Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

IC2003147 |

Pages: 220 |

Feb 2023 |

Nowadays, regardless of the company’s operations, all businesses and organizations rely on computer tools and information systems to speed up the process value chain. The execution of these operations is crucial to the operation of the business. In contrast, and despite its significance, the computer tool is still the weakest link in existing businesses because the unavailability of an application or machine room for a few hours can become a catastrophe that leads to negative outcomes like a significant loss of revenue or damage to the reputation of the company.

In the event of a natural or man-made calamity, virtual servers and data centers can be replicated and recovered using disaster recovery-as-a-service, a third-party cloud computing and backup service paradigm. To protect the organization's sensitive data, the backup is typically created in a public, cloud, virtual private cloud (VPC), or hybrid environment. By minimizing downtime and disturbances, the disaster recovery-as-a-service solutions delivers total support and control over the network during failures and assures business continuity. These factors are anticipated to boost the disaster recovery-as-a-service market growth in the upcoming years.

However, many companies are worried about data leak because the majority of their information is housed on cloud servers. Companies are stepping up system security as a result of an increase in data breaches and hacking incidents. Many businesses do not view disaster recovery-as-a-service (DRaaS) as a realistic solution because it entails working with outside entities and could pose a risk of a data breach. These factors are anticipated to restrain the disaster recovery-as-a-service market share in the upcoming years.

However, disaster recovery solutions are widely used by both public and private enterprises to preserve their data and application services. Supporting business continuity, which enables speedier recovery but comes with a price tag, is a major difficulty in providing a DR service. These days, cloud-based DR solutions take the place of outdated methods and provide infrastructure & operations specialists with a quick and affordable fix. With cloud computing and its pay-per-use pricing model, businesses may pay for long-term data storage and applications while only spending money on the storage they actually need. Previously, they had to purchase resources for an off-site DR location. Many businesses are aiming for a cloud-based disaster recovery method to store their data on the cloud. These factors are anticipated to boost the disaster recovery-as-a-service industry demand in the coming years

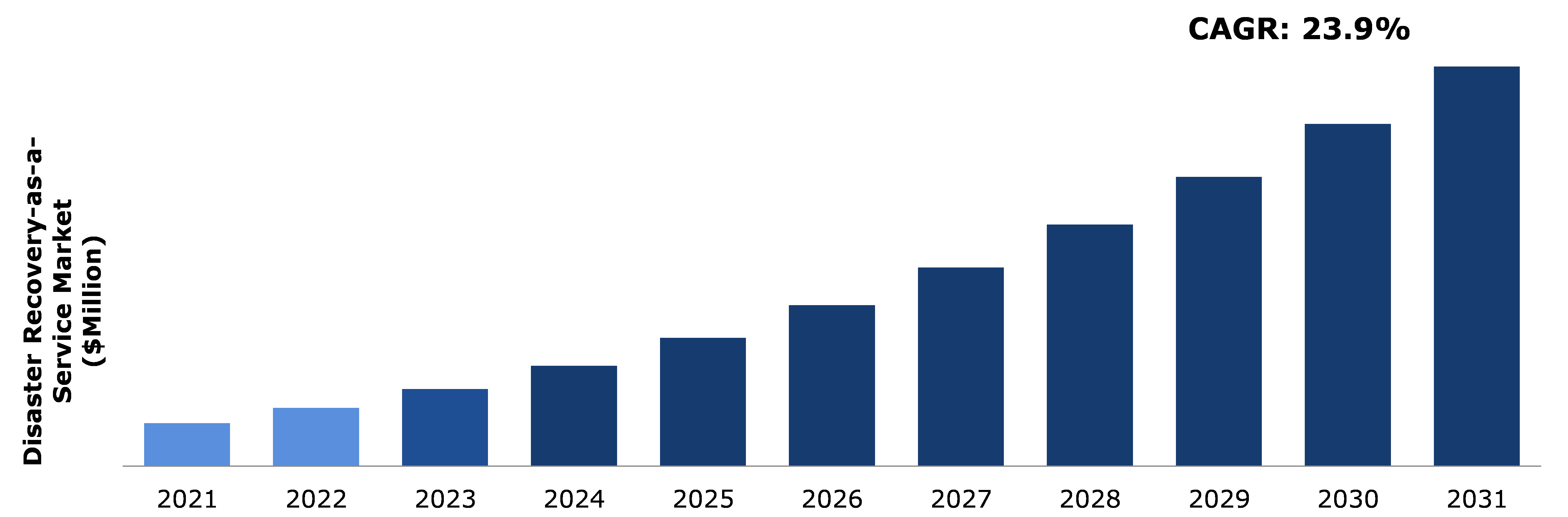

According to regional analysis, the North America disaster recovery-as-a-service market accounted for the highest market size in 2021 and is estimated to grow at a significant pace during the analysis timeframe. This is majorly owing to the presence of large number of trusted disaster recovery-as-a-service solution providers and rapid technological advancements in BFSI, healthcare, and retail sectors in this region.

An organization's capacity to respond to and recover from a situation that adversely impacts business operations is known as disaster recovery (DR). The objective of disaster recovery (DR) techniques is to make it feasible for an organization to quickly resume using its vital IT infrastructure and systems following a disaster. Organizations frequently conduct a thorough review of their systems in advance of this and produce a formal document that should be followed in a crisis. This is to distinguish between a straightforward network outage and a crisis situation and to respond appropriately.

