. Overview

9.4.2. Business segments

9.4.3. Product portfolio

9.4.4. Financial performance

9.4.5. Recent developments

9.4.6. SWOT analysis

9.5. Siemens Healthineers AG

9.5.1. Overview

9.5.2. Business segments

9.5.3. Product portfolio

9.5.4. Financial performance

9.5.5. Recent developments

9.5.6. SWOT analysis

9.6. Stryker

9.6.1. Overview

9.6.2. Business segments

9.6.3. Product portfolio

9.6.4. Financial performance

9.6.5. Recent developments

9.6.6. SWOT analysis

9.7. GE Healthcare

9.7.1. Overview

9.7.2. Business segments

9.7.3. Product portfolio

9.7.4. Financial performance

9.7.5. Recent developments

9.7.6. SWOT analysis

9.8. BD

9.8.1. Overview

9.8.2. Business segments

9.8.3. Product portfolio

9.8.4. Financial performance

9.8.5. Recent developments

9.8.6. SWOT analysis

9.9. Cardinal Health

9.9.1. Overview

9.9.2. Business segments

9.9.3. Product portfolio

9.9.4. Financial performance

9.9.5. Recent developments

9.9.6. SWOT analysis

9.10. Boston Scientific Corporation

9.10.1. Overview

9.10.2. Business segments

9.10.3. Product portfolio

9.10.4. Financial performance

9.10.5. Recent developments

9.10.6.SWOT analysis

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com