The COVID-19 pandemic has brought several uncertainties leading to severe economic losses as various businesses across the world were standstill. However, the disaster recovery-as-a-service market growth was positively impacted during the pandemic. This is because there was a drastic increase in online transactions during the pandemic owing to travel restrictions, lockdown, and social distancing norms. Such an increase in online transactions has increased the demand for data security solutions to avoid data loss or to prevent hacking attacks. The disaster recovery-as-a-service is an essential cloud-based disaster recovery solution that prevents data loss due to natural or man-made calamities. Also, disaster recovery-as-a-service played a major role in reducing downtime and boosting productivity during the pandemic as majority of the corporate employees were working from home. All these aspects have led to a positive impact on the disaster recovery-as-a-service market size during the pandemic.

Disaster Recovery-as-a-Service market size is growing rapidly owing to several benefits offered by this cloud computing service model. For instance, DRaaS helps several organizations to back up their data and crucial IT infrastructure on cloud to ensure business continuity. DRaaS helps facilitates efficient recovery of crucial data as many disasters such as floods, hurricanes, earthquakes, and wildfires can result in data loss. Additionally, power outages, equipment failure, and cyberattacks can result in data loss that has become more frequent in recent years.

Technological information and data systems have grown exponentially more vulnerable as a result of this ongoing growth. The interruptions range in severity from little ones like a brief loss of power or disc drive failure to major ones like a fire. Although the vulnerabilities may be reduced or removed through management, operational, or technical controls, it is practically difficult to totally eradicate all risks as part of the department's resiliency endeavor. Due in large part to its reasonable pricing structure, disaster recovery-as-a-service is becoming more and more popular among businesses of all kinds. Using disaster recovery-as-a-service through a third-party service provider efficiently eliminates the majority of the extra costs associated with hosting the data in a cloud server. This further reduces the company's unnecessary costs, such as those related to the purchase or leasing of server, network, and storage equipment, holding space for auxiliary datacenters, spending monthly expenses for ventilation, electricity, and broadband. These factors are anticipated to generate excellent opportunities to boost the Disaster Recovery-as-a-Service market share in the coming years.

To know more about global disaster recovery-as-a-service market drivers, get in touch with our analysts here.

Data is now one of the most important elements of an organization in the digital age. Organizations face considerable risks from data leaks, including significant brand harm and financial losses. Finding and avoiding data loss has emerged as one of the most urgent security challenges for businesses as a result of the exponential growth in data volume and the increasing frequency of data breaches. These factors are going to hamper the growth of disaster recovery-as-a-service market demand in the forecasted time period.

Large-scale internet services, such as data backup and information recovery, are becoming easier to find due to the rapid development of internet technology. Designing equally large-scale computer infrastructures that support these online services cost-effectively has proven to be a significant issue because these large-scale services demand significant networking, processing, and storage capacities. Over the past ten years, cloud computing has been improved in response to this increase in demand, becoming a lucrative industry for companies that possess sizable datacenters and provide their computer resources. Without a doubt, cloud computing offers great advantages for data backup and accessibility at a fair price. Thus, the disaster recovery-as-a-service (DRaaS) is now a great choice for businesses of all kinds, including major companies, thanks to advancements in cloud and replication technology. The cost of a secondary site is eliminated by the subscription model, while network transparency, rerouting simplicity, and better tools have made DRaaS less of a laborious but necessary effort.

To know more about global Disaster Recovery-as-a-Service market opportunities, get in touch with our analysts here.

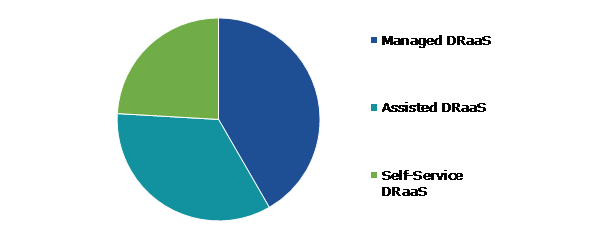

Based on operating model, the market has been divided into managed DRaaS, assisted DRaaS, and self-service DRaaS. Among these, the managed DRaaS sub-segment accounted for the highest market share in 2021.

Source: Research Dive Analysis

The managed DRaaS sub-type accounted for the highest market in 2021 and is predicted to show the fastest growth by 2031. Disaster Recovery-as-a-Service (DRaaS) is a solution that offers server workload recovery and data replication in a cloud environment. As managed DRaaS handles routine management chores such as firewalls, load balancing, monitoring, antivirus, operating system patching, and networking, the platform delivers cloud strategy optimization and experience. The service and support will offer users different combinations of the required managed services. A managed service with a subscription model eliminates the need to invest in, set up, and manage hardware, operating systems, and infrastructure for disaster recovery data centers.

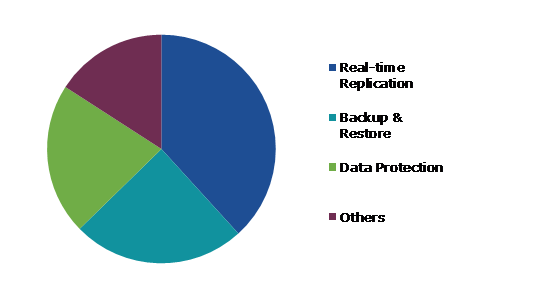

Based on service type, the market has been divided into real-time replication, backup & restore, data protection, and others. Among these, the real-time replication sub-segment accounted for highest revenue share in 2021.

Source: Research Dive Analysis

The real-time replication sub-segment accounted for the highest market share in 2021. Disaster Recovery-as-a-Service real-time replication is the process of instantly transferring data from one or more locations to another as it is being created. In reality, a period of time always passes between the time data is generated and the time it is duplicated. Real-time replication has a wide range of applications, including data distribution to other servers for reporting or application processing, data warehouse feeding, and data synchronization with faraway offices.

The backup & restore sub-segment is anticipated to show the fastest market growth by 2031. A service called backup and restore will handle copying and archiving client files on a distant server. The data is sent to the cloud-based server through a secure network. On the other hand, infrastructure as a service, which is used for cloud-based disaster recovery, backs up the data on a distant server. Instead of relying on non-proprietary methods to manage data, it is advised to select backup-as-a-service providers. Backups are used to restore data in the event of loss or damage, typically via deletion or damage. Data loss due to deleting, disc or system failure, malware, fire, or other disasters has happened or is likely to happen in this case, so the backup & restore plan helps the organization recover important data.

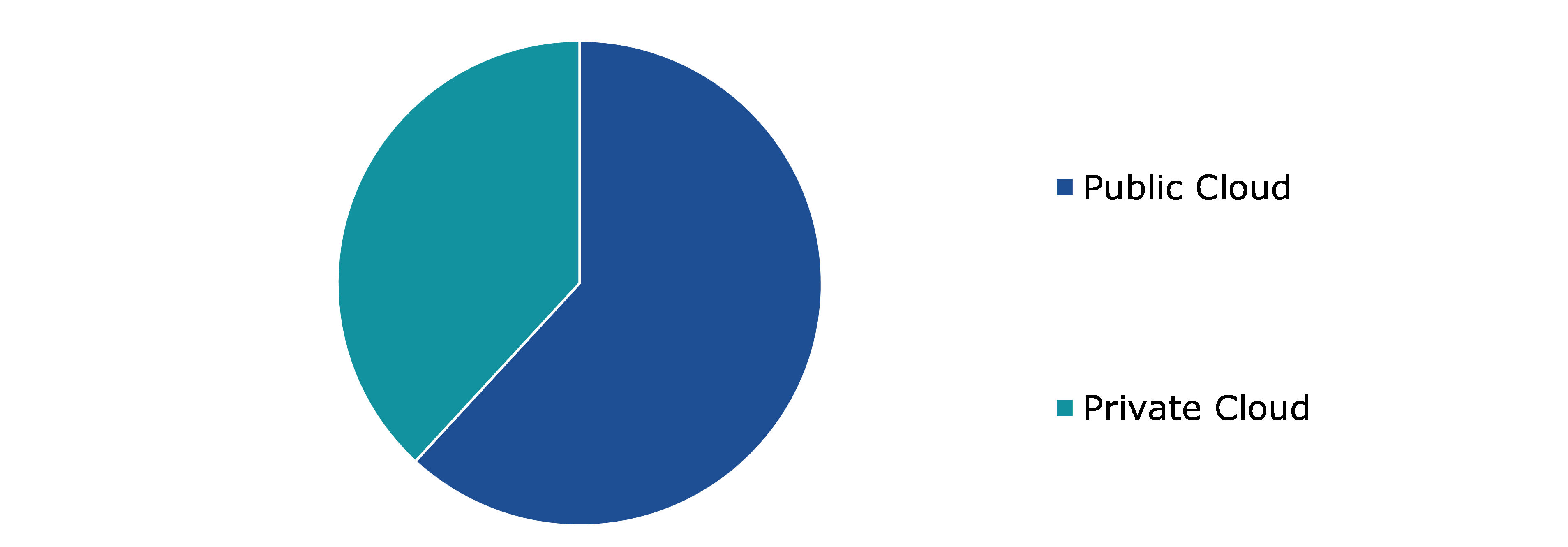

Based on deployment mode, the market has been divided into public cloud and private cloud. Among these, the public cloud sub-segment accounted for the highest market share in 2021.

Source: Research Dive Analysis

The public cloud sub-segment accounted for the highest market share in 2021. There are many applications for public cloud storage where its scalability, agility, and economic flexibility are appealing. The fail-over sites in a cloud provider's workload, such as Azure or AWS, are maintained by public cloud disaster recovery. The only operational expense associated with public cloud disaster recovery is licensing; however, the operating cost of public cloud may become expensive depending on the size and usage of protected resources.

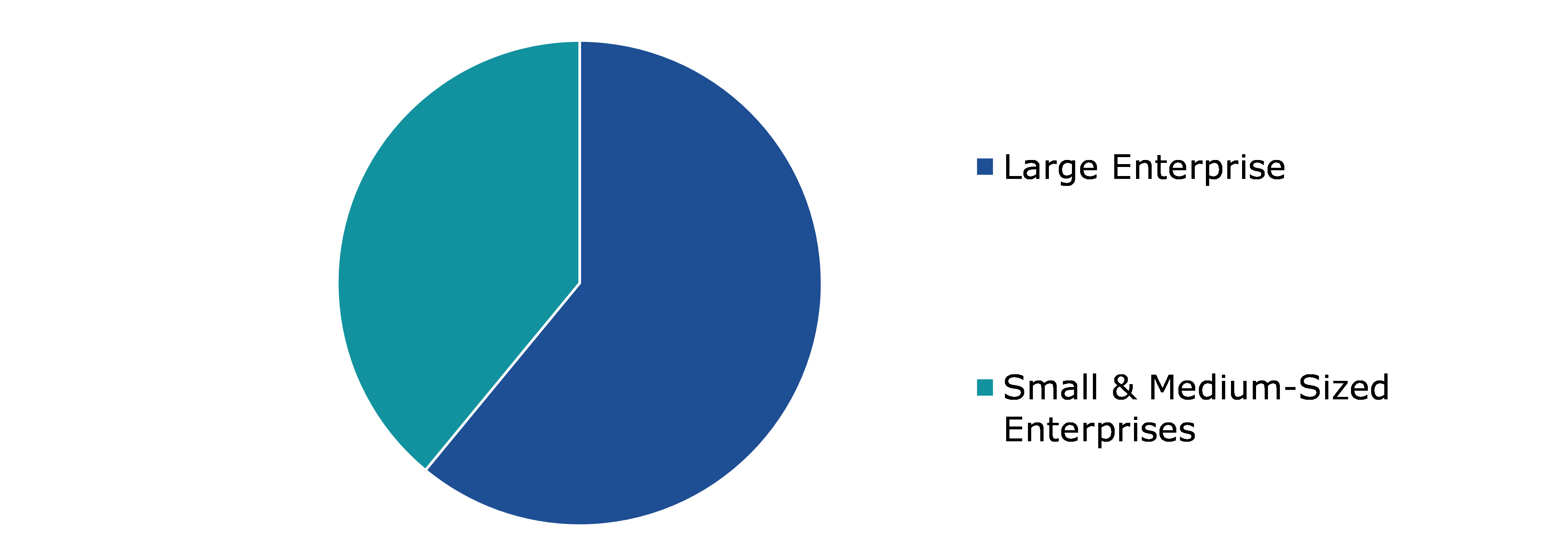

Based on organization size, the market has been divided into large enterprise and small & medium-sized enterprises. Among these, the large enterprises sub-segment accounted for the highest market share in 2021.

Source: Research Dive Analysis

The large enterprise sub-type accounted for a highest market in 2021. Large enterprise make significant investments in cutting-edge technology to boost their overall efficiency and effectiveness. Large enterprises are urged to adopt cutting-edge DRaaS solutions into their operations in order to boost revenue and stay competitive. They also hold a larger market share since new technologies are more readily available. Furthermore, because large enterprises store a large amount of data, they are increasing their investments in disaster recovery service systems. These factors are expected to boost the disaster recovery-as-a-service market demand for large enterprise segment during the forecast period. in

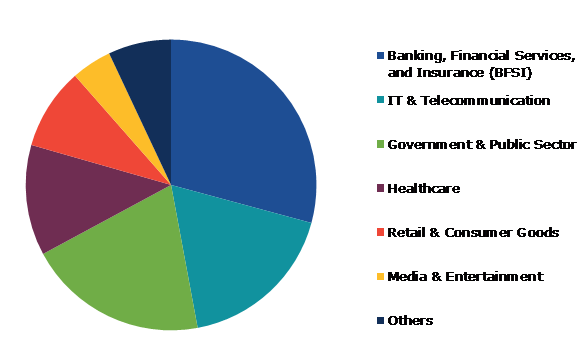

Based on end-use industry, the market has been divided into banking, financial services, and insurance (BFSI), IT & telecommunication, government & public sector, healthcare, retail & consumer goods, media & entertainment, and others. Among these, the banking, financial services, and insurance (BFSI) sub-segment accounted for the highest market share in 2021.

Source: Research Dive Analysis

The banking, financial services, and insurance (BFSI) sub-type accounted for highest market share in 2021 and is predicted to show the fastest growth by 2031. Disasters can be crucial for companies in the key banking, financial services, and insurance (BFSI) field, as downtime can have drastic consequences. Thus, it is crucial to have a comprehensive disaster recovery plan that guarantees business continuity. This necessitates that every BFSI organization understand the principles of "predictive intelligence," which include incident prevention, monitoring, reaction, restoration, and recovery, and develop the necessary approach to execute resilience. Disaster Recovery-as-a-Service (DRaaS) is a strong alternative because it enables businesses to balance a quick disaster recovery solution with a cheaper cost.

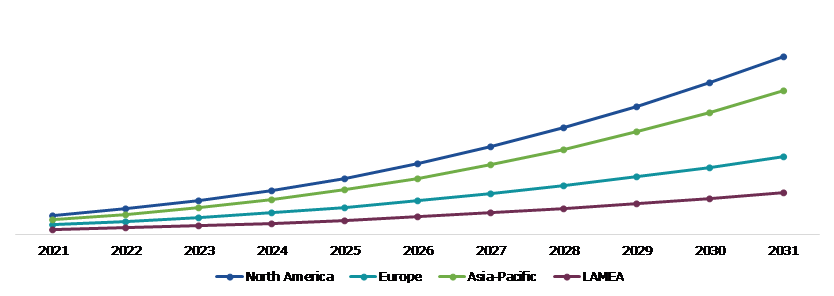

The Disaster Recovery-as-a-Service market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The North America Disaster Recovery-as-a-Service market accounted for the highest market share in 2021. The existence of a significant number of businesses in the region and the high penetration rate in the telecommunications, information technology, and financial services industries are anticipated to be the main drivers for the expansion of the disaster recovery-as-a-service market share in the region. The presence of certain significant players, including Microsoft Corporation, IBM Corporation, and Amazon Web Services, plays an important role in this market that boosts the disaster recovery-as-a-service market growth. The expansion of the disaster recovery-as-a-service market in this region has been fueled by significant investments in research & development as well as the expanding usage of cutting-edge technologies like cloud technology. High demand for data centers and increasing use of disaster recovery-as-a-service by both small and large businesses are anticipated to boost the disaster recovery-as-a-service market in the forecasted time period.

Investment and agreement are common strategies followed by major market players. For instance, in April 2022, to recover more quickly from significant cybersecurity events such as malware infections, Kyndryl, a former IBM division and current managed infrastructure service provider, will have integrated air-gapped data vaulting technology from Dell.

Source: Research Dive Analysis

Some of the leading disaster recovery-as-a-service market players are Microsoft Corporation, Amazon Web Services, Inc., IBM, VMware, Inc., Sungard Availability Services, Recovery Point, InterVision, TierPoint, LLC, Infrascale, and Acronis International GmbH.

| Aspect | Particulars |

| Historical Market Estimations | 2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Operating Model |

|

| Segmentation by Service Type |

|

| Segmentation by Deployment Mode |

|

| Segmentation by Organization Size |

|

| Segmentation by End-use Industry |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global disaster recovery-as-a-service market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of providers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on disaster recovery-as-a-service market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Disaster Recovery-as-a-Service Market Analysis, by Operating Model

5.1.Overview

5.2.Managed DRaaS

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region, 2021-2031

5.2.3.Market share analysis, by country, 2021-2031

5.3.Assisted DRaaS

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region, 2021-2031

5.3.3.Market share analysis, by country, 2021-2031

5.4.Self-Service DRaaS

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region, 2021-2031

5.4.3.Market share analysis, by country, 2021-2031

5.5.Research Dive Exclusive Insights

5.5.1.Market attractiveness

5.5.2.Competition heatmap

6.Disaster Recovery-as-a-Service Market Analysis, by Service Type

6.1.Overview

6.2.Real-time Replication

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region, 2021-2031

6.2.3.Market share analysis, by country, 2021-2031

6.3.Backup & Restore

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.2.Market size analysis, by region, 2021-2031

6.3.3.Market share analysis, by country, 2021-2031

6.4.Data Protection

6.4.1.Definition, key trends, growth factors, and opportunities

6.4.2.Market size analysis, by region, 2021-2031

6.4.3.Market share analysis, by country, 2021-2031

6.5.Others

6.5.1.Definition, key trends, growth factors, and opportunities

6.5.2.Market size analysis, by region, 2021-2031

6.5.3.Market share analysis, by country, 2021-2031

6.6.Research Dive Exclusive Insights

6.6.1.Market attractiveness

6.6.2.Competition heatmap

7.Disaster Recovery-as-a-Service Market Analysis, by Deployment Mode

7.1.Overview

7.2.Public Cloud

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region, 2021-2031

7.2.3.Market share analysis, by country, 2021-2031

7.3.Private Cloud

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region, 2021-2031

7.3.3.Market share analysis, by country, 2021-2031

7.4.Research Dive Exclusive Insights

7.4.1.Market attractiveness

7.4.2.Competition heatmap

8.Disaster Recovery-as-a-Service Market Analysis, by Organization Size

8.1.Overview

8.2.Large Enterprise

8.2.1.Definition, key trends, growth factors, and opportunities

8.2.2.Market size analysis, by region, 2021-2031

8.2.3.Market share analysis, by country, 2021-2031

8.3.Small & Medium-Sized Enterprises

8.3.1.Definition, key trends, growth factors, and opportunities

8.3.2.Market size analysis, by region, 2021-2031

8.3.3.Market share analysis, by country, 2021-2031

8.4.Research Dive Exclusive Insights

8.4.1.Market attractiveness

8.4.2.Competition heatmap

9.Disaster Recovery-as-a-Service Market Analysis, by End-use Industry

9.1.Banking, Financial Services, and Insurance (BFSI)

9.1.1.Definition, key trends, growth factors, and opportunities

9.1.2.Market size analysis, by region, 2021-2031

9.1.3.Market share analysis, by country, 2021-2031

9.2.IT & Telecommunication

9.2.1.Definition, key trends, growth factors, and opportunities

9.2.2.Market size analysis, by region, 2021-2031

9.2.3.Market share analysis, by country, 2021-2031

9.3.Government & Public Sector

9.3.1.Definition, key trends, growth factors, and opportunities

9.3.2.Market size analysis, by region, 2021-2031

9.3.3.Market share analysis, by country, 2021-2031

9.4.Healthcare

9.4.1.Definition, key trends, growth factors, and opportunities

9.4.2.Market size analysis, by region, 2021-2031

9.4.3.Market share analysis, by country, 2021-2031

9.5.Retail & Consumer Goods

9.5.1.Definition, key trends, growth factors, and opportunities

9.5.2.Market size analysis, by region, 2021-2031

9.5.3.Market share analysis, by country, 2021-2031

9.6.Media & Entertainment

9.6.1.Definition, key trends, growth factors, and opportunities

9.6.2.Market size analysis, by region, 2021-2031

9.6.3.Market share analysis, by country, 2021-2031

9.7.Pharmaceutical

9.7.1.Definition, key trends, growth factors, and opportunities

9.7.2.Market size analysis, by region, 2021-2031

9.7.3.Market share analysis, by country, 2021-2031

9.8.Others

9.8.1.Definition, key trends, growth factors, and opportunities

9.8.2.Market size analysis, by region, 2021-2031

9.8.3.Market share analysis, by country, 2021-2031

9.9.Research Dive Exclusive Insights

9.9.1.Market attractiveness

9.9.2.Competition heatmap

10.Disaster Recovery-as-a-Service Market, by Region

10.1.North America

10.1.1.U.S.

10.1.1.1.Market size analysis, by Operating Model, 2021- 2031

10.1.1.2.Market size analysis, by Service Type, 2021- 2031

10.1.1.3.Market size analysis, by Deployment Model, 2021- 2031

10.1.1.4.Market size analysis, by Organization Size, 2021- 2031

10.1.1.5.Market size analysis, by End-use Industry, 2021- 2031

10.1.2.Canada

10.1.2.1.Market size analysis, by Operating Model, 2021- 2031

10.1.2.2.Market size analysis, by Service Type, 2021- 2031

10.1.2.3.Market size analysis, by Deployment Model, 2021- 2031

10.1.2.4.Market size analysis, by Organization Size, 2021- 2031

10.1.2.5.Market size analysis, by End-use Industry, 2021- 2031

10.1.3.Mexico

10.1.3.1.Market size analysis, by Operating Model, 2021- 2031

10.1.3.2.Market size analysis, by Service Type, 2021- 2031

10.1.3.3.Market size analysis, by Deployment Model, 2021- 2031

10.1.3.4.Market size analysis, by Organization Size, 2021- 2031

10.1.3.5.Market size analysis, by End-use Industry, 2021- 2031

10.1.4.Research Dive Exclusive Insights

10.1.4.1.Market attractiveness

10.1.4.2.Competition heatmap

10.2.Europe

10.2.1.Germany

10.2.1.1.Market size analysis, by Operating Model, 2021- 2031

10.2.1.2.Market size analysis, by Service Type, 2021- 2031

10.2.1.3.Market size analysis, by Deployment Model, 2021- 2031

10.2.1.4.Market size analysis, by Organization Size, 2021- 2031

10.2.1.5.Market size analysis, by End-use Industry, 2021- 2031

10.2.2.UK

10.2.2.1.Market size analysis, by Operating Model, 2021- 2031

10.2.2.2.Market size analysis, by Service Type, 2021- 2031

10.2.2.3.Market size analysis, by Deployment Model, 2021- 2031

10.2.2.4.Market size analysis, by Organization Size, 2021- 2031

10.2.2.5.Market size analysis, by End-use Industry, 2021- 2031

10.2.3.France

10.2.3.1.Market size analysis, by Operating Model, 2021- 2031

10.2.3.2.Market size analysis, by Service Type, 2021- 2031

10.2.3.3.Market size analysis, by Deployment Model, 2021- 2031

10.2.3.4.Market size analysis, by Organization Size, 2021- 2031

10.2.3.5.Market size analysis, by End-use Industry, 2021- 2031

10.2.4.Spain

10.2.4.1.Market size analysis, by Operating Model, 2021- 2031

10.2.4.2.Market size analysis, by Service Type, 2021- 2031

10.2.4.3.Market size analysis, by Deployment Model, 2021- 2031

10.2.4.4.Market size analysis, by Organization Size, 2021- 2031

10.2.4.5.Market size analysis, by End-use Industry, 2021- 2031

10.2.5.Italy

10.2.5.1.Market size analysis, by Operating Model, 2021- 2031

10.2.5.2.Market size analysis, by Service Type, 2021- 2031

10.2.5.3.Market size analysis, by Deployment Model, 2021- 2031

10.2.5.4.Market size analysis, by Organization Size, 2021- 2031

10.2.5.5.Market size analysis, by End-use Industry, 2021- 2031

10.2.6.Rest of Europe

10.2.6.1.Market size analysis, by Operating Model, 2021- 2031

10.2.6.2.Market size analysis, by Service Type, 2021- 2031

10.2.6.3.Market size analysis, by Deployment Model, 2021- 2031

10.2.6.4.Market size analysis, by Organization Size, 2021- 2031

10.2.6.5.Market size analysis, by End-use Industry, 2021- 2031

10.2.7.Research Dive Exclusive Insights

10.2.7.1.Market attractiveness

10.2.7.2.Competition heatmap

10.3.Asia Pacific

10.3.1.China

10.3.1.1.Market size analysis, by Operating Model, 2021- 2031

10.3.1.2.Market size analysis, by Service Type, 2021- 2031

10.3.1.3.Market size analysis, by Deployment Model, 2021- 2031

10.3.1.4.Market size analysis, by Organization Size, 2021- 2031

10.3.1.5.Market size analysis, by End-use Industry, 2021- 2031

10.3.2.Japan

10.3.2.1.Market size analysis, by Operating Model, 2021- 2031

10.3.2.2.Market size analysis, by Service Type, 2021- 2031

10.3.2.3.Market size analysis, by Deployment Model, 2021- 2031

10.3.2.4.Market size analysis, by Organization Size, 2021- 2031

10.3.2.5.Market size analysis, by End-use Industry, 2021- 2031

10.3.3.India

10.3.3.1.Market size analysis, by Operating Model, 2021- 2031

10.3.3.2.Market size analysis, by Service Type, 2021- 2031

10.3.3.3.Market size analysis, by Deployment Model, 2021- 2031

10.3.3.4.Market size analysis, by Organization Size, 2021- 2031

10.3.3.5.Market size analysis, by End-use Industry, 2021- 2031

10.3.4.Australia

10.3.4.1.Market size analysis, by Operating Model, 2021- 2031

10.3.4.2.Market size analysis, by Service Type, 2021- 2031

10.3.4.3.Market size analysis, by Deployment Model, 2021- 2031

10.3.4.4.Market size analysis, by Organization Size, 2021- 2031

10.3.4.5.Market size analysis, by End-use Industry, 2021- 2031

10.3.5.South Korea

10.3.5.1.Market size analysis, by Operating Model, 2021- 2031

10.3.5.2.Market size analysis, by Service Type, 2021- 2031

10.3.5.3.Market size analysis, by Deployment Model, 2021- 2031

10.3.5.4.Market size analysis, by Organization Size, 2021- 2031

10.3.5.5.Market size analysis, by End-use Industry, 2021- 2031

10.3.6.Rest of Asia Pacific

10.3.6.1.Market size analysis, by Operating Model, 2021- 2031

10.3.6.2.Market size analysis, by Service Type, 2021- 2031

10.3.6.3.Market size analysis, by Deployment Model, 2021- 2031

10.3.6.4.Market size analysis, by Organization Size, 2021- 2031

10.3.6.5.Market size analysis, by End-use Industry, 2021- 2031

10.3.7.Research Dive Exclusive Insights

10.3.7.1.Market attractiveness

10.3.7.2.Competition heatmap

10.4.LAMEA

10.4.1.Brazil

10.4.1.1.Market size analysis, by Operating Model

10.4.1.2.Market size analysis, by Service Type, 2021- 2031

10.4.1.3.Market size analysis, by Deployment Model, 2021- 2031

10.4.1.4.Market size analysis, by Organization Size, 2021- 2031

10.4.1.5.Market size analysis, by End-use Industry, 2021- 2031

10.4.2.Saudi Arabia

10.4.2.1.Market size analysis, by Operating Model, 2021- 2031

10.4.2.2.Market size analysis, by Service Type, 2021- 2031

10.4.2.3.Market size analysis, by Deployment Model, 2021- 2031

10.4.2.4.Market size analysis, by Organization Size, 2021- 2031

10.4.2.5.Market size analysis, by End-use Industry, 2021- 2031

10.4.3.UAE

10.4.3.1.Market size analysis, by Operating Model, 2021- 2031

10.4.3.2.Market size analysis, by Service Type, 2021- 2031

10.4.3.3.Market size analysis, by Deployment Model, 2021- 2031

10.4.3.4.Market size analysis, by Organization Size, 2021- 2031

10.4.3.5.Market size analysis, by End-use Industry, 2021- 2031

10.4.4.South Africa

10.4.4.1.Market size analysis, by Operating Model, 2021- 2031

10.4.4.2.Market size analysis, by Service Type, 2021- 2031

10.4.4.3.Market size analysis, by Deployment Model, 2021- 2031

10.4.4.4.Market size analysis, by Organization Size, 2021- 2031

10.4.4.5.Market size analysis, by End-use Industry, 2021- 2031

10.4.5.Rest of LAMEA

10.4.5.1.Market size analysis, by Operating Model, 2021- 2031

10.4.5.2.Market size analysis, by Service Type, 2021- 2031

10.4.5.3.Market size analysis, by Deployment Model, 2021- 2031

10.4.5.4.Market size analysis, by Organization Size, 2021- 2031

10.4.5.5.Market size analysis, by End-use Industry, 2021- 2031

10.4.6.Research Dive Exclusive Insights

10.4.6.1.Market attractiveness

10.4.6.2.Competition heatmap

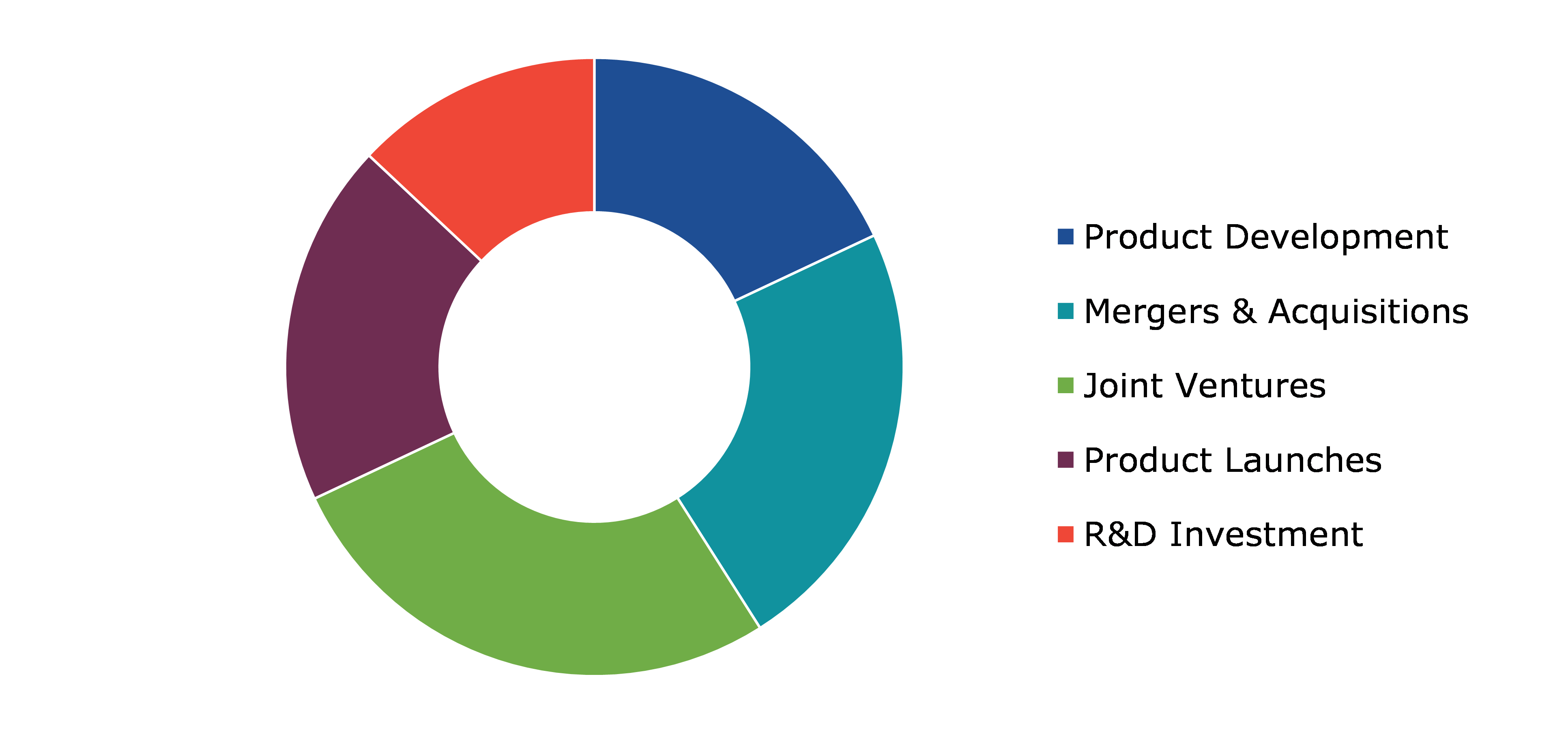

11.Competitive Landscape

11.1.Top winning strategies, 2021

11.1.1.By strategy

11.1.2.By year

11.2.Strategic overview

11.3.Market share analysis, 2021

12.Company Profiles

12.1.IBM Corporation

12.1.1.Overview

12.1.2.Business segments

12.1.3.Product portfolio

12.1.4.Financial performance

12.1.5.Recent developments

12.1.6.SWOT analysis

12.2.HP Development Company, L.P.

12.2.1.Overview

12.2.2.Business segments

12.2.3.Product portfolio

12.2.4.Financial performance

12.2.5.Recent developments

12.2.6.SWOT analysis

12.3.Amazon Web Services, Inc.

12.3.1.Overview

12.3.2.Business segments

12.3.3.Product portfolio

12.3.4.Financial performance

12.3.5.Recent developments

12.3.6.SWOT analysis

12.4.Cable & Wireless Communications Limited.

12.4.1.Overview

12.4.2.Business segments

12.4.3.Product portfolio

12.4.4.Financial performance

12.4.5.Recent developments

12.4.6.SWOT analysis

12.5.TierPoint, LLC.

12.5.1.Overview

12.5.2.Business segments

12.5.3.Product portfolio

12.5.4.Financial performance

12.5.5.Recent developments

12.5.6.SWOT analysis

12.6.Microsoft

12.6.1.Overview

12.6.2.Business segments

12.6.3.Product portfolio

12.6.4.Financial performance

12.6.5.Recent developments

12.6.6.SWOT analysis

12.7.VMware Inc.

12.7.1.Overview

12.7.2.Business segments

12.7.3.Product portfolio

12.7.4.Financial performance

12.7.5.Recent developments

12.7.6.SWOT analysis

12.8.NTT Communications Corporation

12.8.1.Overview

12.8.2.Business segments

12.8.3.Product portfolio

12.8.4.Financial performance

12.8.5.Recent developments

12.8.6.SWOT analysis

12.9.RACKSPACE US, INC.

12.9.1.Overview

12.9.2.Business segments

12.9.3.Product portfolio

12.9.4.Financial performance

12.9.5.Recent developments

12.9.6.SWOT analysis

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}